“I can feel it coming in the air tonight, oh Lord”

~ In The Air Tonight by Phil Collins

“Father tell me, we get what we deserve

Oh we get what we deserveAnd way down we go

Way down we go

Say way down we go

Way down we go”~ Way Down We Go by Kaleo

“The closest thing to eternity on earth is a government program.”

~Ronald Reagan

You would think Reagan fanboys like Donald Trump and Paul Ryan would heed their idol’s words of wisdom, but no. This week, the world’s worst healthcare bill was pulled effectively putting the Trumpflation narrative on notice. To be clear, tax reform is not impossible, just a lot less likely than the market had originally priced. We should see those diminished odds be reflected across the Trumpflation trade over the next few weeks.

I could not agree more with Jawad’s assessment. All the legs of the Trumpflation narrative came under fire this week. First up, long term bond yields are showing no signs of higher expectations of growth. Possible double top forming in the 10 year.

The 30 year is has fallen back to 3% as well.

https://twitter.com/RagnarD80/status/845763066331582468

Of course falling interest rates, and a flatter yield curve bode quite poorly for one of the largest beneficiaries of Trumpflation, US financials.

In this new era of Trump, banks were set to be deregulated allowing them to make more loans. A steepening yield curve means that banks would make more money per loan. On top of making more loans, banks would make more money per loan, a bank bull’s dream. Not only were Trump’s plans of deregulation dealt a sizable a blow and the yield curve flattened to post crisis lows but to make matters even worse, bank lending has been slowing like the US economy is about to enter a recession. In short, this euphoric fever dream has quickly turned into a bad mushroom trip.

From the article:

“We find three key channels that are inhibiting demand growth: 1) political uncertainty, 2) elevated corporate leverage, and 3) Fed policy, both through past tightening and expected tightening going forward. We see little evidence that the slowdown in lending is due to tighter bank or non-bank lending standards.”

Given the embarrassing defeat of the Republicans and Trump administration this week, it appears political uncertainty is far from resolved. Elevated corporate leverage is not going away anytime soon. And the Fed continues to talk a big game despite a lack of data to support their hawkish stance.

It’s not “hard” to see where I’m going with this. It’s 2011 (Déjà vu) all over again.

The Fed may think it can pull its foot off the pedal but the market knows better.

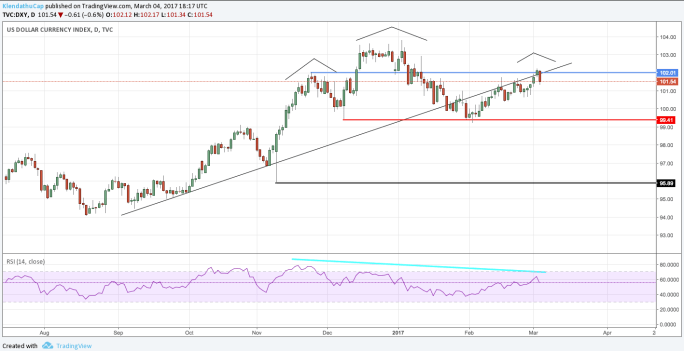

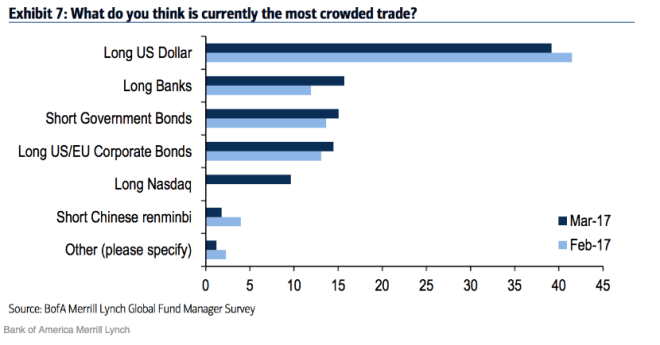

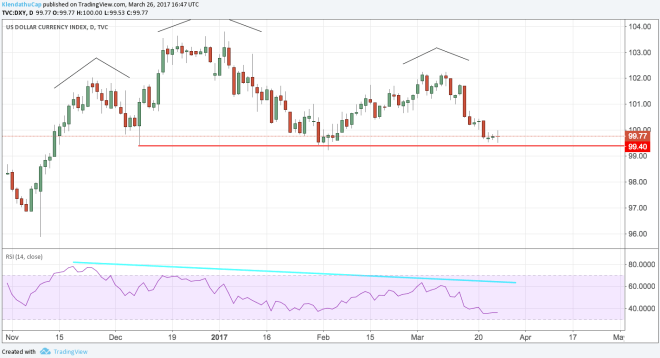

Which brings me to the dollar or what many consider to be the most crowded trade. If the Fed is reached peak 2017 hawkishness, this crowded traded could be in big trouble.

Those betting on higher growth, higher US interest rates, a resurgent financial sector and tax reform are also betting on a stronger dollar. Although I think the case for a stronger dollar over the long term continues to build, the short term forces are only pointed in one direction and that is down.

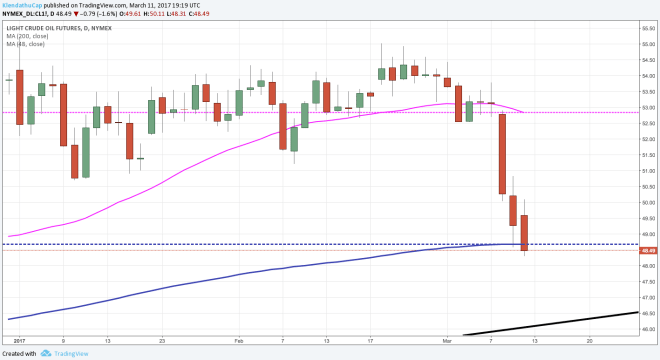

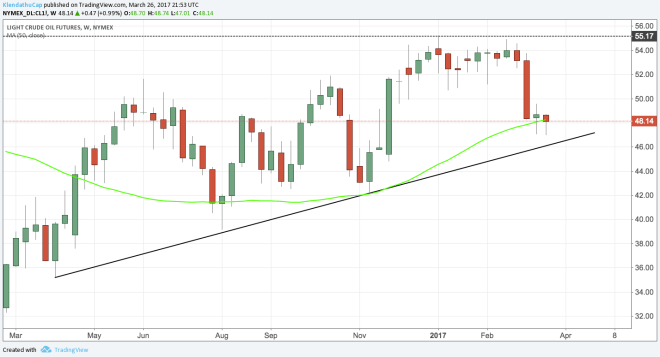

Lastly, oil closed under the 50 week moving average this week for the first time since last July.

I don’t think speculators realized US shale could grow production as fast as it did.

Either that or they really did believe US economic growth was accelerating. Which brings me to the rising role that US shale has played in US economic growth over the past year.

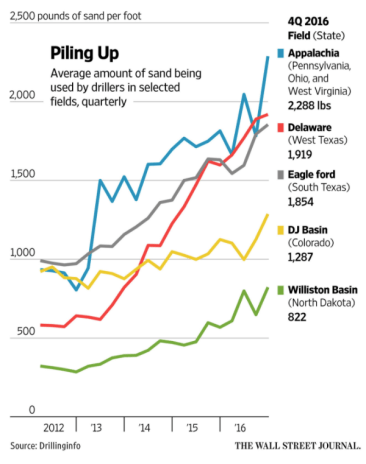

The trucking and sand industries have been huge beneficiaries of the US shale resurgence. To increase the effectiveness of their wells, companies have been using more and more sand per well.

“Tudor, Pickering, Holt & Co. estimates the sector will need 120 million tons of sand by next year, more than double the demand in 2014 at the height of the U.S. drilling boom.”

The increased demand for sand has flowed through to increased trucking demand as well.

“The expense is compounded by the logistics of moving sand from mines to well sites thousands of miles away. Drillers don’t use sand found on a beach. They prefer fine white silica, much of it found in northern Midwest states. Shipping 5 million tons of sand can require 200,000 truck loads, according to a 2013 study by the University of Wisconsin.”

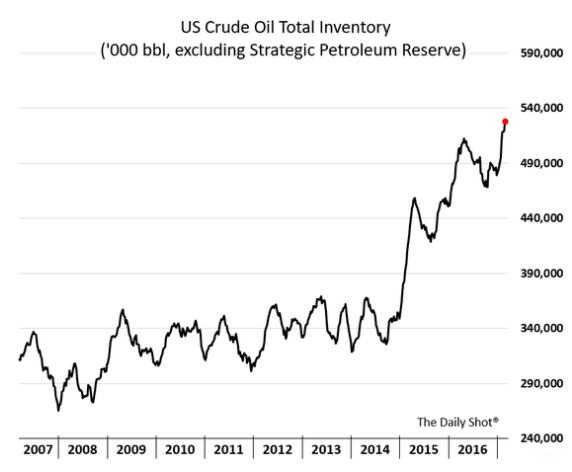

In short, US economic growth is heavily reliant on US shale growth. Lower oil prices not only puts bond bears on notice but US economic bulls as well. The longer oil stays low, the more likely we’ll begin to see a further liquidation of the record long oil contracts.

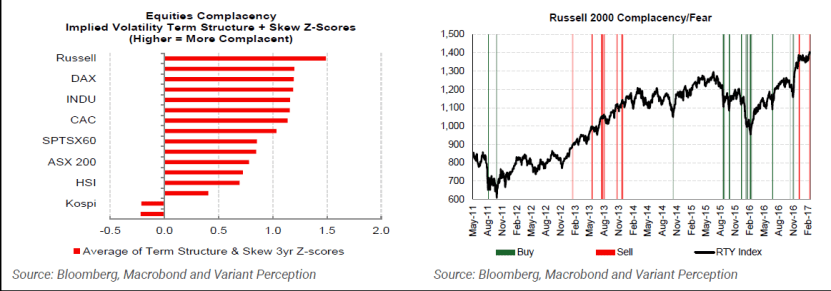

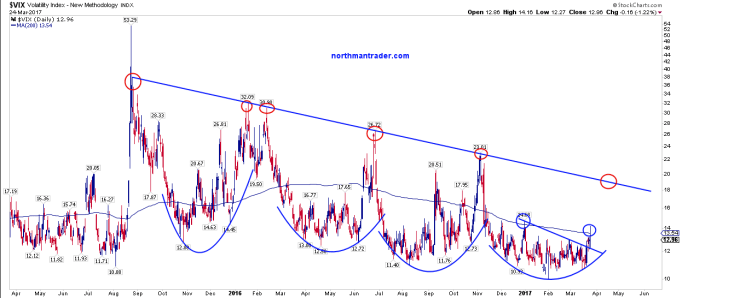

Given the fragility of the situation you might expect investors to be a bit more worried about a pick up in volatility, but you would be wrong. Despite the potential unwind of several large speculative trades, investors remain incredibly complacent.

A lot of this may have to do with volatility being sold short. The fact that this week marked the first weekly close above 12 this year is simply incredible. Which leads me to believe that the sell off we saw this week is likely a prelude to a larger move.

DISCLAIMER: This blog is the diary of a twenty something millennial who has never stepped foot inside a wall street bank. He has not taken an economic or business course since high school (for which he is immensely proud of) and has been long gold since 2012 (which he is not so proud of). In short his opinions and experiences make him uniquely unqualified to give advice. This blog post is NOT advice to buy or sell securities. He may have positions in the aforementioned trades/securities. He may change his opinion the instant the post is published. In short, what follows is pure fiction based loosely in the reality of the ever shifting narrative of the markets. These posts are meant for enjoyment and self reflection and nothing else. So ENJOY and REFLECT!