Man this reflationary trade is getting long in the tooth. The dollar has been subdued for 9 months now and all the bears have either gone back in their caves or transmogrified into bulls. OPEC’s production cut is icing on the proverbial cake at this point.

As a result investors have turned dare I say “wildly” bullish on emerging markets. The demographics look great. The yield is phenomenal. If the dollar stays where it is or goes lower it will rip higher! But what if the dollar doesn’t do any of those things. What if, EM forbid, it begins to rise?

Investors have convinced themselves that the stresses on the global economy that brought about the January sell off have dissipated. When in reality, they’ve actually grown tremendously.

Or as Leland Miller, president of China Beige Book puts it:

“Right now, the markets are lulled to sleep… People become used to the stable China narrative until they start looking more closely into the data.”

But he goes even further.

“I’d find it earth-shatteringly surprising if we don’t have a significant problem between now and China’s leadership change… This is not a stable economy. It’s one that twists and turns and happens to end up at the same spot. There are real problems below the surface.”

Real problems like the stark differences between cities.

The richest man in China, Billionaire Wang Jianlin describes the situation:

“prices keep rising in major Chinese metropolises like Shanghai but are falling in thousands of smaller cities where huge numbers of properties lie empty.”

In essence, money is crowding into the good and leaving the bad investments. Starving the weak to feed the strong will only exacerbate the current issues facing China. The situation is so bad that Wang Jianlin doesn’t even see a palatable solution.

“I don’t see a good solution to this problem… The government has come up with all sorts of measures — limiting purchase or credit — but none have worked.”

The situation is so bad that the very restrictions meant to curb speculation have actually driven demand higher.

I think the situation has become so bad that the CCP and the PBOC may have realistically just one option left, and that is to drain liquidity from the entire economy. It will hurt. It will hurt A LOT but at this point it’s more valuable to deflate the bubbles before they get systemic and potentially destabilizing (although an argument could be made we past that point long ago). And that is for now, exactly what the PBOC is doing:

“China’s benchmark money-market rate climbed to a 14-month high as the central bank pulled funds from the financial system and commercial lenders stocked up on cash to meet quarter-end requirements.

The seven-day repurchase rate, the benchmark gauge of funding availability in the financial system, rose 12 basis points to 2.75 percent as of 5:07 p.m. in Shanghai. That’s the most expensive since July last year.”

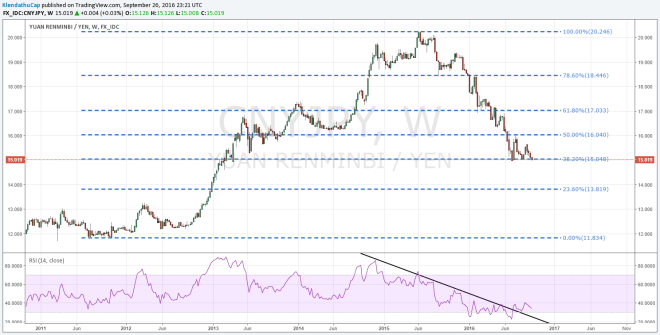

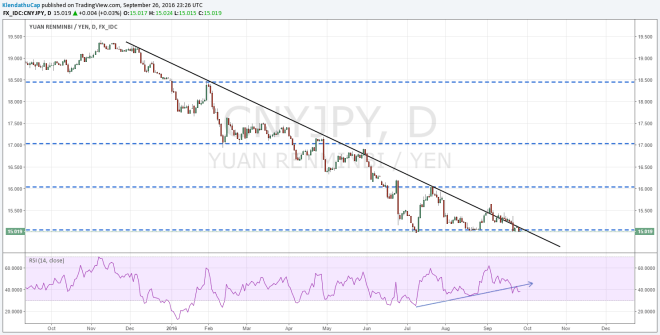

China’s desire to deflate its asset bubbles requires that the Yuan remain strong. Although I’d argue, the PBOC isn’t actually picking a currency level so much as the limit to the size of its asset bubbles which results in a stronger Yuan. In the end, the result is the same. China is finally trying to deflate its financial bubbles with the most blunt tool in its arsenal, liquidity. As Jeffery Snider notes:

“The problem of picking CNY rather than SHIBOR is this money market “uncertainty principle” where if you hold steady the currency (thus “dollars”) you have to let internal liquidity deteriorate. The test came on August 30 when the overnight rate in SHIBOR moved above 2.06% and the PBOC let it by holding fast to CNY. It has only paused in its ascent for one day since then, fixing at 2.095% today.”

Make no mistake, this is an incredibly dangerous game to play. Chinese banks are increasingly relying on not only short term funding but each other for those very funds. Rising short term rates will only exacerbate these issues.

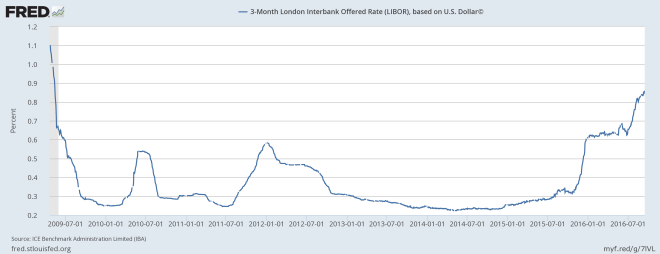

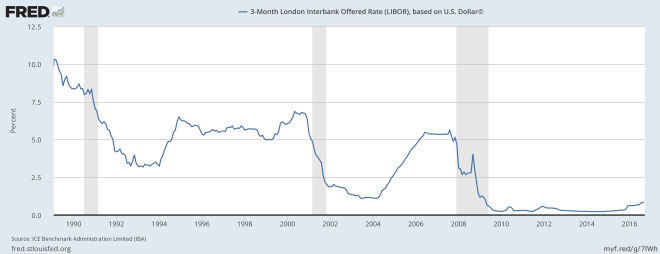

This liquidity issue is not endemic to China. In case that wasn’t evident based on rising LIBOR, negative Yen/dollar and Euro/dollar basis swaps, Deutsche Bank stock hitting fresh lows and Saudi Arabian Banking stocks trading below the February lows. There is a global dollar liquidity problem. Ignore the connections at your own peril. Suffice it to say, it’s not all that surprising the global trade has ground to a halt.

“The World Trade Organization cut its forecast for global trade growth this year by more than a third on Tuesday, reflecting a slowdown in China and falling levels of imports into the United States.”

Falling levels of imports into the US translates into less dollars abroad further exacerbating the very liquidity problems that are grinding global trade to a halt. To say I’m bearish right now would be an understatement. With consensus turning bullish on EM and bearish the dollar, I could not think of a better opportunity to short some risk assets.

Given the liquidity stress, the demand for good collateral such as US treasuries is likely to rise and exceed any selling pressure unleashed by risk parity funds. Although right now that is pure speculation and I will be watching for signs to tell me otherwise. With that said I am holding a small bond position and will not look to add till I better understand the dynamics going forward.

Against the backdrop of potentially falling rates, a rising dollar and rising liquidity risk it isn’t abundantly clear what gold will do. Overall, this is the beginning of an investment theme I expect to take hold over the next three months. More research and time must be devoted before trades and “predictions” can be made. Would you like to know more?

{kind=link}