Me at the beginning of 2016 versus me at the end of 2016. On the left is a man whose life is out of balance. He is missing something. He is estranged from his wife and kids, and it will take a cadre of terrorists for him to realize it. But once he does, he will emerge a stronger and better man. #BestChristmasMovieEver

Well it’s that time of year to recap the wonderful year that 2016. If you go back and read some of my earlier posts (and I kind of hope you don’t), you’ll notice a clear trend of growth, both in writing style and the quality of analysis. My favorite post this year, although it certainly is not the best written, may be #3. Bulls on a Tightrope. It’s hard to face your fears whether in life or your portfolio, but writing that post was incredibly cathartic and launched what I believe was the next step in my journey to becoming a better investor. I want to thank all of my readers for the best year I could have hoped for. Passive investing be damned, it’s time to ride this momentum into 2017!

“Although we are likely in the blow off top phase of US equities, the duration and magnitude of this phase will be dampened due to the abnormally high amount of foreign land mines just waiting for the Fed to step on. If the typical blow off top phase is 18 months, we maybe have 9-12 months which started in early November. I remain open to other possibilities but until new information comes to light, I leave the last word to Admiral Ackbar.”

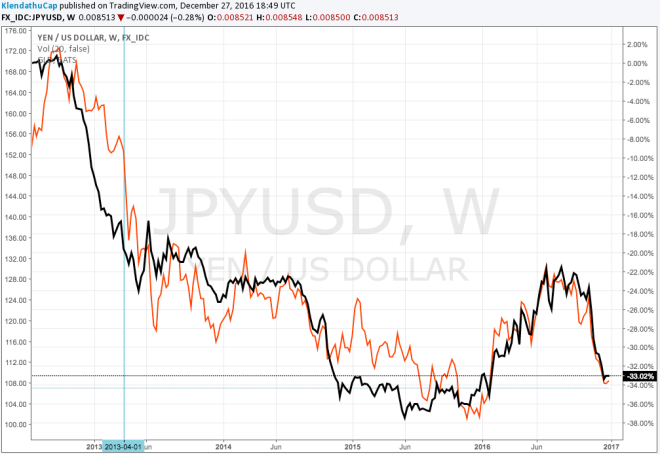

“But given said speculation and the Yen’s refusal to go higher, it’s quite possible USDJPY is bottoming here at the 100 level which just so happens to be the 50% retracement of the 2012-2015 move. As demonstrated multiple times through out this post, I have my doubts, but it is best to remain open near such key inflection points.”

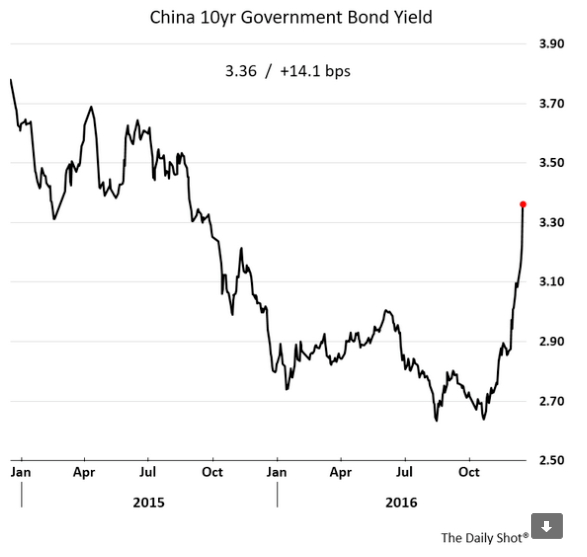

“Speaking of unintended consequences, imagine you are a yield starved Japanese investor whose interest rates have been pinned to floor. Your own central bank has practically outlawed interest rates. Your currency has already started to fall against the US dollar which now offers a much higher rate of return. Would you hold that worthless government paper if US 10-year interest rate rose to 3%? The BOJ seems to be on the verge of monetizing a lot more bonds than it originally signed up for.”

3. Bulls on a Tightrope

“Higher than expected inflation would kill my long us treasury and cash positions. Higher than expected EM demand coupled with a re-surging US economy would kill my short US equities and Canadian banks positions. Hard to say what would happen to gold, but if fears of a global recession faded the price of the yellow metal could take a heavy hit.

Needless to say, in a 6 months my portfolio could go from looking near genius to incomprehensibly stupid, and that is exactly why I decided to discuss the bull case today. Fear is a powerful motivator, and one should never be fully comfortable with their positions.”

2. Predictions For 2017: Shit Escalates

“I think Inflationary pressures originating primarily in China with help from OPEC are quite likely to ripple through the global economy, catching investors and central banks off guard. This inflation surprise should destabilize markets in ways that even the great and powerful Klendathu Capitalist cannot predict (see prediction #10.).

I would argue that those inflationary pressures have already done tremendous damage to the US economy where the US consumer was already suffering under immense pressure from stagnant wages and rising energy and healthcare costs. Unable to provide additional dollar liquidity to the rest of the world, the global economy will slow and the dollar will begin the next leg higher in its bull market”

1. Lithium: Late To The Party But It’s Only Just Begun“Between Elon Musk promising to consume the world’s current production of lithium ion batteries and China pretty much outlawing internal combustion engines by the year 2020 lithium demand is set to take off. Just last year Chinese sales of Electric Vehicles (EVs) increased 223% and a 4 fold increase from 2014.”

Following excerpts are from Shane Black’s The Last Boy Scout.

If you’ve ever read a Shane Black script, and a I recommend you do, especially The Last Boy Scout which was a hell of script that didn’t quite translate to the screen, you’ll notice the man’s affinity for coiled springs. The metaphor is only used twice, but the effect is devastating.

No one writes action like Shane does, the most prolific spec script writer in the most prolific era of spec screenwriting, he was able to sell his pages for one thousand times their weight in gold…

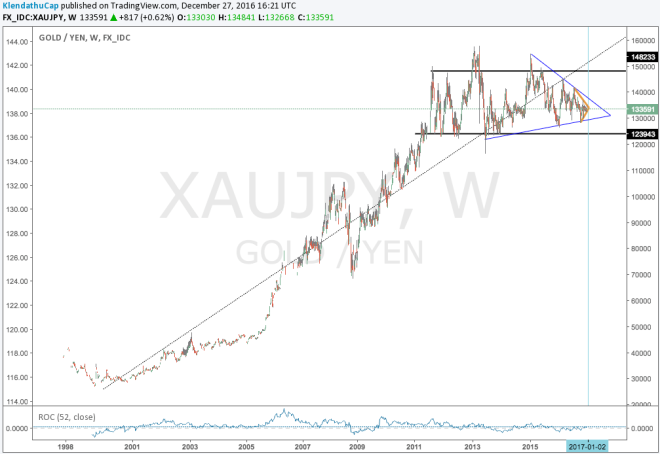

Speaking of gold (#transitions) the Yen has shared an increasingly strong correlation to gold over the last few years. Ever since and even before the BoJ officially launched its QE program in April of 2013, the yellow metal and the Yen have been highly correlated to one another. As the Yen rises so to does gold and vice versa.

Lost in this simple correlation is the fact that XAU/JPY has been locked in a trading range for the past five years.

The same chart, but in log scale. Notice the significance of the 16+ year trend line. Still broken, due to the sideways chop, but I think that will be temporary.

As to why I think we are about to witness a sea change in XAU/JPY cross largely stems from my opinion that developed markets are about to experience much higher inflationary pressures than expected due to Chinese stimulus and base effects from rising oil prices. The BoJ in particular has proven quite slow to react to these inflationary pressures. From my recent post, Predictions for 2017:

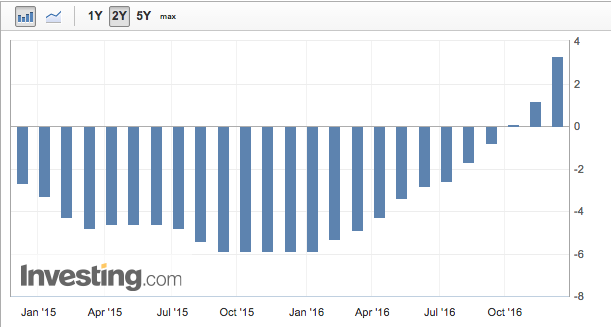

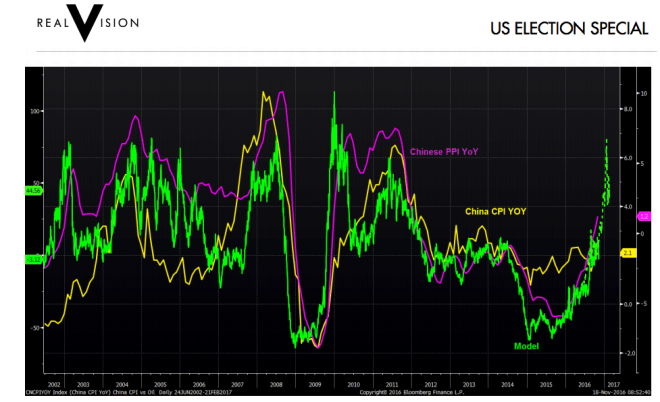

“It needs to be said, that by comparison, the PBoC is light years ahead of their western counter parts, the BOJ in particular. The BoJ pinned bond yields to the floor the same month that Chinese PPI had turned positive.”

Chinese PPI

And yet despite rising oil and Chinese producer prices, these rising inflationary pressures remain hidden in the data. From Nikkei Asia Review:

“The core consumer price index (CPI), which includes oil products but excludes volatile fresh food prices, slipped 0.4 percent in November from a year earlier, government data showed.”

Given that oil is up 40% YoY in Yen terms, I find it hard to believe that Japan CPI is still trapped in a deflationary spiral. In just another month, oil in Yen terms will be up 100% YoY.

The evidence points to a significant amount of government manipulation which obscures the simple truth, inflation is rising, and bond yields SHOULD be rising as well. Due to the government of Japan’s incredibly high debt load it is clear this cannot happen. The longer the BoJ’s yield curve control policy persists in the face of these inflationary pressures the more sinister the motives behind said policy are revealed. From Nikkei Asia Review:

“Prices of cars with 1.5- to 2-liter engines have risen further, to an average of 3.19 million yen, about 50% higher than a decade ago. Prices for compacts have risen about 30%.”

If we assume the BoJ’s objective is not to bring about higher inflation, which has already arrived, but to stealthily lighten the government’s debt burden it is likely that they will tolerate much higher inflation. I argue that such policy risks destabilizing the bond market as well as the economy it supports. From Nikkei Asia Review:

“The BOJ’s new policy framework aimed at keeping long-term interest rates around zero percent will help maximise the benefits of global tailwinds for Japan’s economy, Kuroda said.”

The BoJ is hoping to ride the combined inflationary tailwinds of higher Chinese inflation and higher oil prices that should prop up bond yields in developed markets such as the EU and the US. As interest rate spreads between Japan and these economies widen, the Yen should continue to weaken. The weakening Yen will exacerbate the rising inflationary forces and complicate the Japanese governments job of convincing their citizens that the yellow liquid falling from the sky is actually rain.

Japan is well known for its homogeneity, and yet one wonders how long they can keep this going. Which brings me back to this idea of the coiled spring that the BoJ continues to load. At a certain point, faced with a falling currency, rising inflation, negative interest rates, the spring will unleash its pent up energy.

“Shit escalates.” ~ Sevro au Barca, Golden Son a novel by Pierce Brown

“If you do not know where you come from, then you don’t know where you are, and if you don’t know where you are, then you don’t know where you’re going. And if you don’t know where you’re going, you’re probably going wrong.” ~ Terry Pratchet

My predictions for 2017 follow two simple rules, shit escalates, and it’s so crazy that it just might work. You’ll know which prediction follows which rule when you see it… Trust me, I’m from the government and I’m here to help.

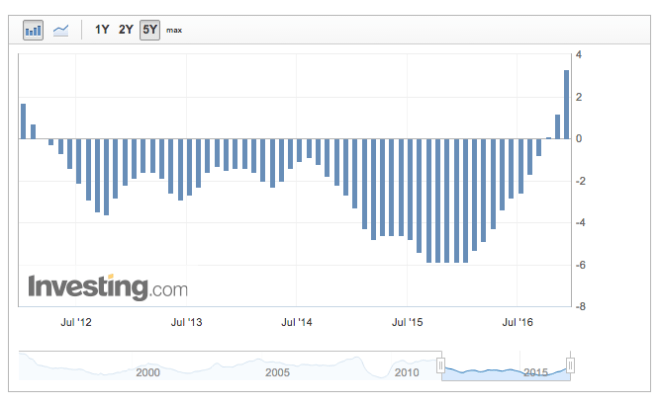

But as the wise Terry Pratchet once said we can’t make predictions for 2017 without discussing the disaster that was 2016. An obvious statement, and yet a necessary one. 2016 started off with consensus believing bond yields would rise to the 3% (at least in the US). But China’s unstable economy threw investors off balance in the January sell off. The middle kingdom’s economy, on the back of a super yuuuuge stimulus push, made a local bottom shortly there after.

Even though China’s economy bottomed, it still took months before it stopped exporting deflation to the rest of the world. And because China had been exporting deflation for so long, the market became convinced that deflation would continue in perpetuity. What the market and more importantly Central Bankers were missing was the fact that deflation in China had in fact bottomed, and although negative, was rising sharply.

Chart of Chinese Producer Price Index (PPI)

This turn from deflation to inflation also fooled Chinese investors who piled into the record low bond yields. In fact, investors’ response to these rising inflationary pressures was so slow that yields in China did not bottom until PPI had already turned positive (for the first time in over 4 years)!

Chinese PPI

And this is where things get very tricky for the Chinese authorities. They wanted this inflation. Just not this quickly. Locked in a deflationary debt spiral, a little inflation is a gift from the financial gods, BUT rip roaring inflation has the nasty effect of pushing up bond yields which in turn tightens financial conditions. And although we have not yet seen rip roaring inflation, China has gone from DEEP deflation to rising inflation within 12 short months. The Chinese Authorities are clearly aware of this shift, but it’s unlikely that they acted fast enough. The PBoC did not start tightening liquidity until a month before PPI turned positive.

It needs to be said, that by comparison, the PBoC is light years ahead of their western counter parts, the BOJ in particular. The BoJ pinned bond yields to the floor the same month that Chinese PPI had turned positive. But we’ll get to this later. For now let’s place our focus back on China where the PBoC has been tightening liquidity since September. Which brings me to my first prediction, which is more of a backward looking statement.

#1. We have likely seen the top in the Chinese bond market.

Philosophically speaking, a peak in bond values means that risk is growing. Given the predicament the Chinese authorities find themselves in, caught between Scylla and Charybdis, this would seem like a rather obvious statement. On the one hand, we have seen how little room they have to tighten before the deflationary pull of Charybdis overwhelms their economy. To reuse my Battle Of The Bulge Analogy:

“The Chinese government to use yet another historical reference, has engineered a counter offensive akin to the Battle of the Bulge in WWII. Right up until the battle it was perfectly clear that Nazi Germany was going to lose the war. Nazi Germany was quickly crumbling under the multiple fronts, dwindling resources, and Hitler’s repeated mistakes. And because of all of these “facts”, the Allies under estimated the Nazi Germany’s strength and paid dearly for it.

Nazi Germany threw everything it had into that battle and once it was over, the regime quickly crumbled less than four months later. Economic cycles last much longer than war cycles, so I’m not saying China is less than 4 months from collapse, but that once the stimulus fades, the economy will roll over hard and fast.“

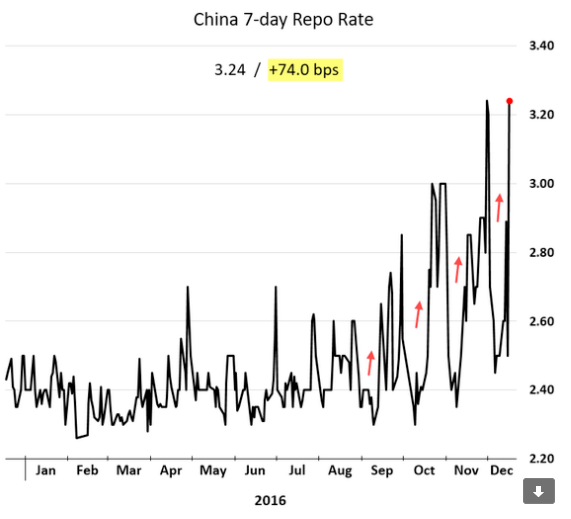

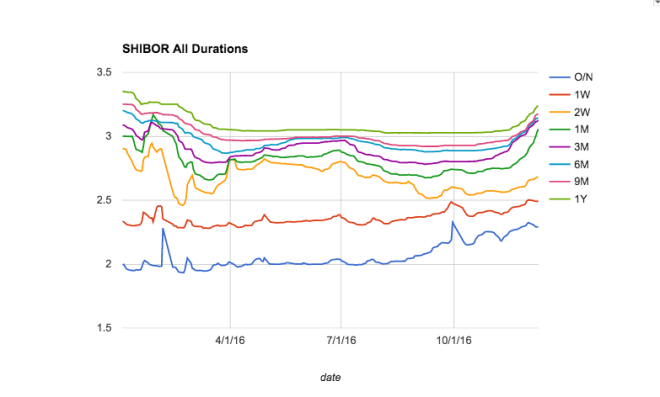

HIBOR is approaching levels last seen in the January sell off.

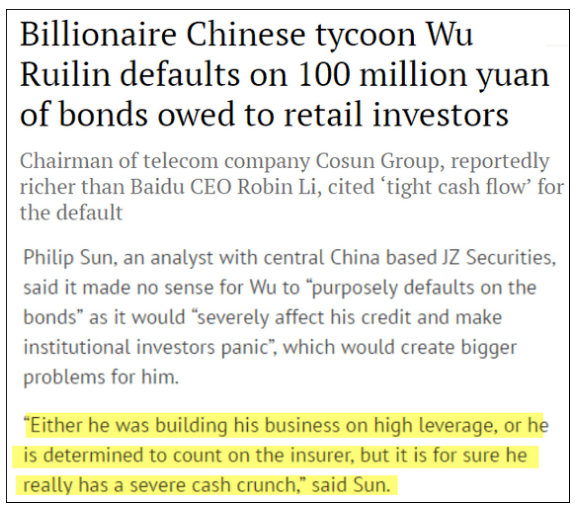

In fact liquidity is so tight that just recently, a MULTI-“billionaire” defaulted on just 100 million Yuan worth of debt. I use quotes, because anyone can be a billionaire if they borrow a few billion dollars and ignore the liability side of their balance sheet.

I’m sure he’s not the only one swimming naked. Wealth management products are incredibly susceptible to higher interest rates. These ponzi finance vehicles have increasingly invested in each other which has pushed counter party risk exponentially higher. From WSJ:

“Some 40% of the assets in wealth management products—the biggest portion—was invested in bonds as of the first half of this year, up from 29% in 2015, according to Moody’s Investors Service.”

This interconnectivity of WMPs has further restrained the PBoC’s ability to tighten. In spite of rising inflation, if the PBoC wanted to keep the economy going they would have to inject more liquidity… and that is exactly what they did. From WSJ (my emphasis in bold):

“On Friday, the PBOC tapped an emergency lending facility it created in 2014 to extend 394 billion yuan ($56.7 billion) in six-month and one-year loans to 19 banks. That pushes the net amount extended through the facility to 721.5 billion yuan so far in December, a monthly record, according to Beijing-based research firm NSBO.”

The Chinese government finds itself in a constant battle against short term destabilizing forces. Every time it tries to take its foot off the gas, the economy gets pulled in by Charybdis, prompting even more Cow Bell. I’m mixing metaphors but you get the point.

On the other hand, they can no longer stimulate as much as they want or else they’ll face, Scylla, the nine headed inflation monster that will rip their debt to shreds. It is quite likely that China has now reached the point where stimulus’ effect on the economy over the medium term is net negative. More specifically, more stimulus pushes inflation higher which in turn tightens liquidity and defeats the purpose of stimulating in the first place. My guess is that the recent monthly record of stimulus injections will show up in the inflation data much sooner than the Chinese authorities would like.

But why are they doing this? Surely they don’t believe this is sustainable? To once again use my Battle of the Bulge analogy, this time from the perspective of “the other side”.

This is a very interesting WW2 story "from the other side of the hill" https://t.co/e2AINlmDdv

In the article, a German tank officer is asked about what thoughts were running through his head before the now famous Battle of the Bulge.

The Chinese authorities may be trying to walk an atomically thin line but they still have hope. They can see the finish line! It’s just nine months away to the government reshuffling. They can surely make that. Right? Unfortunately, the German soldiers weren’t able to buy time for the full 3 months. The battle ended after just 40 days.

Which brings me to the thorn in the Chinese Authorities’ side, capital flight. For if there’s anything that’s going to derail the government’s plans it is capital flight. Thanks to increased stimulus fueling the weaker currency, rising inflation, and tighter financial conditions, capital flights has re-accelerated. Once again stealing from We Need to Talk about China:

“…to use yet another WWII analogy, the Yuan would be fighting a war on two fronts. Rising inflation coupled with rising demand for safety would only add more fuel to the dollar shortage inside China. This short period of strength the Yuan has enjoyed from tighter monetary policy is likely over. With the 7 handle in sight of USDCNY, FX reserves should deplete much more quickly and once again reenter back into the consensus narrative.”

This voracious demand to diversify out of the Yuan is exactly what we are seeing. From Bloomberg:

“A wealth management product from China Merchants Bank Co. in Shanghai last week, paying 2.37 percent annual interest on U.S. dollars, sold out in 60 seconds flat.”

Investors do not even care that this WMP is likely invested in a host of other WMPs nor do they care that inflation is already higher than the offered yield. For now dollar denominated WMPs may be the next gimmick to keep the ponzi-scheme going. There certainly is no shortage of demand here, from Bloomberg:

“In November, banks sold 49 percent more foreign-currency denominated wealth management products, most of them in U.S. dollars, than in October, according to PY Standard, a Chengdu-based wealth management research and ratings firm that tracks the data. November’s foreign currency deposits increased 11.4 percent from a year earlier, more than double the 4.8 percent rise in October, according to the People’s Bank of China.”

And of course, one only needs to look at the performance of bitcoin to get an idea of the state of Chinese capital flight. As of writing this article, Bitcoin crossed $900.

China has limited tools to fight this continued capital flight. Normally a country could hike interest rates, but the fragility of the Chinese debt bubble has proven this to be impossible. The other economic option is to grow fast enough in dollar terms to attract foreign capital. Given the debt, instability, and slowing economy, that is not likely to happen either. As of writing this article, Xi Jinping indicated that he expects the economy’s slow down to continue.

Nobody attacks this Chinese “stabilization” narrative better than Jeffery Snider. From Alhambra Partners:

“If you had proposed a stabilizing Chinese economy in the middle of 2014 it would have meant with IP at 9%, not 6%. And if you had done the same in 2010, as many policymakers and economists attempted, production would be growing at 13% not 9%. The Chinese economy, as the global economy, gets weaker not in a straight line but via clear, distinct episodes.”

So China is really left with just one option which is to close the capital account down, and restrict almost all outflows. This method has worked for as long as it hasn’t really worked. What I mean by that is as long as companies did not have trouble getting their profits out of the country, this was a viable strategy. But clearly capital was fleeing the country, likely much larger than the PBoC is willing to admit, thus the PBoC was forced to implement more effective (stricter) capital controls.

The problem with strict and rigid capital controls, is that they also hurt foreign businesses trying to do business in the country. As the business environment becomes more and more unfriendly, foreign and local companies will begin to pull back investments. From the WSJ:

‘”A majority of clients are currently consolidating and restructuring their China business,” said Bernd-Uwe Stucken, a lawyer with Pinsent Masons LLP in Shanghai. Some clients are closing down their business, with new investments being the exception to the rule, Mr. Stucken said.’

To make matters worse, these capital controls were also poorly implemented further compounding the falling faith in the Chinese economy. From the WSJ:

“Adding to the confusion: it is unclear where the limits are, because regulators haven’t published official rule changes, but instead have given only informal guidance to banks, according to Daniel Blumen, partner at Treasury Alliance Group, a consulting firm.”

I know this is already getting pretty long, so I just want to sum things up. China’s economy is slowing under an unbearable exponentially growing debt load with rising inflation that is almost sure to tighten financial conditions and counteract further stimulus. The currency is falling with no end in sight. Uncertainty in the country is high. One minute it will be too hot, the next too cold. The government has increasingly made it more difficult to do business through Draconian capital controls… At what point do you think corporations would take a step back and reexamine the situation and slow further investment? It may not be long before China realizes that the biggest risk to its economic stability is not too much capital leaving but not enough entering.

I almost forgot to mention another large source of capital flight, that the PBoC is currently unwilling to stop. From Bloomberg:

“That’s when a $50,000 cap on how much foreign currency individuals are allowed to convert each year resets, potentially aggravating capital outflow pressures that are already on the rise. If just 1 percent of China’s almost 1.4 billion people max out those limits, that’s an outflow of about $700 billion — more than the estimated $620 billion that Bloomberg Intelligence estimates indicate has already flowed out in the first 10 months of this year.”

The communist party has done a commendable job delaying the inevitable but 2017 will be the year where the cracks become to wide for even the guys on CNBC to ignore. Which brings me to my next prediction.

#2. USDCNY will surpass the mythic 8 level.

And given the correlation between Bitcoin and the Yuan, I will add a corollary to this prediction which is for Bitcoin to exceed the all time highs of $1200. Although I’m not exactly calling for gold/bitcoin parity but I’ll get to that later.

It is important to note that the PBoC can still inject liquidity into the system for a few more months before inflation reaches intolerable levels. But as long as Chinese Authorities prioritize short term stability over long term stability they, and by proxy the rest of the world, will suffer much higher inflationary pressures.

The developed world is not only ill-prepared for but almost completely ignorant of these rising inflationary pressures. At least the Fed is hiking and promising to hike even more. Unfortunately tighter Fed policy only compounds China’s capital flight problems. But what is the Fed to do? Given China’s inflationary path, they are likely behind the curve. From The Case For Higher Interest Rates:

“The Fed has been cornered for years, never able to unwind its policies without inviting disaster. The problem with being behind the curve is that the Fed will have to admit through policy that they made yet another mistake. If the Fed doesn’t react fast enough, inflation could rip higher pushing bond yields to intolerably high levels.”

The Fed’s addition of a 3rd rate hike in 2017 is likely to be a prelude to a much bigger admission. But that doesn’t necessarily mean that the dollar is about to rip higher.

Gartman: "the dollar is headed higher, dramatically so"

Although the three additional rate hikes haven’t fully been priced in, the market is now aware of the possibility. On the other hand, the market is currently unaware of any rate hike or tighter monetary policy from the ECB or the BOJ.

Although the ECB did taper.

ECBs Draghi: Message Is 'ECB Is Not Tapering, Will Stay In Market'

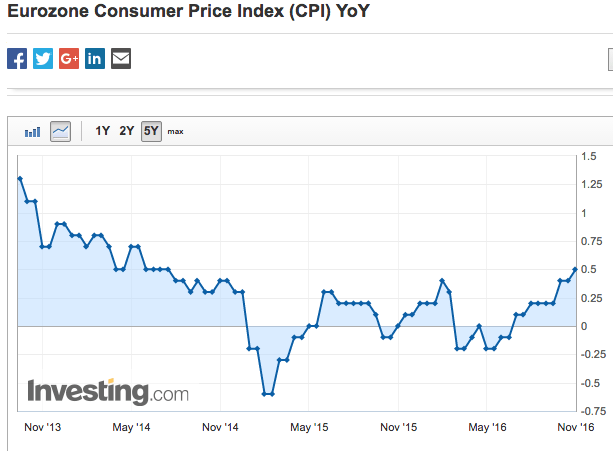

But remember those powerful inflationary forces that China is likely to export to the rest of the world? Well they’re coming to Europe and Japan, where rates are NEGATIVE. And let’s not forget that oil is up 40% YoY and soon to be rising. Recall oil was in the 20s into the end of January, $50 oil would translate into a 66% YoY move. Can you say, “HELLO inflation?”

Which brings me to the ECB’s CPI forecasts. If this institution had no power, and the “elite” people working there did not devote their entire lives to managing the economy based on unknown information, this would be adorable…

ECB’s Draghi: 2016 CPI Unchanged At 0.2% – 2017 CPI F’cast Raised To 1.3% From 1.2% – 2018 Seen At 1.5% From 1.6% – 2019 Seen At 1.7%

#3. The BOJ and the ECB tighten monetary policy, and potentially end NIRP.

In the face of rising inflationary pressures the ECB and the BOJ will be forced to tighten monetary policy. They may even consider using the opportunity as an excuse to end the mistake that is Negative Interest Rate Policy (NIRP), although that perhaps is more unlikely than it seems. Negative rates allow any debt level, no matter how high, to be sustainable. And these economies have too much debt. The only thing keeping them together is the same thing that is slowly killing them. So they may leave those foolish policies in place but still allow the yield curve to steepen tremendously.

Take a step back and recall the mood around European and Japanese banks back in the summer of 2016. Locked in a deflationary spiral, rates were negative and falling to new 10,000 year lows. The business models of the unfortunate banks trapped in these deflating economies were unsustainable and their equity reflected it. But if we get inflation and interest rates in these deflationary trapped economies begin to rise, that narrative vanishes faster than Keyser Soze.

#4. In a phoenix like turn of events EU and Japanese area banks rise from the ashes… only to be slain once more.

Come spring of next year, trend followers will be tripping over themselves to get a slice of these no longer “dead beat” banks. With their banks no longer in free fall, and rising interest rates, capital should flow back into these economies. Given the huge flows into US as of late, I suspect the EUR/USD carry trade is about to unwind.

With the BOJ and ECB unexpectedly tightening monetary policy, the Yen and the Euro should rise against the dollar.

#5. The dollar pause ain’t over…

It is important to remember, that US yields have already risen dramatically. This has dramatically tightened financial conditions in the US which has its own debt problems. The US consumer is already suffering from a financial tightening that it was not prepared for, and since the US consumer is 70% of the US economy, US economic growth should slow. European and Japanese economies and currencies should out perform expectations as they play catch up.

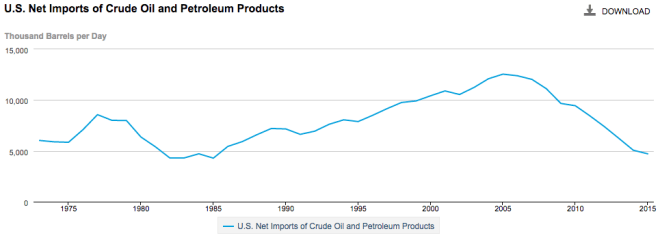

Before I get to the weak American consumer, I’d like to discuss, US shale. US imports of oil and petroleum products are one of the largest sources of dollar funding for the rest of the world. But since the advent of US shale, US oil imports has fallen by over 50%.

Combine the falling US oil imports with the falling dollar value of oil, it becomes quite evident that the US is not exporting the same quantity of dollars it once was. Because the dollar is the global reserve currency, foreign nations rely on additional dollars to fund and expand their economies. In the immediate aftermath of the GFC, the Fed made up this difference via its QE policies. But now due to the rising inflationary pressures, the Fed is tightening.

US shale is also increasing its output and locking that production in so that they can not only maintain these high levels of production but also better weather the next down turn in the price of oil.

With US dollar exports virtually flatlining since the GFC, combined with a much more hawkish policy from the Federal reserve, the amount of dollars flowing abroad is unlikely to be sufficient for developing nations to continue growing at the pace they would like. Trump’s protectionist policies if enacted will only compound these effects accelerating a short squeeze in the dollar. That is UNLESS…

The American consumer can step up to the plate and supply the necessary dollars to the global economy…

#6. Don’t be fooled by any dollar weakness the dollar bull market ain’t over.

The American consumer is tapped out and will not be able to supply the dollar funding the rest of the world requires. Real wages have not been nearly as high as advertised.

Facing a triple assault from higher mortgage rates, rising health care costs, and higher energy prices, the US consumer simply doesn’t stand a chance at supporting the global economy. Falling dollar liquidity globally will initiate a short squeeze and reignite the dollar bull market sometime in 2017.

Rising healthcare premiums made the headlines and may have turned the election in Trump’s favor. And although US shale has decreased US demand for foreign oil, the US remains a net energy importer. Higher oil prices will hurt the consumer more than it helps. Let’s not forget that natural gas bottomed in February of this year. This winter is already making out to be a cold one. Natural gas prices should rise higher, further pushing up the utility bill.

In the face of these rising costs, the US consumer has been forced to dip into their savings to maintain their standard of living. This trend is likely to be self defeating and reverse over the next few months.

And even though Americans dipped into their savings, they still slowed their purchases at restaurants, who have taken a double hit on falling margins and sales over the last quarter.

Next up on the weakening US consumer’s hit list is the auto industry. As @TeddyVallee puts it, one would be hard pressed to find a more favorable environment f0r US auto companies, and yet in spite of record discounts, low gas prices, and falling interest rates, sales fell.

Most attractive environment to grow volumes, yet they're negative. Seems to me there's a lot of opportunity in the sector. Where am I wrong?

It is important to note that this time last year, US shale was struggling to survive. Oil rigs were being cut left and right. Production was falling. Workers were being laid off. US shale in YoY terms should be a heavy contributor to GDP growth over the Q4 and Q1 2017. A resurgent US shale industry will likely do a sufficient job masking the underlying weakness in the US consumer. But don’t be fooled by a +2% GDP growth number in Q1, it will likely mark the high point in US GDP growth in 2017.

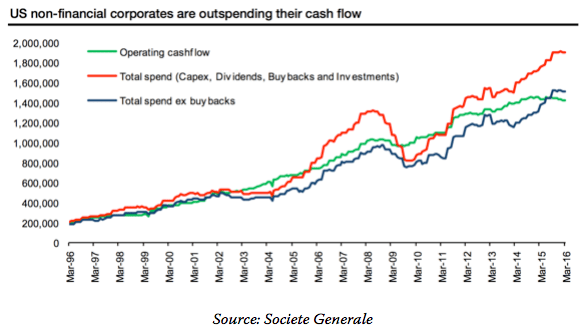

Of course, the American consumer isn’t the only one drowning in debt. US corporates have been taking on debt since 2011, and over the past two years have been spending all their profits on financial engineering gimmicks such as buybacks and dividends.

Higher interest rates will reduce US corporates’ ability to buy back stock.

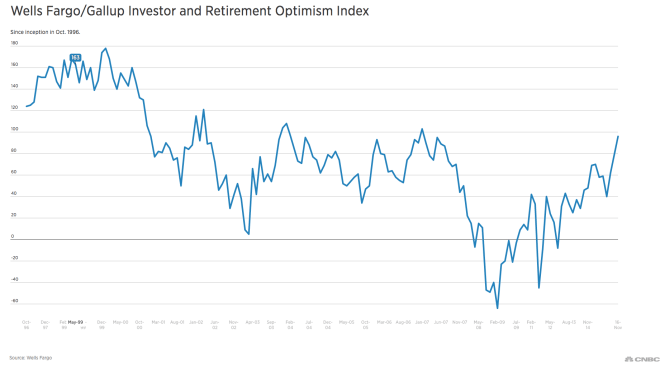

But if you thought a declining growth rate, declining buybacks, European capital flowing home, and a weakening US consumer would dampen investor euphoria you would be mistaken. Welcome to Trumptopia! Or as Admiral Ackbar likes to say, “It’s A Trap!”

Another sign of optimism just hit a record high. Who needs cash when Trump’s going to inflate it all away?

#8. The US equity markets will peak in 1H 2017, and in spite of any Trump stimulus will end the year in the red.

Now as much as readers would love for me to make a fool of myself predicting what the yellow metal/pet rock formerly known as gold will do, I will say that I haven’t a clue. But perhaps you should ask this guy.

Given government’s surging desire to ban cash, and tighten capital controls, it’s hard to argue against them. Which is why I’m not, just noting the shift of yet another demographic from bullish to bearish on the yellow metal. Although I’ll remind fellow bitcoin bulls to be wary of China no longer tolerant of capital flight, regardless of the form it takes.

China Said to Study Limiting Outflows Via Bitcoin as Yuan Drops : BBG

Back to gold. By the time a trend becomes an “official trend”, the major driving forces are no longer the major driving forces. And yet, the crowd still focuses on them with x-ray vision that cuts through the new driving forces. It is somewhere in this phase where the real forces driving the price could and do turn and yet the crowd is none the wiser because they are still focusing on the initial non irrelevant driving forces.

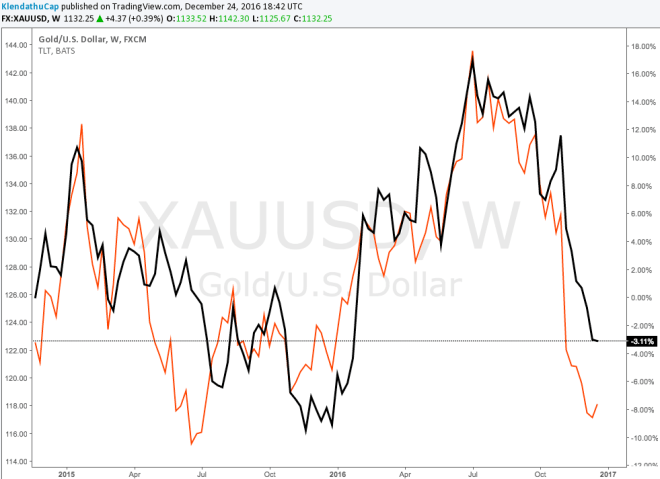

#9. Gold will break its correlation to nominal changes in interest rates.

Gold (rhs) in black, TLT (lhs) in orange

The major driving force of gold in 2016 was the addition of negative rates which prompted a deflationary state of mind. As bond yields approached the zero lower bound, and in some cases plunged through them, it didn’t make much sense to hold them over gold. Now that yields are rising, investors have jumped ship.

I expect yields in developed markets to move higher with inflation. But what if they don’t? What if rates in Japan and the EU remain suppressed due to a staunch commitment from the central banks? After all, they want negative real rates to deflate their very large debt bubbles.

If the authorities do not allow rates to rise, then the EU and Japan will be facing deeply negative real rates. Gold should do quite well in such an environment. And once again, if you consider a weaker dollar on the back of a slowing US economy into a rising inflation environment, gold could really shine… at least until the dollar begins the next of its bull market (see prediction #6).

Which brings me to my next prediction, which is actually more of a statement of fact than a prediction, which in turn gives me confidence that I will absolutely nail it.

No one does. My predictions are shouts into a howling wind. It is my hope that they have stimulated your mind and opened you to new possibilities.

To sum up, my 2017 Predictions are as follows:

#1. We have likely seen the top in the Chinese bond market. #2. USDCNY will surpass the mythic 8 level. #3. The BOJ and the ECB tighten monetary policy, and potentially end NIRP. #4. In a phoenix like turn of events EU and Japanese area banks rise from the ashes… only to be slain once more. #5. The dollar pause ain’t over… #6. Don’t be fooled by any dollar weakness the dollar bull market ain’t over. #7. The US Consumer Will Roll Over hard and the US will enter a recession in H2 2017. #8. The US equity markets will peak in 1H 2017, and in spite of any Trump stimulus will end the year in the red. #9. Gold will break its correlation to nominal changes in interest rates. #10. In regards to future events, I know nothing.

I think Inflationary pressures originating primarily in China with help from OPEC are quite likely to ripple through the global economy, catching investors and central banks off guard. This inflation surprise should destabilize markets in ways that even the great and powerful Klendathu Capitalist cannot predict (see prediction #10.).

I would argue that those inflationary pressures have already done tremendous damage to the US economy where the US consumer was already suffering under immense pressure from stagnant wages and rising energy and healthcare costs. Unable to provide additional dollar liquidity to the rest of the world, the global economy will slow and the dollar will begin the next leg higher in its bull market.

If it was not obvious, a large portion of my thesis hinges on higher inflation coming out of China. I would argue that inflation has been baked into the cake via excessive monetary stimulus out of China, but I could be wrong. I don’t believe there’s much of a chance of a muddle through for China though, and this is likely the biggest hole in my thesis. If China muddles through and is neither too hot nor too cold but just right, I could prove to be very wrong. But there’s another outcome, which I find much more likely than a muddle through…

If China surrenders to deflation then everything I’ve said is null and void. Prepare for negative yielding US treasuries. $2,000 bitcoin, and volatility… lots of volatility. If anyone is offering residency in New Zealand here’s my email: zegemabeach@gmail.com…

Just kidding…

But seriously, everything I’ve said gets thrown out the window in the event China decides to have a hard landing, although I’d argue that within 18 months it will be forced on them. I hate to end my predictions for 2017 on such a gloomy outlook, so here’s some cheerful war propaganda for ya! And to paraphrase Lieutenant Johnny Rico,

“Come on you Apes, do you want to invest forever!”

The inflation story has run too far ahead of itself. OPEC, China, and the “Trumpflation” narrative, the major drivers of this inflation, are all pausing at the same time. I know that I’ve been flip-flopping like a fish out of water as of late. But that tends to happen around a pivot point. And fortunately the markets have been kind enough to wait for me. I know guys like Jeffery Gundlach and Jesse Felder have been calling for this pivot a bit longer than I. And finally with a lot of struggling, I too agree. So let’s go through it all.

The Trumpflation narrative is on the verge of coming undone. His own party is prepared to fight him on his key fiscal issues. Which should translate into smaller deficits and lower domestic inflation both of which should push yields lower. To be fair, these are the same congressmen that allowed Obama to rack up $10T of debt in just 8 years. Given enough shoving they’ll likely go along, but that will take time. And time is something this narrative is currently running out of.

OPEC likely needs to prove itself before oil can sustain above $50 a barrel.The market priced in the cut before it happened, but failed to realize what $50+ oil would do for US shale. Rising OPEC production coupled with rising US production is hardly bullish for oil. Inventory builds are massive at the moment. Lower oil prices over the next few weeks should drag down inflation expectations as well.

Crude: +4.682 M Gasoline: +3.905 M Distillates: +0.233 M Cushing: +0.632 M

The PBoC has been tightening liquidity since October. Officials were/are likely worried about rising inflation and decided not to overheat the economy before the new year. They’ll likely turn the taps on in mid January for the Lunar holiday, but till then, deflation and risk off should will be increasing at the margins.

With China tightening till January, OPEC not cutting till January, Trump facing significant political opposition and speculators massive short US treasuries, we could be in for a significant short squeeze in US treasuries.

So if tell you, US yields are set to go lower compressing interest rate spreads between JGBs, the Yen would strengthen. And once you think the Yen is about to strengthen a whole host of trade opportunities become available. Because I’m driving to Texas this weekend (which makes this my last post for the next week), I’ll suggest the most obvious, gold. Gold looks due for a nice bounce.

Actually, I’ll give you another. Once the Fed hikes, and pushes short term rates higher, imagine what the yield curve will do with the long end falling? We could see a much flatter yield curve in just a few short weeks. Bank stocks, the darlings of the FOMO crowd could come under heavy fire.

A real benefit from my constant flip flopping, is that I now have a much better perspective on two sides of the inflation story. At risk of getting ahead of myself, I believe this next move will be nothing more than a counter trend move. I believe that China will once again open the spigot, OPEC and Russia will actually cut production, and Trump? Well Trump ain’t passing so much as a grape salad let alone a massive stimulus bill with the US is growing at 2.5%. US shale may hide the deteriorating US consumer for another quarter or two at most but soon it will be obvious the marginal buyer in the domestic world is no longer there. But at this point, that’s beyond the time horizon of this move.

My biggest concern for this rebound thesis is that the Chinese authorities over estimate the strength of their economy and tighten too much. As a China bear, my bias shows here, but I still think it is something to watch out for. OPEC might also fail to cut, but I doubt it, as they say in the talkies, “there’s no turning back”. Seriously could you imagine how stupid it would be for them to go back now, after US shale hedged a record amount of its production! Odds of that happening are SMALL.

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.

Head fakes, it’s a theme I’ve been trumpeting a lot of late. The rising inflation story I have said multiple times is a major component of this theme. Already fund managers have shifted to this rising inflation story, and the multi-year high in US 10 year reflects this thinking.

And perhaps the move in US yields has gone too far, but I’ll get to that later. Overall, I think the rising inflation story is not yet over. I may be a long term bond bull, but for now, I think higher inflation coming out of both China, and OPEC will lead to higher interest rates in the developed world, particularly in Europe.

OPEC has successfully pushed the price of oil much higher than it was a year ago. There of course has been much talk about how ridiculous the optics of their agreement looks but I think it is important to ignore the snarky Zerohedge headlines and focus on the actual price of oil. On a YoY basis we can clearly see that oil is pushing +50%. Bond bulls ignore this at their own peril.

OPEC production hit a record high this November, which certainly doesn’t bode well for a successful cut. At the same time, it looks to those on the surface, that OPEC is ceding defeat in its war with North American shale. And they are but that doesn’t mean they don’t have a plan. Russia recently sold a stake in Rosneft to Glencore (a Neutral Swiss Company) and Qatar’s SWF (OPEC). The deal was also financed through Russian banks to further integrate the two sides, OPEC and Russia.

With this bit of news, the OPEC production cut, in my estimation, has gone from an act of desperation to a smart gamble. OPEC+Russia now produces half the world’s oil, making it a much more formidable cartel. A cut of 10% of their production would amount to over 4 million bpd, the likes of which North American shale could simply not keep pace with.

But I’m not suggesting they do that all at once. This new cartel will likely take the Federal reserve’s approach of slow and steady moves. IF this first relatively small cut holds and by that I mean the price of oil stabilizes somewhere over $50, I could easily envision a scenario when as early as this spring we see significant chatter of a future cut that could come this summer. In essence, the cartel would force the market to price in additional production cuts before they even happen. OPEC+Russia production future production quotas could become the new Fed dot plots.

It must be said, that this is still a gamble. And like all gambles, this one is not without its downside. OPEC + Russia have acknowledged the power of North American shale, and will have ceded significant market share to them. IF there is another downturn in the price of oil due to a demand shock in the form of a global recession or something to that effect, this new cartel will find a much more resilient North American Shale industry than the one we saw in 2015 and 2016 which is saying something. In such a scenario, the price of oil could easily fall way below the lows we saw earlier this year.

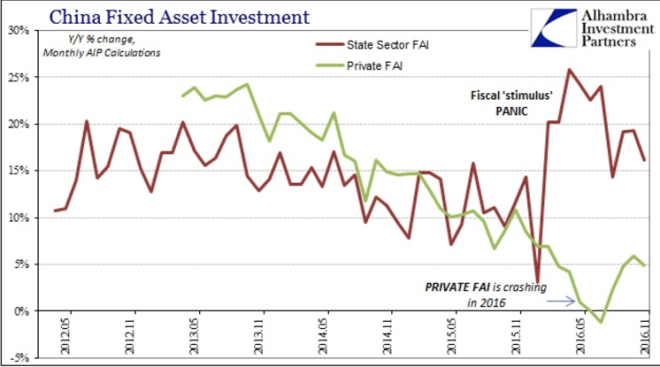

But for now I don’t foresee an imminent global demand shock. In my previous article, We Need To Talk About China, I discussed the implications of China goosing its economy long enough so that it will make it to the government reshuffling next fall. It is important to watch state investment in RoC terms which should continue to decline into the winter months, and could put significant pressure on this thesis. China has to be very careful here and realize just how fragile their economic counter attack has left them. Meanwhile the private sector showed a modest improvement, but most likely will not come even close to carrying the load necessary to get China to the government reshuffling.

China's state sector still doing most of the shovel work, but private sector showing modest improvement pic.twitter.com/suUXFzWdsG

In order to cross the finish line, state investment in the commodity heavy enterprises will have to continue to be the major drive of Chinese economic growth which should continue to push inflation higher. The Li Keqiang index has sharply rebounded from record lows earlier this year, and is likely to continue to remain elevated for at least the next few months.

OPEC + Russia combined with China’s inflationary policies should have a huge impact on European inflation which had already bottomed and had been trending higher throughout the year.

A lot of folks are calling for EUR/USD parity, and I am one of them. But perhaps the timing of that call may be a little bit further out than we anticipate.

BAML: Long USD’ is back to being the world’s most ‘crowded trade’ by far

I remember in the summer staring at this obviously dead end currency with an insolvent banking system scratching my head to as why anyone would use this multi-colored paper for anything other than kindling. But now I’m going to offer a different perspective.

One of Europe’s most glaring problems is its insolvent banking system. The banks cannot lend because the yield curve is as flat as a pancake that was thrown in a NIRP hole. The European bank business models were supposedly dead in this environment, and they were… But inflation is rising and with it the long end of the yield curve is set to go much higher and the banks will be able to breathe a temporary sigh of relief.

Given these rising inflationary pressures, one might think the ECB would be all hands on deck, but the ECB is a monolithically slow and reactive institution that will not be able to turn the ship in time. Draghi has only just announced the smallest of tapers while extending the duration of QE. FFS a three toed sloth on more quaalude than The Wolf of Wall Street has faster reflexes than these guys.

ECB’s Draghi: Inflation Outlook Not Very Different From Start Of Programme

The ECB will still be pumping QE into this inflationary environment. Now you can make a very good argument that the ECB is not buying bonds to push up inflation, but maintain the low borrowing costs of the insolvent nations that make up the EU. And this is quite valid for it has certainly helped suppress Euro area sovereign bond yields and contributed to the the record spreads between US and European sovereigns.

U.S. Treasury yields are the highest on record relative to similarly-dated German notes. pic.twitter.com/wYfS9K07Qm

This ridiculous mis-pricing in European credit over US credit is even more insane when one looks at Italian bonds. This is the same economy where 20% of its loans are non-performing.

The most absurd chart: #Italy's 10y yields trade below US 10y yields despite Debt to GDP ratio >30% above US's & Italy's banks in crisis. pic.twitter.com/NqwVLhqxPp

But then you must consider the ECB’s credibility is at stake and the market will be more than happy to serve these technocratic sloths their much deserved humble pie. Imagine inflation hitting 1.5% over the next few months with an accelerating trajectory. In spite of the ECB’s QE, long term rates could begin to rise, and we would start to hear rumblings of a potentially accelerated taper out of the ECB further pushing rates European sovereign rates higher.

At the same time, US rates may have gone a little too far too fast. The Trumpflation narrative appears to be on the verge of tipping over. Yet again it bares repeating, from my recent post, It’s a Trap!:

“Donald Trump much like Alexander Hamilton has promised drastic change in a time of hidden crisis. To these men it was clear that the final battle had not yet been fought, but the majority of the population did not share their sentiment.

In order to win the election, Donald Trump successfully united a diverse group of people and yet he didn’t win the majority vote. And although the republicans may have won congress, Donald is hardly a republican president. Donald Trump is akin to a battle commander who has charged too far ahead of his troops. He will need to wait to gather the army before he can launch an effective attack.”

Lo and behold the Republican establishment is now prepared to fight him on his stimulus package and tax cuts. Of course these are the same folks who rolled over for Obama as he added $10T in debt in just 8 years.

The fact remains, that expectations of US fiscal stimulus have gone too far and will have to be reigned in considerably as reality sets in. This should translate in significant downward pressure on US yields which once again should further tighten the record spreads between US and EU sovereigns.

A lot of what I have discussed, will also have tremendous implications for Japan but that is for another post. For now, I’d like to end this post with a chart. This time, of the wonderful EUR/USD that has staunchly held the 105 line for over the past 2 years now. I believe it will one day break, but not today, and not very soon. As you can clearly see, RSI momentum has diverged from the overall trend. If we do see a stronger Euro, like most the recent moves, this will be something to fade. #HeadFake

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.

And if you said this life ain’t good enough

I would give my world to lift you up

I could change my life to better suit your mood

Because you’re so smooth

Despite the 6.7% growth, 2016 has not been a good year for China. I’ll be the first to admit that I do not fully understand why Xi is waiting for the government reshuffle next fall. In spite of the smoothest GDP growth in economic history, I find it hard to believe that higher debt levels, smaller FX reserves, and rising shadow bank risk will be any more manageable under a regime where he has “full” control.

Fortune favors the bold, and although Xi has boldly secured power for himself, he does not deem it sufficient to combat the problems he faces. And maybe he is right, maybe he lacks the required strength to do what is necessary, but that inaction speaks volumes about the efficacy of the Chinese government. Maybe Xi is like Alexander Hamilton who I alluded to in a previous post:

“Alexander Hamilton had already mapped out the future republic of the United States at the close of the revolutionary war in 1783, but it wasn’t until 1787 that the US Constitution was actually created and it would take another 2 years after that for it to finally be ratified.

Donald Trump much like Alexander Hamilton has promised drastic change in a time of hidden crisis. To these men it was clear that the final battle had not yet been fought, but the majority of the population did not share their sentiment.

… Donald Trump is akin to a battle commander who has charged too far ahead of his troops. He will need to wait to gather the army before he can launch an effective attack. I have little doubt that Donald will bring about much needed change in time, but rescinding some executive orders will only tickle the status quo.”

Is Xi too far ahead of his time? Perhaps he is. Clearly there are sizable vested interests blocking his path. I don’t think it is a lack of knowledge of the problems, but the way in which to combat them without upsetting the status quo. But the status quo is part of the problem, and is what Xi seeks to change. Xi likely feels the best way to change the status quo is to change the people in power through bureaucratic means next fall.

Of course, there is another, less kind analogy one could use, and the truth is probably somewhere in between, but I think General George McClellan of the American Civil War, might prove to be a more apt analogy. Like General McClellan during the American Civil War, Xi is waiting for full strength before launching an assault. With the hindsight of history, we know that McClellan bungled multiple opportunities to end the war in its first year if he had acted more decisively.

Obviously Xi will not be able to solve China’s problems nearly so quickly. China’s credit boom and its solutions will echo through the decades, but unlike McClellan’s predicament, where the South’s capacity to form and equip an army was much more limited, debt and risk in China are growing exponentially. By the time Xi’s armies arrive, the enemy is likely to be the largest and most powerful force in economic history. Defeating such an enemy will be nigh impossible, One must not miss the irony of this analogy, for should Xi fail, he risks starting the very thing McClellan failed to end – civil war.

As poetic as that all sounds, I have a lot to learn about Chinese politics and perhaps should dedicate my time this winter to such books (I am happily taking any recommendations). So it’s best to take my analogies with a grain of salt and enjoy them for what they are, an introduction into the quagmire that is China’s economy.

For now I feel forced to assume that the Chinese government will do everything in its power to maintain a “stable” Chinese economy till at least the fall. Their recent policy moves have indicated as much. 2016’s global shopping spree of Chinese billionaires and companies has led the government to institute a freeze on future deals lasting right up until the fall reshuffling. From the WSJ:

“The new controls, once in place, are to remain in effect until the end of September and thus are intended as a temporary tool to stabilize outflows ahead of a major reshuffle of the top echelon of the ruling Communist Party late next year, the people familiar with the matter said. That’s in keeping with other efforts by Beijing to try to keep the economy on an even keel before the leadership change.”

Consensus believes Beijing will keep the economy stable up until the leadership change. Although I do agree that outcome has the highest of available probabilities, I think that those odds are falling. Trump has thrown the “One China” policy on the bargaining table, as well as the Yuan and pretty much everything else. He may be relatively soft on Russia, but he’s going hard on China. Or to steal from Quentin Tarantino,

“You devalue the Yuan in your dreams, you better wake up and apologize.”

An obvious problem with this strategy is that China is fragile. The Chinese economy relies on increasing amounts of foreign capital to keep its economy going. When that does not come in, the central authorities must provide. In essence, China cannot give Trump what it does not have. But perhaps, the reason why Trump is hammering them from the get go is because of these apparent weaknesses in both the economy and Beijing’s power structure.

After the reshuffling in the fall, Xi will be far less likely to acquiesce to any of Donald’s demands. For once Xi has his power, it is assumed that he will begin instituting much needed change. Those changes very likely will be detrimental to the short stability of China, and indirectly the United States.

Once again, Trump may be smarter than people think, by pressing China now, he reserves “the right” to blame them for US economic woes during his term if and when Xi decides to stop sacrificing China’s long term stability. Until then, China needs to stop capital outflows, maintain its economy for the next 9 months, and keep Donald Trump at bay. Welcome to the new golden triangle.

Maintaining the Yuan has proven exceptionally difficult of late. China continues to add new laws and regulations that have increasingly hampered the economy and done little to staunch capital outflows that have once again started to rise.

How popular is investing in China going to be if companies can't send dividends back home? https://t.co/7KzGSIH7Up

— Blume Industries CEO Balding 大老板 (@BaldingsWorld) December 7, 2016

“Several European companies in China have been unable to remit dividends abroad following the introduction of new exchange controls, the first indication that Chinese attempts to curb capital outflows are causing problems for foreign businesses. The EU Chamber of Commerce in Beijing said the payment difficulties experienced by European companies were “disruptive to business operations”. “

The Chinese government now risks hurting foreign investment into the country if corporations cannot bring their profits home. This is coming at an especially trying time for the nation as private investment has been on a downward trajectory for the past 5 years. Despite the massive stimulus from the central authorities, the private sector has not been convinced in a recovery whatsoever.

The most important chart I have seen in months. It explains so much – the January selloff, the pivot, EM/commodity rally pic.twitter.com/4Qhxl5AxjU

The image above, as The Long View states, is quite powerful. The Chinese government to use yet another historical reference, has engineered a counter offensive akin to the Battle of the Bulge in WWII. Right up until the battle it was perfectly clear that Nazi Germany was going to lose the war. Nazi Germany was quickly crumbling under the multiple fronts, dwindling resources, and Hitler’s repeated mistakes. And because of all of these “facts”, the Allies under estimated the Nazi Germany’s strength and paid dearly for it.

Nazi Germany threw everything it had into that battle and once it was over, the regime quickly crumbled less than four months later. Economic cycles last much longer than war cycles, so I’m not saying China is less than 4 months from collapse, but that once the stimulus fades, the economy will roll over hard and fast.

I will admit that I drastically underestimated the Chinese government’s resolve. And when their backs were against the wall, they released an economic blitzkrieg likes of which we have never seen. Unlike the two month Battle of The Bulge which oddly enough started in mid December, the results of this blitzkrieg are still playing out almost a year later. The most obvious of which is rising inflation. I made note of this inflation in previous posts “Weekly Review: Would You Like To Know More” and “It’s A Trap!“.

“2016 was a lost year for the Chinese economy and yet the leaders in Beijing continue to believe that they control their own destiny. But as they continue to close down other channels of capital outflows, it risks trapping this inflation in China and further destabilizing the country. As Julian Brigden’s model shows, China in less than a year has gone from deep deflation to surging inflation.”

In response to this dramatic shift from deep deflation to ripping inflation, the Chinese government has been forced to tighten liquidity.

The long end of SHIBOR has exploded higher, and will likely go much higher before this is over. After all who would lend for a year at less than 3% if inflation is pushing 5%?

If the Battle of the Bulge analogy holds, the Chinese economy will roll over much harder and faster than consensus and even the central authorities anticipate. The market could shift from a risk-on inflationary environment to a risk-off – inflationary environment quite quickly.

In this scenario, to use yet another WWII analogy, the Yuan would be fighting a war on two fronts. Rising inflation coupled with rising demand for safety would only add more fuel to the dollar shortage inside China. This short period of strength the Yuan has enjoyed from tighter monetary policy is likely over. With the 7 handle in sight of USDCNY, FX reserves should deplete much more quickly and once again reenter back into the consensus narrative. With that said, I’d like to thank Bloomberg News for their wonderfully timed article.

And once again, as the Chinese economy is set to slowdown, the Fed is about to hike interest rates. It seems a bit myopic to suggest that the world is about to witness a 2016 January sell off redux, but the similarities are too hard to ignore.

With just 9 months to go, Xi can practically see the finish line. At this point it is a forgone conclusion that the central authorities will go above and beyond to do what is necessary to get the economy there. What I am worried about, is that rising inflation will make it quite difficult if not close to impossible for the stimulus to have the desired effect.

Too much stimulus and they risk fueling the inflation further which would raise interest rates and actually tighten liquidity. Too little stimulus, and the economy looses momentum and descends into the deflationary spiral their economic Battle of the Bulge was meant to delay. We’ve already seen the Australian economy start to hit the skids. There are many financial bubbles riding on China maintaining their economic stability.

Although I have my doubts, there still remains the possibility that China will able to successfully walk this line. If that is the case, the rest the world should expect much higher inflation going forward.

I’m going to save the consequences of higher inflation for another post entirely. If you’d like to know more, follow me here or on twitter. For now, China is in a big heap of trouble. They are proven masters at the game of can kicking and perhaps should not be bet against, but at the same time, even if they are successful they will likely push inflation into the parts of the world that are most unprepared for it. I for one look forward to watching Trump try and dance on the tight rope with them.

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.

“If you need a deal badly, you’ll get a bad deal.” ~ Louis-Vincent Gave

It’s taken OPEC over a year to get this production cut in place. And like past cuts, this one too is riddled with flaws. It’s only for 6 months. Indonesia dropped out. Saudi Arabia was forced to admit defeat. Libya and Nigeria are set to erase at least half the cut in the next year. The list goes on and on.

For those of us who enjoy the hindsight of history, it’s been fun to watch OPEC do battle with the shale revolution. The slow march of technology occasionally moves further and faster than many anticipate. OPEC, like John Henry has been forced to learn this lesson the hard way.

This deal will serve the shale producers in North America much more than the citizens of OPEC. Producers are rushing to hedge their production for the next 12-18 months, so in the next oil price downturn, when OPEC is forced to flood the market, they’ll find a much more resilient North American shale industry. I am very bearish oil. I think we’ll see oil in at least the low 30’s sometime in H2 2017.

On the flip side, OPEC has managed to prop up the price of oil. This time last year oil was in the 30’s. I think there’s a good chance OPEC will be able to maintain the price of oil above $45 for the next 2 months. Which means on a YoY basis, inflation is likely to pop even more than it already has.

Bonds will not have a good time. What I’m looking to do is hedge my long term short oil thesis with a short term short bond position, particularly EM bonds. With the sell off in bonds as strong as it is, I wouldn’t be surprised to see them correct a bit and offer a better opportunity from the short side.

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.

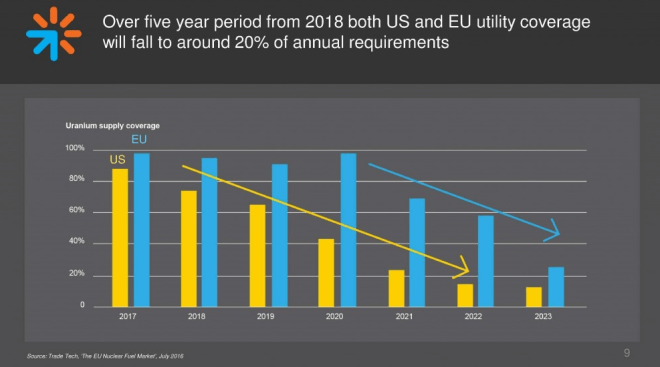

“No one goes there anymore, that place is too crowded.” – Yogi Berra

Did you hear that the long-term and spot prices of Uranium hit +11 year lows last month? Of course you didn’t. Unless you follow me on twitter that is. Hint, hint. Wink, wink. I’m just kidding but seriously, uranium, I’ve been talking about it so much lately the government is probably monitoring my data.

This sector has been left for dead, eaten by radioactive Chernobyl wolves, pissed on by a drunk drifter before finally being lit on fire for warmth by the very same drifter. And just in case anyone forgot why this sector has been left for dead, as of was writing this blog post, Fukushima was hit by yet another earthquake and tsunami (Yes I’ve been working on this post for that long… and yes some times you can’t kill your darlings).

According to World-nuclear.org, Uranium energy demand is set to grow by over 15% over the next 7-10 years. On the surface 15% over 7- 10 years doesn’t sound like a lot but as any resource investor knows, timing is almost everything. And in this case uneconomical prices have shuttered future production and the amount of uranium under contract is about to fall precipitously over the next 7 years both of which should amplify the impact of the relatively small 15% demand growth.

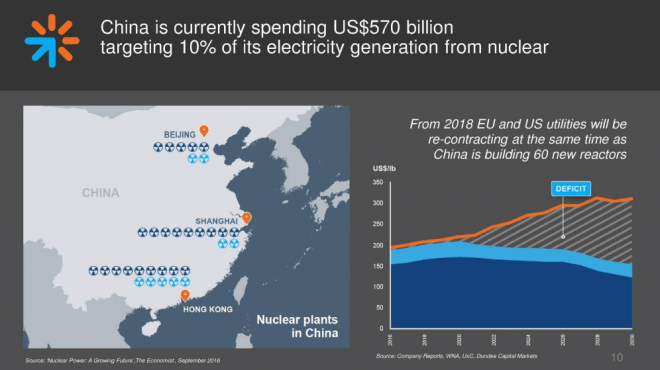

Let’s not forget that China has shown time and time again that it puts a high premium on securing resources for itself. China has acquired massive stockpiles of iron ore, copper, oil and any other resource it sees as strategically important to its interest, with its push to go green and reduce pollution you can bet that uranium is on that list. Chinese utilities will be looking to acquire uranium for their reactors under construction as well as the hundreds of GWs of reactors still in the planning stage. As utilities the world over rush to lock in lower prices, we could see a significant short squeeze.

Of course that’s all been known for a few years now. It is the emergence of President Trump that may have thrown a curveball into the uranium story. Although I think the “Trumpflation” narrative is ridiculous, the spike of inflation is real. OPEC’s production cut will certainly add fuel to that rising fire. Investors are now forced albeit temporarily to consider the impact of inflation on their portfolios, which could serve as a useful catalyst for hard assets such as uranium and uranium miners.

But perhaps more importantly, Trump has shown he’s more than willing to go the extra mile to keep jobs in America.

US uranium production has fallen since the 80’s and never got back up. Since Fukushima, US mines have been hit particularly hard and have been forced to shutter production entirely. But those mines are still ready and permitted to go if the price is right, or if a certain person in power offers the utility companies a deal they can’t refuse.

US imports roughly 90% of its uranium. Domestic production near all time lows. That could change under president Trump. pic.twitter.com/jp8kpYTEE9

Trump wants to keep jobs in America, develop the US’ natural resources to become energy independent and above all he needs “shovel ready” projects to do it. It’s hard to imagine a better project that fits so nicely into all those overlapping Venn Diagrams. Not to mention the overall cost of uranium ore as percentage of a nuclear power plant’s total costs is about 1% so any political pushback for rising energy costs will be minimal. One can practically imagine Alan Rickman rising from the grave to say,

“You asked for miracles Donald, I give you uranium.”

As I have just shown the fundamental case for US uranium miners is quite strong. But timing a bottom in any market is incredibly difficult. The resource market is notorious for luring investors over trap doors and false bottoms. With that said, the technical set up on some of these American miners is starting to look quite interesting.

First up is Energy Fuels Inc (EFR). The share price seems to have found a bottom while lurking underneath the calm water RSI momentum has taken off.

We see a similar divergence on the weekly chart as well.

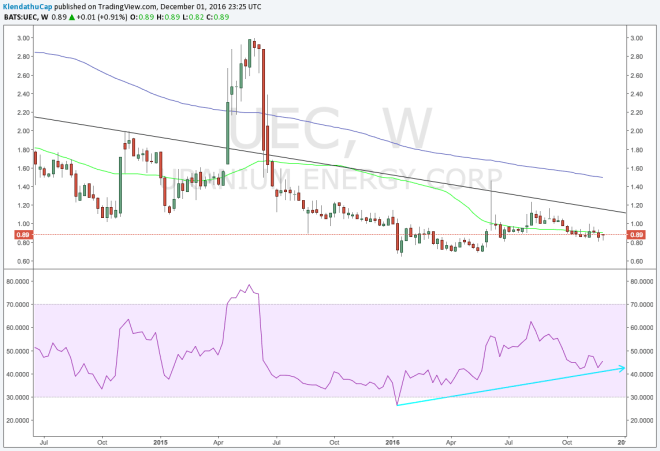

Moving on to Uranium Energy Corp (UEC), the pattern is not as clear on the daily…

… But the weekly looks quite lovely.

Disclaimer: I own shares in both EFR and UEC. This post is not advice to buy and or sell securities. If you act on the words of an unaccredited twenty something millennial over the internet you have only yourself to blame.

“But given said speculation and the Yen’s refusal to go higher, it’s quite possible USDJPY is bottoming here at the 100 level which just so happens to be the 50% retracement of the 2012-2015 move. As demonstrated multiple times through out this post, I have my doubts, but it is best to remain open near such key inflection points.”

“But given said speculation and the Yen’s refusal to go higher, it’s quite possible USDJPY is bottoming here at the 100 level which just so happens to be the 50% retracement of the 2012-2015 move. As demonstrated multiple times through out this post, I have my doubts, but it is best to remain open near such key inflection points.”

“Between Elon Musk promising to consume the world’s current production of lithium ion batteries and China pretty much outlawing internal combustion engines by the year 2020 lithium demand is set to take off. Just last year Chinese sales of Electric Vehicles (EVs) increased 223% and a 4 fold increase from 2014.”

“Between Elon Musk promising to consume the world’s current production of lithium ion batteries and China pretty much outlawing internal combustion engines by the year 2020 lithium demand is set to take off. Just last year Chinese sales of Electric Vehicles (EVs) increased 223% and a 4 fold increase from 2014.”