Global interest rates are on the rise. Those who have feared earlier in the year that Central Bankers were “cooking” the goose by keeping their accommodative monetary policies on hyper driver are being proven correct in their initial assumption. People like Jawad Mian, and Julien Brigden have been arguing that the (probably local) bottom in commodity prices we saw in January/February of this year would come back to bite the central banks in their derrières. It seems we are seeing exactly this.

To understate this important shift that has happened in the past few months cannot be understated. Just a few months ago, following the BREXIT, the world was no longer concerned that interest rates would ever rise. In fact, investors were panicking because they thought rates would never rise again! Unsurprisingly, rates started rising shortly after said consensus was reached.

Investors were buying bonds of longer and longer and duration because those bonds were rising in value fastest. Now that inflation has rebounded (albeit temporarily), these bonds are getting hit the hardest. With long term risk free rates rising, all other assets will have to readjust.

So far, what I’ve said is nothing new. Anyone with a couple charts on government bonds could easily tell you as much. And anyone falling the markets for the past year or so will tell you that the best way to make any money would be to front run the momentum, and as of right now the momentum is pushing yields higher. OPEC’s talks of a production cut have only added fuel to the fire (pun intended).

But lost in these recent moves are the larger, and more powerful forces at work pushing government bond yields lower. Perhaps most important of these forces is China’s slowing economy and the capital flight that follows.

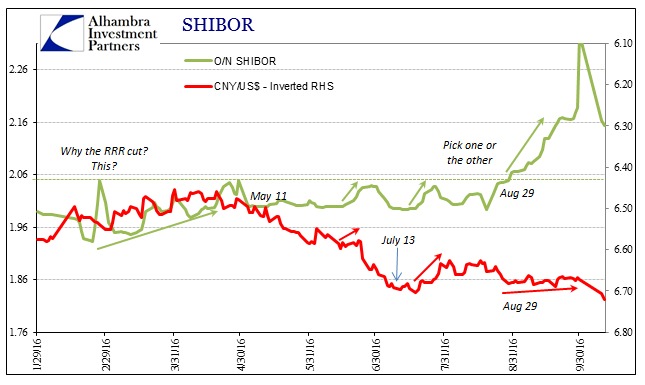

In past articles, I have made a number of strong comments regarding any Yuan weakness but it is important to note, that the recent weakness in the Yuan is mostly due to re-surging US Dollar strength.

But perhaps even more importantly, even though the Yuan is not weakening against every other currency, the effect remains the same – capital flight has started to re-accelerate and officials are starting to panic.

https://twitter.com/WorthWray/status/792708280363601921

Perhaps the purest way to trade Chinese Capital flight is to buy Bitcoin, which has rallied back above $700. As Chinese Authorities clamp down on other forms of capital flight such as insurance fraud, bitcoin will become an increasingly attractive form of capital flight.

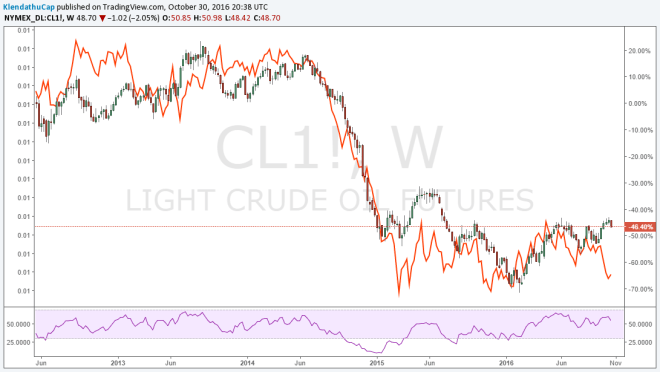

As capital flight accelerates out of China, the Yuan should continue to weaken and more importantly the dollar will strengthen. A strengthening dollar will eventually weigh on the price of oil, and other commodities. Right now the inverse of the DXY (orange) and WTI are on a break, but like and Ross and Rachel they always get back together, and with the dollar set to go higher, their time apart seems quite limited. And of course that’s not including the unlikely chance of an OPEC oil cut, which although beyond my expertise seems quite unlikely. If I’m wrong, US shale will have my back to cap any oil gains at around $60.

Falling commodity prices will reinforce the deflationary trends that have been present since 2012. Which brings me back to US and global interest rates. I view the current sell off in bonds as a buying opportunity and not a top. This +35 year trend in falling interest rates is not yet over especially in the US which is still viewed and will continue to be viewed as the world’s safe haven. I still have a small position and will look to add on to it. The US 10yr getting above 2.00% would represent a strong buying opportunity, IMHO.

Now although the risk free rate of interest may be headed, lower that doesn’t mean risky corporates borrowing costs will come down, specifically junk rated corporates whose borrowing costs have fallen tremendously from the February blow out. And these bonds which are already very illiquid are held in an increasingly smaller share of hands:

The top five investment companies hold $264 billion in US high-yield bonds, according to a big report from Stephen Caprio and Matthew Mish at UBS. That’s equivalent to 20% of the market.

The top 20 hold $605 billion, equivalent to 46% of the US high-yield market, and mutual funds and separately managed accounts hold 70% of the market.

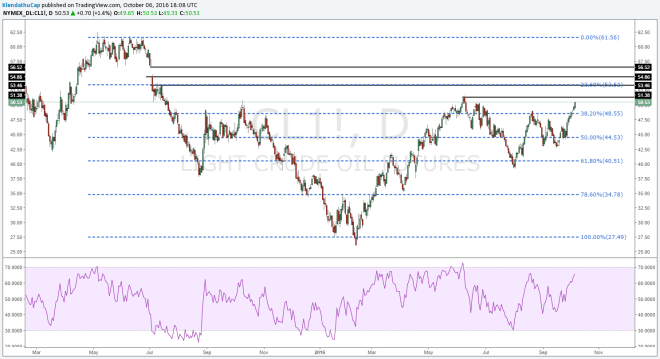

The US corporate junk bond market has become a land mine waiting for something to set it off. Potentially the biggest explosion will come from the oil companies which have benefited both from the reach for yield as well as OPEC’s misguided attempts to push oil higher. If OPEC disappoints their credit and equity looks incredibly vulnerable. Negative momentum as XLE struggles around the 38% fib retracement level from the 2014 highs does not bode well for these stocks.

A lot of these companies took on a lot of debt to maintain their dividends so yield starved investors would buy them without checking what’s going on under the hood.

As junk rated debt sells off and their cost of borrowing rises these companies could get hit extra hard.

In the end, there seem to be a lot divergences going on in the markets and yet prices haven’t adequately responded. Perhaps the clearest sign of this divergence: IMF president Christine Lagarde is calling for a December rate hike.

https://twitter.com/WorthWray/status/791552101453135872

Given just some of the risks I’ve mentioned in this post, a December rate hike seems like a very bad idea, unless you actually want to crash the global economy…

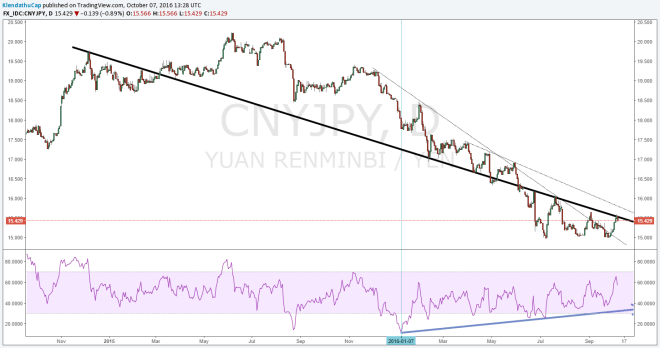

As to why this weakness is occurring, I leave you with a quote from

As to why this weakness is occurring, I leave you with a quote from