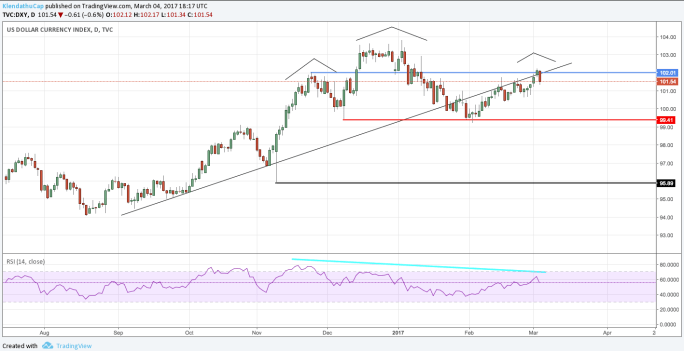

The dollar story is a very interesting one. As the global monetary system’s reserve currency the dollar does not behave like any other fiat currency. The history of other monetary systems typically lasts around 40 years. At 46 years, our current post-Bretton Woods system (beginning in 1971), is old, rickety and fraught with danger. These instabilities have created powerful structural forces that have propelled the dollar higher. The most recent episode was the 2014 rising dollar story that crushed oil and other commodities as well as the Emerging Markets that depend on them.

These forces are still at work. They haven’t gone away, and neither have the bulls who are aware of their presence, no matter how far in the background they may be. I consider myself in this camp, but at the same time, as I indicated in the previous sentence, I believe these forces to be mostly hidden in the background, waiting to be thrust again into the light.

On the other hand, I see a confluence of bearish dollar forces at work. Despite the amazing soybean quarter of 2016 which almost puts TSLA’s Q3 “positive cash flow” to shame, US GDP growth has been sub 2%. Q1 2017 is likely to come in under 2% as well.

It is important to note that these two quarters will have taken place before the effects of rising interest rates and the stronger dollar will be fully felt. These sub par GDP numbers also include the incredible growth we’ve seen from the US shale industry. Is some other US industry going to magically contribute to GDP going forward? It is hard to imagine a scenario where US economic growth will surprise to the upside.

And yet the Fed still finds reasons to hike interest rates. Janet Yellen, looking through her rearview mirror points to the fantastic economic strength we’ve seen in the larger foreign economies.

First off, China does not look as healthy as Janet Yellen’s rearview mirror suggests. The GDP growth target in China has fallen to 6.5% and, more importantly, M1 growth has rolled over which suggests China’s best days are now behind it.

Part of the readjustment in China’s growth is due to the unstable nature of the country’s real estate boom. Xi’s approach to a tighter monetary policy and more stable growth should slow the real estate boom and have far reaching effects for not just China’s economy but commodities and Emerging Markets as well.

As for Europe and Japan, yes it is true their economies have responded positively to the reflation trade. Because these economies have been trapped in deflation the longest, it makes sense to see them be the largest beneficiaries of inflation (at least in the short term). Eurozone’s PMI is at its highest point in over 5 years.

We haven’t seen a Japanese PMI this positive since Abenomics’ heyday in 2014.

Meanwhile, warning signs have piled up in the US, and the ISM manufacturing survey despite being elevated could peak as early as this month.

But we know the real reason the Fed is prepared to hike. The global reflation trade has certainly given Janet and her ilk a false sense of comfort, but the odds of a fed rate hike were incredibly low until a week ago.

That is, until The Donald gave his State of the Union address.

There was no US economic news between mid February and now to suggest such a rapid rise in March rate hike odds. Trump spoke, and the Fed panicked. If everything Donald said was in fact going to happen and at the pace he implied, the Fed would have undoubtedly fallen behind the curve. But is Trump really going to get the things he desires as soon as he suggests? From my November blog post, It’s A Trap!:

“In order to win the election, Donald Trump successfully united a diverse group of people and yet he didn’t win the majority vote. And although the republicans may have won congress, Donald is hardly a republican president. Donald Trump is akin to a battle commander who has charged too far ahead of his troops. He will need to wait to gather the army before he can launch an effective attack.”

However, eloquent and well spoken his State of the Union address may have been, it is of vital importance to realize that Trump does not write the bills. Trump does not pass the bills. The fractured and incompetent Congress does. A large portion of Democrats are still sore from “their” loss in November, and are opposing Trump on every issue imaginable. Meanwhile, the Republicans are split between a Border Adjusted Tax, repealing Obamacare, and a number of other issues. Republican Senator Rand Paul hasn’t even been allowed to see the current bill.

https://twitter.com/darth/status/837352088556359680

Trump’s stimulus is further out than the market and more importantly the Fed anticipates. It is more likely that the Fed is hiking into weakness than strength. Speaking further to probabilities, it is likely that the March rate hike will mark the peak in Fed’s hawkish stance for the year, and yet Hedge Funds are positioned for further US economic strength and inflation.

Somewhat paradoxically, funds are also incredibly long commodities.

The long dollar and long commodity trade is also known as the reflation trade. Rising global growth pushes up demand for commodities, which props up prices which in turn pushes up inflation thereby leading to a rise in bond yields. US bond yields rise higher than those in EU and Japan due the QE and NIRP policies further propelling the dollar higher.

But the reflation trade is not only old and well known but perhaps most importantly is likely turning. As I believe the origin of the reflation trade is found in China (not Trump), it should worry these reflation bulls that China’s economy is slowing not accelerating. It should be even more worrisome that the Fed is hiking not because of improving Chinese economic data but Trump’s rhetoric. From my post The Reflation Trade:

“But investors have become so accustomed to the US driving the global credit cycle that they have missed the origin of the reflation trade. The dollar, commodities and inflation have all risen together for the first time in over a decade which has left investors scrambling for a narrative to explain this paradox. Fortunately, the recent US presidential election has provided just that. Despite the “coincidence” of commodities bottoming with China’s economy in February of last year, investors have latched on whole heartily to the “Trumpflation” narrative. “

The base effects from reflation should peak this month (the data from February is released in March). The Fed with its well polished rearview mirror should fall hook line and sinker for the inflationary data just as it is peaking. Meanwhile growth from the EU (if the specter of Le Pen disappears) and Japan could surprise to the upside while the US lags. Going forward, we should expect Fed dovishness, not hawkishness and dollar weakness not strength.

DISCLAIMER: This blog is the diary of a twenty something millennial who has never stepped foot inside a wall street bank. He has not taken an economic or business course since high school (for which he is immensely proud of) and has been long gold since 2012 (which he is not so proud of). In short his opinions and experiences make him uniquely unqualified to give advice. This blog post is NOT advice to buy or sell securities. He may have positions in the aforementioned trades/securities. He may change his opinion the instant the post is published. In short, what follows is pure fiction based loosely in the reality of the ever shifting narrative of the markets. These posts are meant for enjoyment and self reflection and nothing else. So ENJOY and REFLECT!

Pingback: Mirror Mirror On The Wall: Is The Reflation Trade About To Fall? – The Klendathu Capitalist