In the latter half of 2014 and all of 2015 I was a firm believer that US interest rates would either fall or not rise significantly, which I thought made for a safe investment opportunity with limited downside. However, a lot has changed over the course of 2015. The strengthened dollar has put pressure on commodities and EM economies. Cracks big enough to draw media attention are forming in the US economy and with the Fed embarking on its first rate hike cycle in 11 years, I think it’s a good time to reassess my position.

The dollar sharply rose through the first half of 2014 and before peaking in March of 2015. Expectations for lift off were as early as April, but the Fed successfully pushed the date back another eight months, and with it, the dollar stalled. But now the Fed is finally hiking interest rates. And if the dollar strengthens from here, an already high plateau, the knock on effects for the rest of the world will be quite noticeable.

The dollar will most likely rise in 2016, and the Fed hiking interest rates is just one reason why. History shows that in a currency war, the country who eases wins. And right now the Fed isn’t easing. It’s tightening, which is going to slow down the economy as exports become less competitive and the debt burden becomes too great.

And of course the US still has to deal with the shale fiasco. Remember, not many US shale companies have gone bankrupt yet. Production has only fallen about half a million bpd. The US added on close to 5 million bpd during the shale boom. This time bomb hasn’t detonated and yet low oil prices are hollowing out some sectors of the American economy.

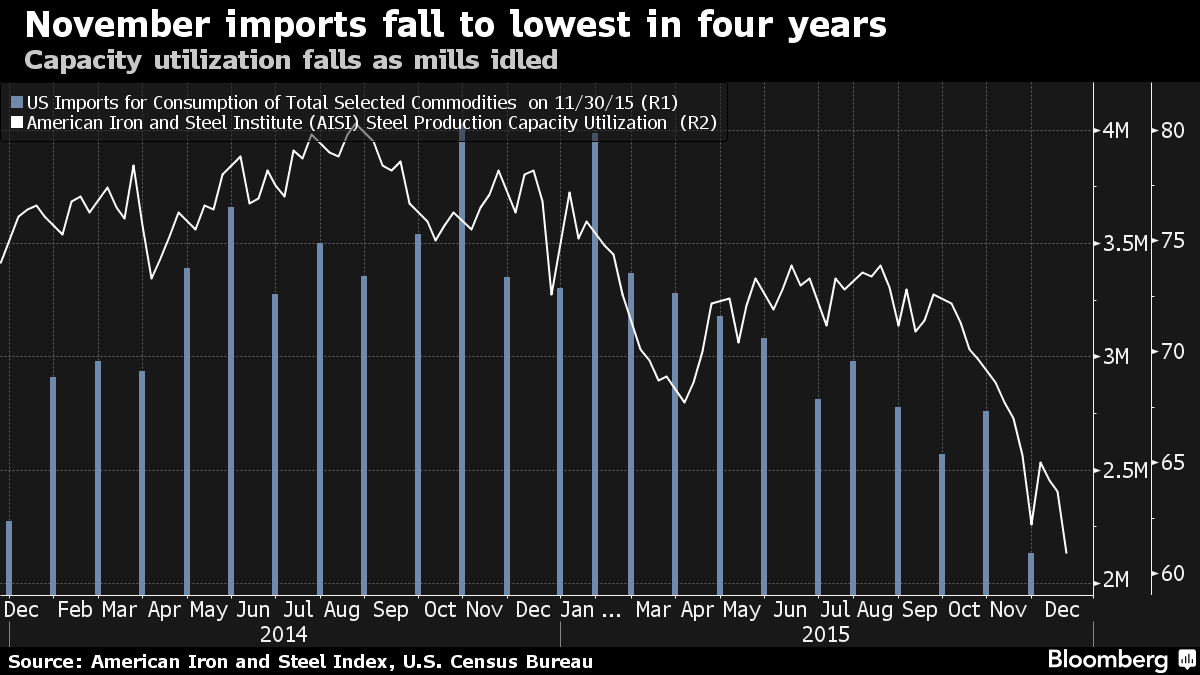

US steel production capacity has dropped from a high of 80% in 2014 down to just above 60% in December. To make matters worse, it’s actually still falling with no rebound in sight. Steel imports are also down for the year. Remember, when the Fed told us back in January how falling oil prices was not only “transitory” but also a net benefit for the economy. I’m so glad these guys are some of the most powerful people in the global economy.

The US economy is slowing down just as the Fed is hiking rates. As demand falls, the US will send less dollars abroad which makes dollars in the foreign markets even more scarce, thereby making it harder for foreign nations to get their hands on them. Once again, taking the Fed’s rate hike as another drain on dollar liquidity, the outlook for dollar liquidity does not look good. But there is hope. President Obama can increase the size of government like it’s nobody’s business. Surely he will step up to the plate and spend a poop ton of extra money to keep the flow of dollars to the global economy going strong. Yeah he’s got that… Like totally…

Oh… Oh Darn. President Obama is set to run the lowest deficit of his tenure. At time when the world needs all the dollar funding it can get, the US government and the Fed are essentially telling the rest of the world to get the turkey out of the fridge.

There’s going to be a huge deceleration in global dollar liquidity, which could directly lead to a bit of a run on the dollar. As the dollar becomes more scarce and more valuable, demand for the green paper will rise. Thus the dollar will strengthen in 2016. Some of the implications for such a move will show up in my next post on the US treasury market.

When people look at back and wonder when the Fed should have hiked, even though I don’t think there ever would have been a “good” time, but there was certainly a better time. The response will be: would you rather hike interest rates when global dollar liquidity is rising at an accelerating rate or when it’s falling?

To its credit, the Fed has set up standing swap lines with five central banks: Canada, Switzerland, England, Japan, and the ECB. Which means that during times of a lack of dollar liquidity, the Fed can swap trillions of dollars for trillions of yen or euros etc and these nations will have the necessary dollars to prevent a systemic collapse. However, you will notice that the Fed has no such lines with any Asian countries, in particularly China. I’m not saying we are headed straight for a currency crisis. I’m merely pointing out that demand for dollars is outstripping supply in the global economy, which is very bullish for the dollar.

Now China lies at the very heart of collapsing commodity bubble. Its economy has slowed greatly as overcapacity, malinvestment and a high debt load weighs on the country’s ability to transition from exporter to consumer. As the dollar strengthens so to does the Yuan, which hurts China’s exports because its trade partners are all devaluing their currencies against the dollar and the yuan.

Canada, Australia, and New Zealand have all cut interest rates in 2015. Since the dollar bull rally began in mid 2014, the three currencies are down 23% against the Yuan, and that’s including the Yuan’s recent devaluations. This currency mismatch is forcing China’s economy to transition too quickly away from its exports. Thus the PBoC will devalue the Yuan, to stabilize exports, while not losing too much purchasing power in the process since China produces a large percentage of its own goods and services. However, such a devaluation could have a tremendous impact on dollar liquidity in Chinese markets.

For over a decade, the Yuan was a one way bet against the dollar. The idea, borrowing lots of dollars, and paying back with cheaper dollars was very enticing to Chinese companies. That is until, the party ended in late 2013 . Ever since, the dollar has been on rising in jumps and fits against the Yuan, and the PBoC have been holding on for dear life. With the dollar set to head higher in 2016, we now find that a lot of Chinese companies are on the wrong side of the boat, waiting for a wave of devaluations to capsize them.

In the long run, the devaluations are massively deflationary for the rest of the world as they seek to export their own deflation which would bring down US bond yields. However, in the short run, until the PBoC widens the trading band, they will be forced to sell treasuries in order to defend the Yuan.

Like the Yuan other currencies pegged to the dollar could be in jeopardy. Saudi Arabia receives most of its dollars from selling oil. The price oil has forced Saudi Arabia’s hand. In order to maintain the peg, without enough oil dollars, Saudi Arabia must sell its dollar denominated assets such as treasuries and or equities. I discussed in my previous post why a Saudi unpegging is unlikely, and therefore expect this pressure to be for the long term or until oil prices rebound substantially.

Now the Fed owns $2.5 trillion in treasuries but they ain’t selling. Not for a looooooooong time. And just like that $2.5 trillion, in mostly long term bonds are taken off the market. Which means liquidity in the treasury market falls, leading to bigger reactions to smaller moves. Thus countries dumping treasuries to defend their currencies, combined with a Federal reserve trying to force people into higher rates puts enormous upward pressure on US interest rates.

But in the end, the Fed’s recent actions may be misguided and misinformed. US growth both in the private and public sectors is slowing down. The dollar liquidity is shrinking in the rest of the world at a time when they need it most. Which brings me to the final chart.

Central banks that have tried hiking interest rates have all been forced to backtrack. Japan who isn’t even on this list, has hiked rates multiple times in the past 20+ years and we all know where their interest rates are. And given the Fed’s so ridiculous it would be funny if it weren’t so depressing track record I believe they will too be forced to lower interest rates by early 2017.

In the end, I think the treasury market is a tale of two time horizons. Short term there seems to be a lot of forces pushing rates upward in the US. Foreigners are selling treasuries. The Fed is raising rates. But long term, the dollar will rally, the chinese will devalue, the US will slow and the Fed will be forced to ease. A scary thought is we could see a multi decade high in the dollar on the back of record low interest rates. If that happens, I’ll probably sell both. That’s it for now.