For better or for worse the oil markets have captured the world’s attention. Multi-decade low oil prices have a way of doing that. Everyone knew there was an imbalance that needed to work itself out, and although the market seems to believe the worst of the turbulence is behind us, I still believe there are future air pockets ahead.

Back in January, most people myself included believed Saudi Arabia’s main goal was to crush US shale, however, at the Doha Saudi Arabia showed its true colors. It seems there was general consensus among the oil ministers of OPEC, but Saudi Arabia stood out from the pack unwilling to compromise unless Iran froze.

Which to be honest, was a ridiculous proposition. Iran has the most spare capacity of all the OPEC nations and is only just ramping up production and with foreign investment set to pour into the country future production capacity is set to rise even further. Delaying all of that with a freeze makes zero sense, especially considering that oil revenues on a relative basis to Saudi Arabia are almost inconsequential.

Perhaps one of the more interesting surprises of the meeting was Prince Mohammed Bin Salman’s threat that Saudi Arabia could flood the oil market with 1,000,000 bpd of oil at essentially the press of the button.

This is a very credible threat. The Saudi Prince’s ability to efficiently make quick decisions with little resistance has drawn the attention and jealously of leaders around the world. I can only imagine how Xi is watching and thinking “if only I had that power”.

The Prince has very smartly changed the incentive structure in Saudi Arabia. Instead of subsidizing everything from water and food to electricity and oil which hides the real cost of these goods, the kingdom has decided to give the value of these subsidies directly to its citizens, who now know the actual market cost of these necessary goods.

The obvious result is less wasteful spending. Whatever oil the Saudi people don’t consume Aramco exports. On the margin this is increasing, further adding to Saudi oil exports. Throw in the expansion of the Shaybah oil field that will add 250,000 bpd, the young Prince’s threat is looking quite credible.

Whether or not Saudi hits its target of an additional 1,000,000 bpd is not the point. The point is, Saudi oil exports are increasing. As is Iranian production, if only they could get the ships necessary to export, we’d really see a huge drop. And with the rising oil price, US shale companies have been able to hedge their production at profitable levels.

All of this points to another down move in the price of oil. How low do we go? I don’t know. Back in January I argued that Saudi should cut prices and increase production at all costs to kill off a sizable chunk of US shale once and for all. Unfortunately, that didn’t happen and you can see in the chart above, there’s been a significant increase in hedging. Although a lot of these companies still carry too much debt and the next down move will probably kill off a lot of weaker ones and finally put a big dent in the multinationals whose share prices have been quite resilient in the face of this record decline in oil prices.

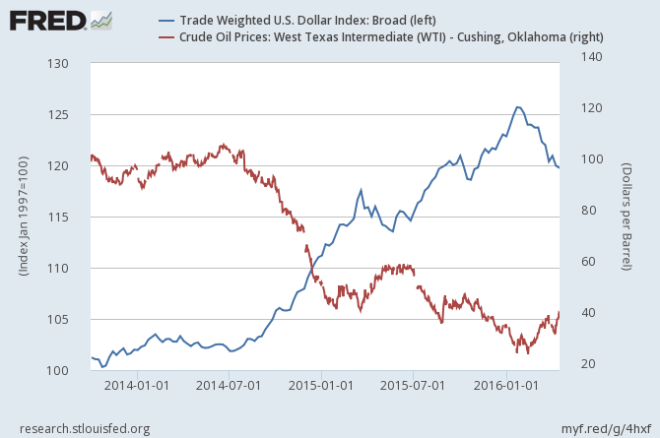

Unbeknownst to most investors, supply and demand mechanics aren’t the only thing driving the oil market. Of course, you guessed it, I’m talking about the dollar. Looking at the chart below, you see oil started to fall as the dollar started to rise. And then as the dollar peaked in January of this year, oil bottomed at $26.50.

I believe that the dollar’s rise is not over. Not by a long shot. We are in a consolidation period that will probably end by early July at the latest, if not much sooner. The mechanisms for this rise and their explanations are for another article. The point is, if the dollar resumes its uptrend, then oil will fall.

Lastly speculative positions in the oil futures market are coming off record levels. When you combine that with the fact that producers are actively increasing hedging, you see that the speculators in record numbers are on the wrong side of the boat.

With all that said, I think WTI over $45 makes for a very good short and would continue adding shorts on the whole way up to $50. Once again my time horizon is till early July for oil to start its down move. If it hasn’t happened by then, I would need to reassess my position. I don’t know how low it would go from here, and there are certainly a whole litany of variables that need to be taken into account, arguably most importantly is any central bank maneuvering such as Fed rate hikes or BoJ kamikaze money printing. But I think the trends, and positioning are on my side and will be watching closely to see how this all plays out.