Countless times have I stated that global leaders are operating on a very thin tightrope. The risks should they fall are asymmetric to the downside. But just because the odds are against them, doesn’t mean they will fail.

I believe there exists a very particular albeit unlikely set of circumstances that could stabilize the global economy for the rest of the year. With market participants expecting a significant correction sooner rather than later (myself included in this group), this particular set of circumstances could be a nightmare for people like us.

What are these “circumstances”? Well they certainly aren’t highly attuned reflexes, expert krav maga technique, next level marksmanship, in-depth knowledge of the criminal underworld and sheer determination to save his only child from the Albania mafia.

I believe that the world economy could stabilize if the following conditions are met:

- The Yen and Euro weaken against the dollar.

- The dollar weakens against commodities and EM currencies.

- Emerging markets rebound accelerates into sustainable growth.

- The US economy stabilizes on the back of a weaker dollar.

- China continues to delay any real adjustment.

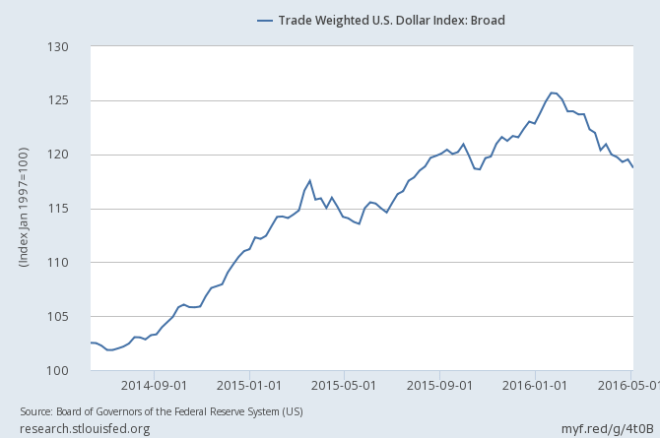

As you can tell, a lot of this scenario depends on what the dollar does. The dollar has to strengthen against the Yen and the Euro to prevent a deflationary spiral from consuming their respective economies. At the same time the dollar must weaken against emerging market currencies to prevent a further unwind of the $9 trillion dollar denominated carry trade and a rebound in commodity prices as well as an deceleration of capital outflows from China.

So how does this actually happen?

Since mid 2014, the global economy has been over shadowed by the effects of a rapidly rising dollar.

Commodities were pummeled taking emerging markets down with them. US growth slowed as credit conditions tightened and the strong dollar dragged down corporate earnings. China struggled under its debt and continued to slow down in the face of expanding credit growth. None of these events are positive for growth going forward.

However, a lot has changed. Since late January of this year, the dollar has fallen back to mid 2015 levels, allowing for a loosening of global liquidity and return to growth in emerging markets. As emerging markets rebound, we could see an increase in global demand. The result of which would be higher commodity prices. Higher commodity prices could alleviate stresses and deflationary pressures in China.

Most importantly, oil may rebound as well off the back of higher emerging market demand, large production cuts from inefficient producers and supply disruptions from various nations. Thus the seemingly mortal blow that oil producers thought was once dealt may now be finally healing leading to high paying job growth in the US and greater dollar liquidity as more petrodollars flow through the system.

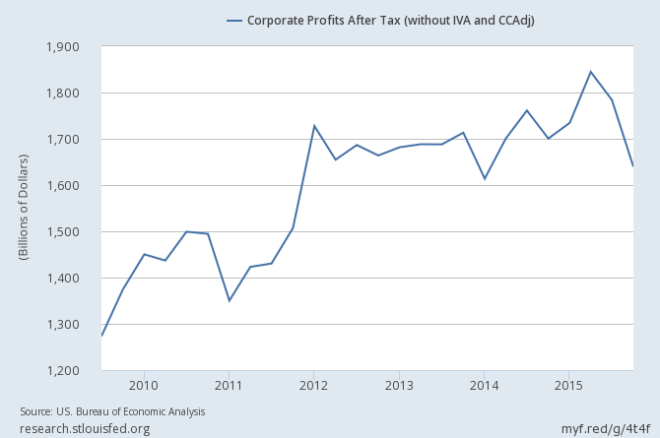

As hinted above, the impacts for the US could be quite huge. With a weaker dollar, the US can export more to higher demanding EMs. The weaker dollar would also give US corporations a breather and perhaps stabilize the recent descent of earnings which peaked last year.

With growth stabilizing in the US, the dollar could strengthen against the EU and Japan while their NIRP and QE policies continue to weaken their currencies. As I suggested in a previous article Japan may also increase its fiscal deficit allowing the BOJ to monetize this extra debt, which would help dispel rumors that the BOJ is running out of bonds to buy. This could also lead to a pick up in demand for Japan and perhaps finally with the help of higher commodity prices lead to the first real signs of inflation in decades.

The big themes here are higher commodity prices. Stronger EM economies and currencies. Weaker Yen and Euro. Stronger than expected US growth. All of these positions have rallied significantly off the February lows which makes going long any of them considerably less sexy. With everyone on oneside of the boat, one year call options on the S&P are quite cheap and offer an interesting way to play such a scenario. The market is certainly not anticipating this bullish scenario which makes it cheap and perhaps necessary to account for in a portfolio as bearish as mine.

My portfolio consists of the following positions (in order of size):

- LONG – precious metals and their miners

- LONG – cash (in dollars)

- LONG – US treasuries

- SHORT – US equities

- LONG – A specific Uranium exploration company (NXE.cve)

- LONG – Lithium miners

- SHORT – Canadian Banks

It’s a simple portfolio that has worked quite well this year. I like to take the Stan Druckenmiller approach of putting a lot of eggs in one basket and watch that basket very closely.

I don’t have the luxury of 50 analysts and another 50 hedge fund managers and another 50 research firms that I can call at a moment’s notice to get their opinion on intimate details about specific economies around the globe. Neither do I have a Bloomberg terminal to get specific information on every little economic detail at the press of the button although I find their website sufficient.

The point is, I don’t the technical knowledge or access that the big guys do. I like to keep things simple, identify major trends, position myself early and wait. The bull case I outlined here is something of an unexpected surprise that may last 12-18 months and at the same time decimate most of the holdings in my portfolio.

Higher than expected inflation would kill my long us treasury and cash positions. Higher than expected EM demand coupled with a re-surging US economy would kill my short US equities and Canadian banks positions. Hard to say what would happen to gold, but if fears of a global recession faded the price of the yellow metal could take a heavy hit.

Needless to say, in a 6 months my portfolio could go from looking near genius to incomprehensibly stupid, and that is exactly why I decided to discuss the bull case today. Fear is a powerful motivator, and one should never be fully comfortable with their positions.

There you have it. A bull case for growth. That wasn’t hard. Now it’s time to rip it to shreds.

![]()

If the Euro and Yen do not weaken against the dollar then their banking systems will be destroyed by the deadly cocktail of deflation, NIRP, a flat yield curve and over regulation. The EU aka Germany for better or worse will not allow on an expansion of fiscal deficits which could temporarily help stabilize the currency bloc via the expansion of more credit. Without the ability to generate new credit in the system, their economies will simply collapse on themselves.

Despite the best efforts of governments and central banks the world economy has never been more interconnected. The major European banks are vital to the system’s health. Their inability to generate credit growth and remain profitable is a systemic issue for the global economy that has yet to be addressed. And no I don’t count Italy’s $5B bandaid for a $100B bullet hole as addressing the issue. These weak institutions must not be allowed to fail. Thus the Yen and the Euro at the very least have to weaken against the dollar to stave off annihilation in the short term.

So the dollar must strengthen against the other funding currencies while paradoxically weakening against EM currencies. Although I outlined that as a possibility if EM growth picks up, I do not find it likely, and even if it does occur let me outline the dangers of such a scenario. If EM demand accelerates from here and successfully pushes up commodity prices as the Yen and Euro weaken, what happens to inflation in Japan and Europe?

Well inflation goes higher… much higher (on a relative basis). With spiking inflation what happens to all those wonderful government bonds with negative yields? Who in their right mind would pay a government to borrow money while that money is also losing value to inflation.

The idea of negative rates only seems less insane if the rate of deflation is higher than that of the absolute value of the negative interest rate (the bonds still generate positive real returns). But if you have negative yielding bonds in an accelerating inflationary environment (even if temporary remember most bull markets end with a spike of inflation followed by deflation) you should and probably will see a very large and possibly destabilizing sell off in European Sovereign bonds.

At the very least, the ECB and BOJ won’t have to get on their hands and knees and beg for someone to sell them some of these “safe” assets. In the end, volatility in the sovereign bond market will undoubtedly translate into volatility across all other asset classes. From equities to currencies to commodities. The end result being the very end of this central planning engineered low volatility environment.

Let’s not forget, in this scenario, the Fed is also behind the curve, just not as far as the ECB and the BOJ, but behind all the same. Hindsight is 20/20 and it’s clear the Fed missed the optimal window to raise rates back in 2013 or even in 2015. Fears of China and global fragility derailed any of the rate hikes necessary to keep the Fed ahead of the curve. And to be fair, the dollar is the world reserve currency and I believe if the Fed hiked in 2015 more than once we would have seen serious financial cracks split wide open.

Now given the recent data and the upcoming BREXIT vote, I don’t expect the Fed to hike in June. Which means the Fed in this bullish scenario will undoubtedly fall behind the curve. By September, it would be apparent that the Fed made mistakes and then the big question is what happens next.

At that point the Fed may be forced to guide the number of rate hikes per year much higher. From the 0.5 per year the market is currently predicting to as high as four. This would represent a significant and sudden tightening that the world like back in January was not prepared.

Thus I think risk assets could be seriously capped on the upside. But that doesn’t mean they couldn’t rise sharply if we did see a BREXIT vote failure coupled with dovish Fed and a more robust US economy in Q2 and Q3 of this year. Which once again makes S&P call options an interesting hedge for this brief period.

I probably should get into the pitfalls of an emerging market recovery based on the health of China’s economy, but this article is getting long in the tooth and that isn’t my area of expertise (not like any area really is). Instead I’ll end it with some good hedging strategies that are either 1) relatively cheap and 2) can fit into my bearish bias. Firstly, I would like to reiterate the great risk reward opportunity S&P call options provide over the near term. No one thinks we will hit new highs on S&P which makes call options above that level so cheap and a great way to hedge this bullish scenario. Secondly Credit default swaps (CDSs) on European peripheral nations or outright shorting European sovereign debt seems like the most obvious choice. As bond yields rise, the governments ability to pay back their debt will be called into question and risks of default should sky rocket. It also happens to play right into the hands of my bearish perspective on the EU its banking system.

That’s it for now. This article has been incredibly trying to say the least. I’m going to dunk my head in a bucket of ice.

Pingback: So You Think You Can Hike – The Klendathu Capitalist

Pingback: The Bull Case Revisited – The Klendathu Capitalist

Pingback: Top Posts From 2016 – The Klendathu Capitalist