“See, madness, as you know, is like gravity: all it takes is a little push.” ~ Heath Ledger’s Joker

Following up with yesterday’s post, the BOJ prayers for eagles were answered with doves. Once again the Fed decided to keep the rate hike on hold and left the BOJ hanging. The irrational nature of faith in central banks makes it incredibly difficult to predict when it will reach a tipping point. The only thing one can do is notice which way the needle moves.

https://twitter.com/edwardnh/status/778990365344993280

Yellen’s press conference had noticeably tougher questions this time around, fielding questions about Trump and central banking credibility. And of course, the BOJ with its “yield curve control” program is certainly not helping to alleviate those concerns of central bank incompetence.

Which begs the question…

https://twitter.com/TheEuchre/status/778766528728535040

The market has not yet fully considered/understood the actions necessary for the BOJ to implement its “yield curve control” policy. The BOJ was purposefully unclear on how exactly it would raise long term interest rates while monetizing the entire bond market. Even Goldman Sachs hasn’t a clue how this will be accomplished

Recall back in 1930’s when FDR first stole all the gold in the US, and then promptly raised the price once they had all the gold. For all intents and purposes, the BOJ is the JGB market, and unlike gold they control an imaginary faith based asset that is more easily manipulated. It’s a scary thing to admit but the BOJ can do whatever it wants as long as the market is OK with it.

However, this manipulation is not without its price. The JGB market has not functioned properly for years, and this recent move is the icing on the cake. The potential spill over effects to the repo markets and thereby the Japanese banking sector are enormous.

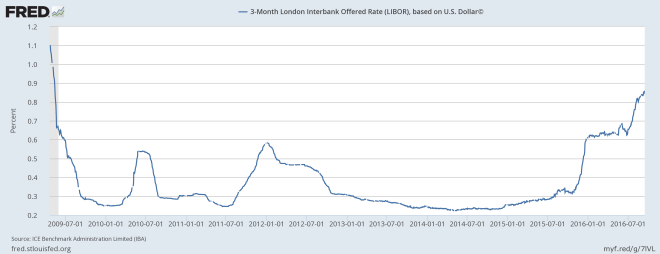

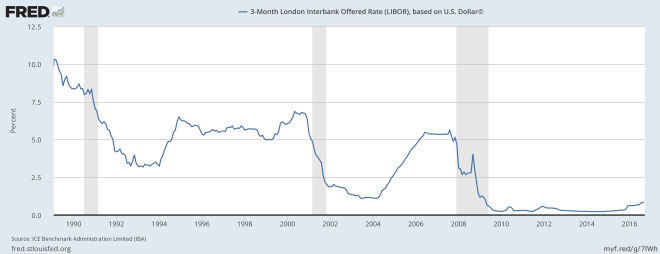

I’m not a financial plumbing guy, but the optics of this situation look abhorrent to say the least, I highly recommend you take a look a Jeffery Snider’s work on the subject. I’m not sure what’s more troubling, the fact that Libor is at its highest point since the crisis or that this steep rise has followed an unprecedented period of calm.

Perhaps more even more worrying is Deutsche Bank’s behavior. The following is an excerpt from an article titled “Is Deutsche Bank Cooking its Derivatives Book to Hide Huge Losses?” written by Mike Shedlock:

“I do not know if the problem is derivatives, the eurozone mess, negative interest rates, counter-party risk, or some combination of the above, but the above images collectively say something is seriously wrong, not only with Deutsche Bank, but the European banking system in general.”

The point is, central banks can shift or hide risk, but they can’t erase it entirely. These aren’t Hillary Clinton’s emails, and the market will hold them accountable one way or another. In the case of Japan, my eyes are on the Yen. With these dangerous new steps, the BOJ is increasingly pushing itself further out on a limb.

Remember, the BOJ chose not to accelerate the growth in its balance sheet which is the most effective tool for moving exchange rates. In the end, the BOJ’s many actions did very little to alleviate any upward pressure on the Yen. It will be interesting to see if the Yen continues to appreciate from here.

Depending on where the US economy is in its cycle, a further slowdown from here could push the dollar weaker and the Yen even higher. If US growth slows further weakening the dollar, the globe could find itself in a bit of a dollar funding squeeze as exports to the US fall.This dollar funding squeeze would most likely set the stage for a massive dollar rally.

Looking at the chart, the dollar could break either way, and given a foreign shock the dollar along with the Yen would likely go much higher, but where the dollar actually wants to go, where it’s headed, may actually be lower.

If you think about that magnificent 2014 run the dollar was on, a large part of the momentum may have been driven by a tightening Fed and an accelerating US economy. Recall market expectations were that the US economy would grow at over 3% a year and the Fed Funds rate would rise to 2%.

Instead we have sub 2% growth and the Fed funds rate is pinned to the floor. So it’s not surprising that given all the financial stress in the global economy that the dollar is not rising. The dollar over shot its target based on ridiculous expectations and now we may be witnessing a counter swing move that too goes further than it “logically” should.

If you recall, the false breakdown in DXY in May of this year was barely saved by a few hawkish speeches by FOMC members, you start to wonder if the threat of future rate hikes is the only thing keeping the dollar elevated at this point.

If the US economy continues to slow, the data may no longer support another Fed rate hike. The Fed would then be forced to capitulate and without threat of a further rate hike the dollar will finally bottom and mark a tremendous buying opportunity. Sounds fancy and maybe it just might happen.

Would you like to know more?