A lot of big shifts/events have transpired over the past week or so and I’d like to touch on them.

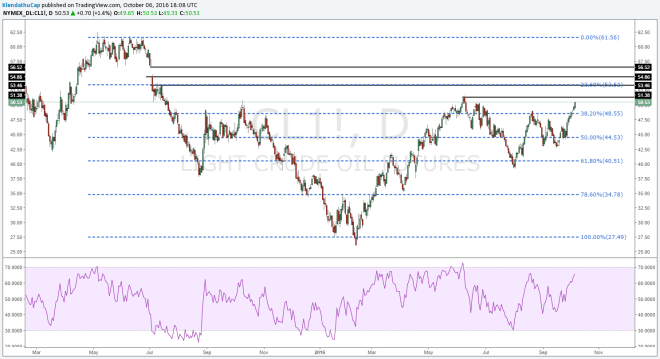

First is oil, and the potential November OPEC production cut. The market has bought the news and oil rallied quite strongly. From the looking at the chart, it’s not too hard to see an inverse H&S pattern forming. A break of 51.5 would suggest oil is going to at least last year’s highs of 61.6. But my bias is to be short oil, and long the dollar. I’m also very skeptical of OPEC’s ability to cut production for a meaningful amount of time. Saudi has the capacity to cut a little bit, but Iraq, Iran, Libya and Nigeria still have additional capacity that they’d like to bring online. I’m actually looking to short WTI. Anything above 51 is a good short in my mind but I might play it cautious and wait till it hits 52.

The problem with oil prices rising so rapidly is that interest rates which HAD fallen to record lows all across the globe have started to rebound. The relative effects from such a rise have profound implications across asset classes.

The statement is a two way street. If bond yields, then equities by comparison become less attractive. As such Utilities and REITs have taken the recent moves on the chin.

Meanwhile, the US economic data while not good hasn’t been terrible which led to the reemergence of Fed rate hike talks. What’s interesting is the case being made for rate hikes is one of financial stability rather than an over heating economy. A growing number of Fed members are worried about the implications for staying at zero for too long. Yet another red flag for risk assets. All of this noise has led to a potential break out in the the dollar index, DXY.

For those who didn’t read last Thursday’s post on the dollar, I’ve become quite bullish due to a number of factors on top of the myriad of problems facing various banking systems around the world.

The fact that rates and the dollar have been rising together with oil is a very interesting dynamic that is not likely to last, but it may have also successfully disguised the BOJ’s “yield curve control” policy. The recent rally in USDJPY has a lot of resistance to work through before we can call this a true break out.

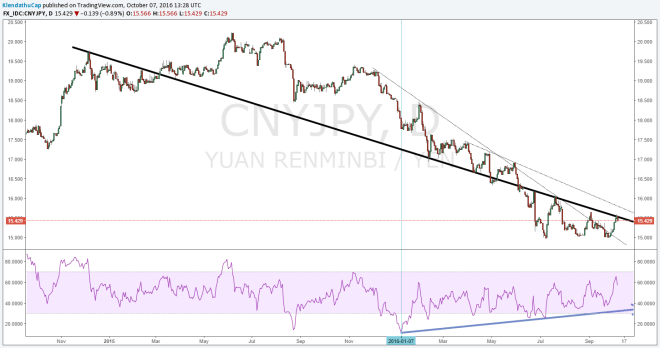

It’s important to note that none of this rally can be attributed to a sharp sell off in JGBs that forced the BOJ to print additional Yen. From a technical perspective, I’m looking for USDJPY to clear the 106 level and hold it. I remain skeptical that the BOJ’s policy has actually started to work. There exists a sizable speculative net long Yen futures position and these spikes may simply be a side effect of the “surprising” rate hike talks. Notice the Yen’s inability to clear a rather interesting trend line in CNYJPY going back over a year.

This could be nothing, but the economies of Japan and China are more closely linked than the markets seem to realize or care. Still important to note the positive momentum divergence in CNYJPY.

But let’s not forget gold, which has bared the brunt of these recent actions. As I said back in August, I thought the primary driver of the gold rally was lower interest rates. With rates on the rebound and a resurgent dollar, it is once again no surprise to what is causing such a steep drop in gold.

If oil continues to rise and drags bond yields with it, gold could fall even further. Also the negative momentum divergence with the price action is a little worrying. With that said, being a gold bull and an oil bear, I think the recent sell off has provided an ample opportunity for adding on to the position and I’d look forward to buying at even better price if the market offers me the chance. That’s not to say I don’t foresee an environment where rates rise against a falling oil price, but once again, that may largely depend on the effectiveness of the BOJ.

As you can see, for a global macro investor these days, there are a lot of unpredictable and irrational actors that play a significant part in the movements of markets. Not to mention the compounded effects from “the reach for yield” phenomenon. As rates rise, assets that were priced based on rates remaining low in perpetuity have to be repriced. In addition the market is working through some very important inflection points which have only added to this volatility. Going forward, it will be interesting to see how these narratives all play out.