The world increasingly finds itself off-balance. The reach for yield phenomenon has left the global system exposed to any increase in interest rates. Rates were steadily rising from the relative peak in “reach for yield” over the summer, but it wasn’t until Donald Trump won the election that investors had a narrative they could latch on to, “Trumpflation”.

Trump is expected to run large deficits that will stimulate inflation. Except Trump’s stimulus package which is only $1T over 10 years will be executed mostly through tax credits. Hardly inflationary, but investors have latched onto the narrative all the same ignoring the bigger risk for rising inflation, China. According to @CrossBorderCap, the world’s factory, China, is the true driver of inflation.

Recall during a 4 week period in Q1 of this year, China pumped out $1T in stimulus. And that stimulus along with the very slow cutting of excess capacity has broken the deflationary spell that had gripped China for the past 4 years.

Investors have been caught off-side by higher inflation leading to record losses in the sovereign bond markets.

The amount of debt in the global financial system has never been higher which will magnify the impact of any move higher in interest rates. To make matters worse, US yields have led the charge higher which has lifted the dollar with it.

Although the trade weighted dollar index has yet to break out to 13 years highs like its DXY counter part, a rising dollar spells trouble for those who borrowed cheap Fed QE dollars post crisis. According to Paul Mylchreest of ADM,

“Chinese companies and entities probably hold $2 trillion of “short dollar” positions once contracts through Hong Kong, Singapore and Japan are included.”

With the Yuan at a post crisis low against the dollar, I’m very worried that this unwind could accelerate beyond the control of central planners.

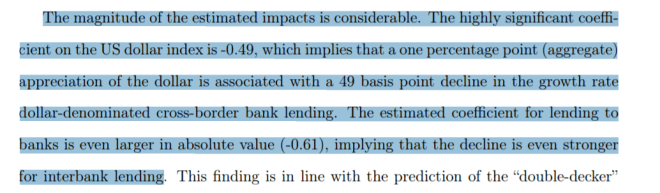

The BIS paper had some very interesting conclusions. Perhaps most significant is the rising dollar’s effect on interbank liquidity.

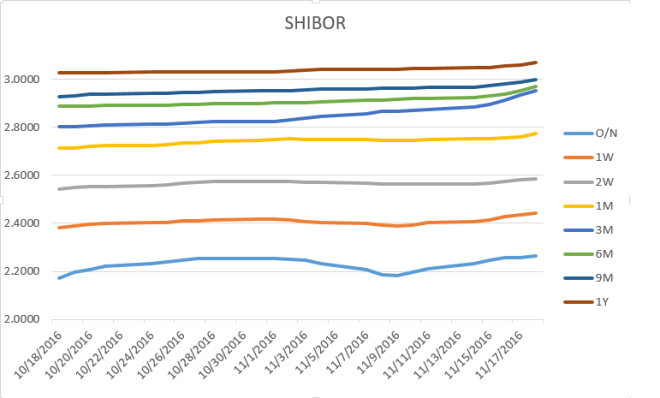

Unsurprisingly interbank lending rates rose every day this week with the longer durations starting to make substantial moves higher.

And yet despite this relatively large tightening, the Yuan continued to weaken against the dollar. The steep depreciation will most likely be met with increased capital flight further straining liquidity in the Chinese economy.

China's yuan depreciating at close to 25% month on month annualized pace https://t.co/2Zk6oKIntM—

Tom Orlik (@TomOrlik) November 18, 2016

However, it is important to note that the Yuan still managed to hold its own against the rest of the major currencies, proving that this is a dollar strength story more so than a Yuan weakening story… for now.

But the dollar is the most important fiat currency in the world, for its rise poses problems for all countries who borrowed too many dollars, not just China.

Going back to the BIS paper,

” Our results therefore show that the dollar index has explanatory power over and above the bilateral dollar exchange rate for cross-border bank lending. This finding strongly supports our previous hypothesis that the dollar is a global risk factor, which affects the risk-taking capacity of banks, and, ultimately, the supply of cross-border bank lending.“

In short, the rising dollar is a sign of rising systemic risk. To make matters worse, there are participants who are actively throwing fuel onto this rising fire.

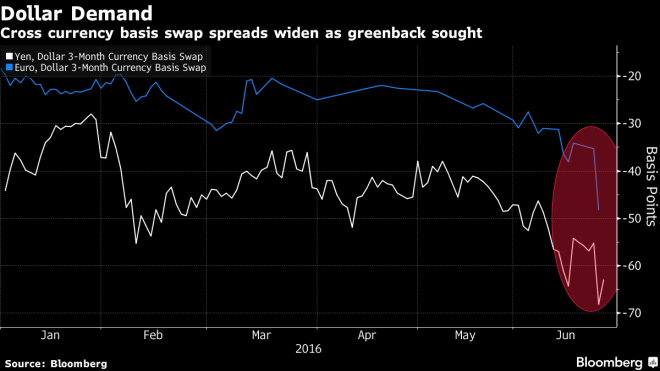

Ignoring the fact that every peg in financial history has been broken the BOJ plunged headfirst into the breach and pegged Japanese Government Bond yields to the floor. Their goal is obvious, force investors out of zero yielding JGBs and into other higher yielding assets such as the dollar. By artificially inflating demand for the dollar this policy creates a serious dollar shortage in Japan which is evident in the deeply negative basis swaps.

I bring this up, because the Yen normally appreciates in risk-off environments. Japanese investors hold the largest amount of assets as percentage of GDP abroad. When markets sell off, Japanese investors repatriate their capital which strengthens the Yen. And yet by strengthening the Dollar vis a vis its yield curve control policy, the BOJ is increasing the likelihood of igniting a risk-off environment that would undo all its Yen weakening efforts.

Bringing this all back to the US economy, where the stronger dollar will most certainly act as a headwind for growth and earnings. In my last post I wrote,

“Let’s not forget the US consumer who is by no means healthy with debt levels hovering at record highs. The double hit from higher mortgage rates and Obamacare premiums is likely to be too much for them too handle.”

Their rising wages will eat away at any corporate earnings growth while simultaneously being insufficient to cover the rising costs of housing and healthcare. All in all, this is not a healthy economy whose recession will likely provide a dollar head fake that could rapidly appreciate the Yen beyond the BOJ’s control and wreak havoc in the financial markets. Needless to say, the Klendathu Capitalist is as bearish as he’s ever been.

Pingback: We Need To Talk About China – The Klendathu Capitalist