And if you said this life ain’t good enough

I would give my world to lift you up

I could change my life to better suit your mood

Because you’re so smooth

~ Smooth by Santana

Despite the 6.7% growth, 2016 has not been a good year for China. I’ll be the first to admit that I do not fully understand why Xi is waiting for the government reshuffle next fall. In spite of the smoothest GDP growth in economic history, I find it hard to believe that higher debt levels, smaller FX reserves, and rising shadow bank risk will be any more manageable under a regime where he has “full” control.

Fortune favors the bold, and although Xi has boldly secured power for himself, he does not deem it sufficient to combat the problems he faces. And maybe he is right, maybe he lacks the required strength to do what is necessary, but that inaction speaks volumes about the efficacy of the Chinese government. Maybe Xi is like Alexander Hamilton who I alluded to in a previous post:

“Alexander Hamilton had already mapped out the future republic of the United States at the close of the revolutionary war in 1783, but it wasn’t until 1787 that the US Constitution was actually created and it would take another 2 years after that for it to finally be ratified.

Donald Trump much like Alexander Hamilton has promised drastic change in a time of hidden crisis. To these men it was clear that the final battle had not yet been fought, but the majority of the population did not share their sentiment.

… Donald Trump is akin to a battle commander who has charged too far ahead of his troops. He will need to wait to gather the army before he can launch an effective attack. I have little doubt that Donald will bring about much needed change in time, but rescinding some executive orders will only tickle the status quo.”

Is Xi too far ahead of his time? Perhaps he is. Clearly there are sizable vested interests blocking his path. I don’t think it is a lack of knowledge of the problems, but the way in which to combat them without upsetting the status quo. But the status quo is part of the problem, and is what Xi seeks to change. Xi likely feels the best way to change the status quo is to change the people in power through bureaucratic means next fall.

Of course, there is another, less kind analogy one could use, and the truth is probably somewhere in between, but I think General George McClellan of the American Civil War, might prove to be a more apt analogy. Like General McClellan during the American Civil War, Xi is waiting for full strength before launching an assault. With the hindsight of history, we know that McClellan bungled multiple opportunities to end the war in its first year if he had acted more decisively.

Obviously Xi will not be able to solve China’s problems nearly so quickly. China’s credit boom and its solutions will echo through the decades, but unlike McClellan’s predicament, where the South’s capacity to form and equip an army was much more limited, debt and risk in China are growing exponentially. By the time Xi’s armies arrive, the enemy is likely to be the largest and most powerful force in economic history. Defeating such an enemy will be nigh impossible, One must not miss the irony of this analogy, for should Xi fail, he risks starting the very thing McClellan failed to end – civil war.

As poetic as that all sounds, I have a lot to learn about Chinese politics and perhaps should dedicate my time this winter to such books (I am happily taking any recommendations). So it’s best to take my analogies with a grain of salt and enjoy them for what they are, an introduction into the quagmire that is China’s economy.

For now I feel forced to assume that the Chinese government will do everything in its power to maintain a “stable” Chinese economy till at least the fall. Their recent policy moves have indicated as much. 2016’s global shopping spree of Chinese billionaires and companies has led the government to institute a freeze on future deals lasting right up until the fall reshuffling. From the WSJ:

“The new controls, once in place, are to remain in effect until the end of September and thus are intended as a temporary tool to stabilize outflows ahead of a major reshuffle of the top echelon of the ruling Communist Party late next year, the people familiar with the matter said. That’s in keeping with other efforts by Beijing to try to keep the economy on an even keel before the leadership change.”

Consensus believes Beijing will keep the economy stable up until the leadership change. Although I do agree that outcome has the highest of available probabilities, I think that those odds are falling. Trump has thrown the “One China” policy on the bargaining table, as well as the Yuan and pretty much everything else. He may be relatively soft on Russia, but he’s going hard on China. Or to steal from Quentin Tarantino,

“You devalue the Yuan in your dreams, you better wake up and apologize.”

An obvious problem with this strategy is that China is fragile. The Chinese economy relies on increasing amounts of foreign capital to keep its economy going. When that does not come in, the central authorities must provide. In essence, China cannot give Trump what it does not have. But perhaps, the reason why Trump is hammering them from the get go is because of these apparent weaknesses in both the economy and Beijing’s power structure.

After the reshuffling in the fall, Xi will be far less likely to acquiesce to any of Donald’s demands. For once Xi has his power, it is assumed that he will begin instituting much needed change. Those changes very likely will be detrimental to the short stability of China, and indirectly the United States.

Once again, Trump may be smarter than people think, by pressing China now, he reserves “the right” to blame them for US economic woes during his term if and when Xi decides to stop sacrificing China’s long term stability. Until then, China needs to stop capital outflows, maintain its economy for the next 9 months, and keep Donald Trump at bay. Welcome to the new golden triangle.

Maintaining the Yuan has proven exceptionally difficult of late. China continues to add new laws and regulations that have increasingly hampered the economy and done little to staunch capital outflows that have once again started to rise.

“Several European companies in China have been unable to remit dividends abroad following the introduction of new exchange controls, the first indication that Chinese attempts to curb capital outflows are causing problems for foreign businesses. The EU Chamber of Commerce in Beijing said the payment difficulties experienced by European companies were “disruptive to business operations”. “

The Chinese government now risks hurting foreign investment into the country if corporations cannot bring their profits home. This is coming at an especially trying time for the nation as private investment has been on a downward trajectory for the past 5 years. Despite the massive stimulus from the central authorities, the private sector has not been convinced in a recovery whatsoever.

The image above, as The Long View states, is quite powerful. The Chinese government to use yet another historical reference, has engineered a counter offensive akin to the Battle of the Bulge in WWII. Right up until the battle it was perfectly clear that Nazi Germany was going to lose the war. Nazi Germany was quickly crumbling under the multiple fronts, dwindling resources, and Hitler’s repeated mistakes. And because of all of these “facts”, the Allies under estimated the Nazi Germany’s strength and paid dearly for it.

Nazi Germany threw everything it had into that battle and once it was over, the regime quickly crumbled less than four months later. Economic cycles last much longer than war cycles, so I’m not saying China is less than 4 months from collapse, but that once the stimulus fades, the economy will roll over hard and fast.

I will admit that I drastically underestimated the Chinese government’s resolve. And when their backs were against the wall, they released an economic blitzkrieg likes of which we have never seen. Unlike the two month Battle of The Bulge which oddly enough started in mid December, the results of this blitzkrieg are still playing out almost a year later. The most obvious of which is rising inflation. I made note of this inflation in previous posts “Weekly Review: Would You Like To Know More” and “It’s A Trap!“.

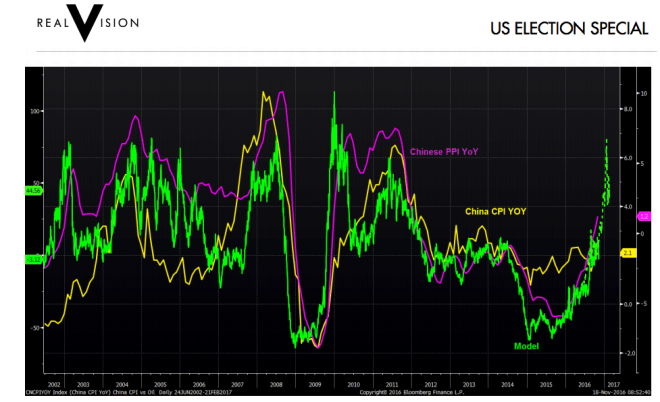

“2016 was a lost year for the Chinese economy and yet the leaders in Beijing continue to believe that they control their own destiny. But as they continue to close down other channels of capital outflows, it risks trapping this inflation in China and further destabilizing the country. As Julian Brigden’s model shows, China in less than a year has gone from deep deflation to surging inflation.”

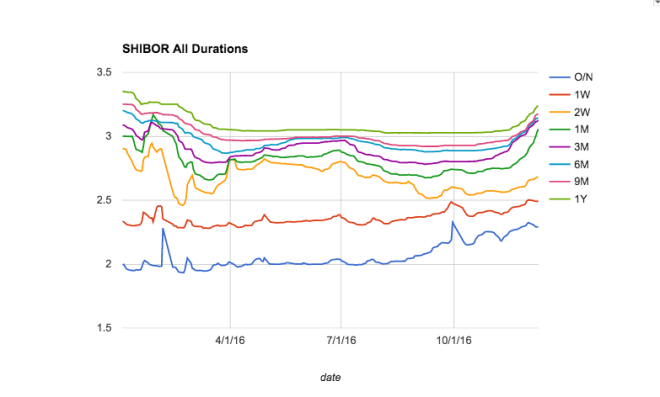

In response to this dramatic shift from deep deflation to ripping inflation, the Chinese government has been forced to tighten liquidity.

The long end of SHIBOR has exploded higher, and will likely go much higher before this is over. After all who would lend for a year at less than 3% if inflation is pushing 5%?

If the Battle of the Bulge analogy holds, the Chinese economy will roll over much harder and faster than consensus and even the central authorities anticipate. The market could shift from a risk-on inflationary environment to a risk-off – inflationary environment quite quickly.

In this scenario, to use yet another WWII analogy, the Yuan would be fighting a war on two fronts. Rising inflation coupled with rising demand for safety would only add more fuel to the dollar shortage inside China. This short period of strength the Yuan has enjoyed from tighter monetary policy is likely over. With the 7 handle in sight of USDCNY, FX reserves should deplete much more quickly and once again reenter back into the consensus narrative. With that said, I’d like to thank Bloomberg News for their wonderfully timed article.

And once again, as the Chinese economy is set to slowdown, the Fed is about to hike interest rates. It seems a bit myopic to suggest that the world is about to witness a 2016 January sell off redux, but the similarities are too hard to ignore.

With just 9 months to go, Xi can practically see the finish line. At this point it is a forgone conclusion that the central authorities will go above and beyond to do what is necessary to get the economy there. What I am worried about, is that rising inflation will make it quite difficult if not close to impossible for the stimulus to have the desired effect.

Too much stimulus and they risk fueling the inflation further which would raise interest rates and actually tighten liquidity. Too little stimulus, and the economy looses momentum and descends into the deflationary spiral their economic Battle of the Bulge was meant to delay. We’ve already seen the Australian economy start to hit the skids. There are many financial bubbles riding on China maintaining their economic stability.

Although I have my doubts, there still remains the possibility that China will able to successfully walk this line. If that is the case, the rest the world should expect much higher inflation going forward.

I’m going to save the consequences of higher inflation for another post entirely. If you’d like to know more, follow me here or on twitter. For now, China is in a big heap of trouble. They are proven masters at the game of can kicking and perhaps should not be bet against, but at the same time, even if they are successful they will likely push inflation into the parts of the world that are most unprepared for it. I for one look forward to watching Trump try and dance on the tight rope with them.

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.

Pingback: Another Head Fake: Why The Euro May Go Higher – The Klendathu Capitalist

Pingback: Inflation Takes a Breather – The Klendathu Capitalist

Pingback: Predictions For 2017: Shit Escalates – The Klendathu Capitalist

Pingback: Keeping Up With The 2017 Predictions – The Klendathu Capitalist