TRIGGER WARNING: This post will include political analysis with very trace amounts of opinion thrown in. As investors so often like to say and rarely actually do, “I am just observing”.

“Now this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.” ~ Winston Churchill

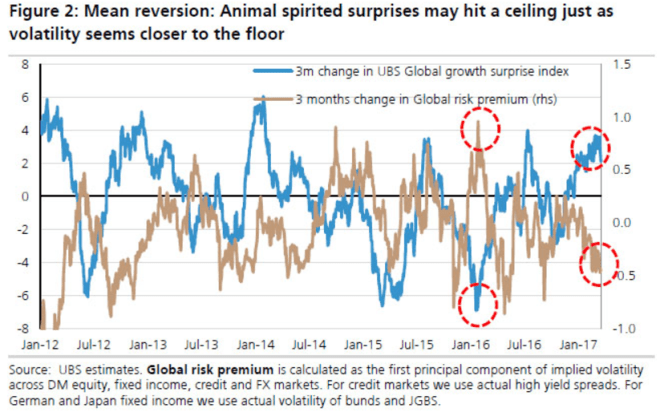

The first correction in the final leg (according to me) of the post crisis bull market has begun. Given the tremendous tremendous divergence between market expectations and reality there is likely a bit more downside to come. Positioning, and sentiment are polar opposite to the bottom we saw in Q1 2016.

Especially, if you consider at what the market was pricing in: record business and consumer optimism as well as a smooth and efficient US government that would pass healthcare and tax reform in short order.

Instead we have a bellicose interventionist President Trump who has sparked geopolitical tensions in the Middle East and North Korea. At the same time, the French elections are turning out to be less clear than the market also predicted (notice a pattern).

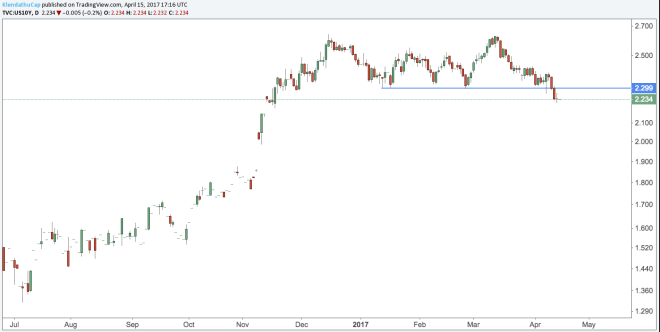

In the end, shit is about to get somewhat more real, but that doesn’t mean the highs are in (more on this later). For now the Trump/reflation trades, which have looked weak these past few months are beginning to unwind. The key 2.30% technical level on the US 10 year was finally breached this week.

The technical breakdown in the US 10 year treasury likely signals further downside in US financials (XLF), a key beneficiary of the Trumpflation narrative.

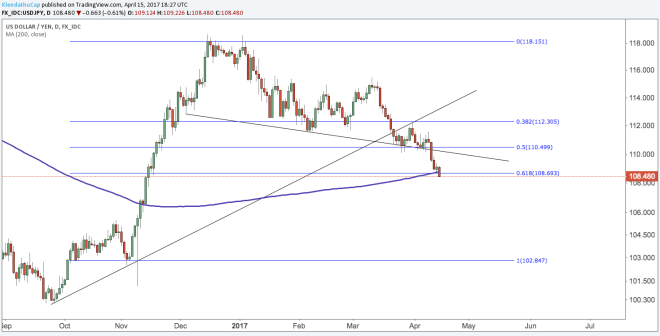

The Yen a key measure of risk has been strengthening, blowing through stops, and just generally crushing risk appetite. Now below the 200dma and the 0.618 fib re-tracement level off the pre-election lows.

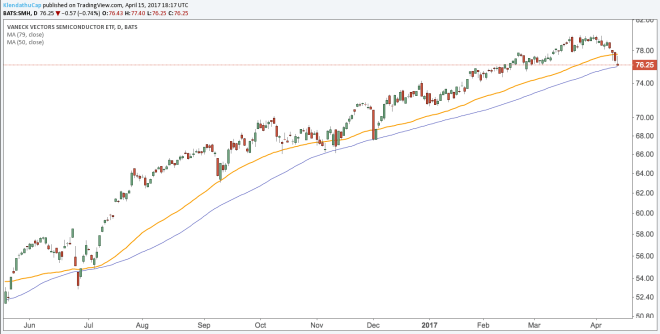

Semiconductors, the post Brexit leader, up 50% from the lows, has closed below its 50dma and is testing the super special (sarcasm) 79dma. But seriously. We haven’t seen a close below the 79dma since BREXIT. This will be something to watch going forward.

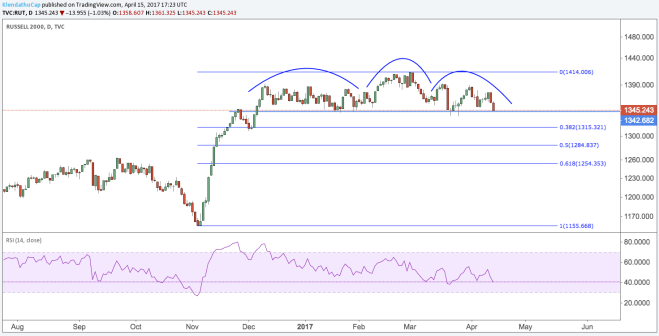

There’s a clear H&S pattern on the Russell 2000.

At the same time, XLE has led oil this year and looks to be headed lower. Given the importance US shale plays in the economy, this could signal further economic weakness.

Throwing salt on the open wound, retail sales and inflation both disappointed expectations on Friday.

https://twitter.com/epomboy/status/852861849108455425

In short: “It’s an ugly planet, a bug planet!” (Video might be broken, but hey! At least you get the reference now).

Although the risks, given the lofty valuations, are asymmetric to the downside, it is of vital importance to not get carried away with our bearishness. I made this mistake in 2016. I missed the signs of a bottom. I had been short on the way down, but instead of pulling back, I pushed harder and paid for it. Maybe this is the time to do that, but maybe it’s not (more on this later). It is worth noting that folks are still incredibly scared of a one off event (including myself).

https://twitter.com/InterestRateArb/status/853297257520799745

As investors we are in constant conflict with our inner animal which tells us us to sell when we should buy, and buy when we should sell. Not only must we not give in to these primal instinct, we must also be keenly aware of the fact that if we are experiencing these emotions it is quite likely that others are as well.

If this correction continues it does NOT mean equities are about to fall apart. Market tops are long processes that take months if not years rarely ever days. Sure the parallels to a 1987 style event have been shown time and time again. Vol selling is the new portfolio insurance. Passive is only passive on the way up. CTAs have record assets under management. The fuel is certainly there. I get it. I am aware of it, but so is everyone else. Stocks have barely fallen and yet the cost of hedging has already shot up dramatically.

Investors remain keenly aware of any downside risk. Meanwhile the central bank put is still there. The Fed may be hiking now, but with economic data coming out towards the downside, Trump meeting stiff resistance in Congress, and most importantly a falling stock market the Fed can quickly pivot from hawkish to dovish rhetoric. If the sell off does accelerate, I expect talks of balance sheet reduction to give way to QE4.

Perhaps this shift potential shift from hawkish to dovish may already be showing in precious metals.

Although I’d likely attribute most of the move in gold to the war premium.

Worth noting, as Luke Gromen likes to remind people smart enough to follow him on twitter: high stock prices are now a matter of national security. Even with equity markets at at all time highs, pensions remain tremendously underfunded. A fall in financial assets would cripple pension funds. The knock on effects would spiral out beyond the government’s control leading to consumer debt crisis with the Fed forced to monetize an ever widening US Federal Government deficit.

Thus the Fed, and “the powers at be” have a hefty amount of incentive to keep stock prices elevated. At the very least, the Fed, armed with its newly minted ammo, should be able to hold the line for 3-6 months before it has to even think of threatening the nuclear option, QE4. Look for the Fed to buy time while the market narrative adjusts to the reality.

From the WSJ:

“A growing number of forecasters are beginning to reconsider their bullish outlook for the U.S. economy as doubts grow over the extent to which President Donald Trump will be able to implement his agenda.”

Now that price and economic soft data are beginning to reflect the “hard: reality, I find it quite comforting to see economists like rats jump from the sinking ship that is Trumpflation and the hopes of fiscal stimulus that come with it. Ironically, as the mainstream lose faith in any Trump stimulus or healthcare reform, the odds of the passage of said legislation are actually rising, albeit from a very low base.

WARNING: Here be Dragons. You are entering the political analysis section of the blog post.

What the narrative surrounding Donald Trump refused to acknowledge was just how little power US presidents have domestically. This is especially true when Congress is gridlocked to a standstill. Throw in debt and demographics on top of the rigid congress, and the US president’s domestic policy is practically set in stone.

After failing domestically, Trump has turned his focus abroad. He needs to score some quick wins politically and I’d say he’s done just that. He has used missile strikes in the Middle East to threaten North Korea and force Chinese action (at least superficially).

By projecting US military strength abroad, Trump has pulled the war hawk members of Congress on both sides of the aisle closer to his point of view. At the same time, he has allowed more of his policy decisions to be influenced by Jared Kushner a left leaning New Yorker further bridging the wide divide between his administration and the Democrats.

At the same time, as the economic backdrop continues to deteriorate, Trump will be more than happy to lay the blame at the feet of a gridlocked Congress. I can see it now: “Congress can’t pass much needed health care reform while bad Obamacare implodes. Sad!”

The Democrats have the most seats in contention next year, and will need political wins to secure those seats, else they’ll cede total power to the Republicans and Trump. They can’t do that if they sit by idly as the economy implodes. With some of the Dems coming closer to Trump’s camp, it won’t be hard to leverage the necessary votes for health care reform which would then pave the way for tax reform. Throw in talks of QE4 and the stock market could surge for the final leg of the post crisis bull market.

DISCLAIMER: This blog is the diary of a twenty something hedge fund manager who has never stepped foot inside a wall street bank. He has not taken an economic or business course since high school (for which he is immensely proud of) and has been long gold since 2012 (which he is not so proud of). In short his opinions and experiences make him uniquely unqualified to give advice. This blog post is NOT advice to buy or sell securities. He may have positions in the aforementioned trades/securities. He may change his opinion the instant the post is published. In short, what follows is pure fiction based loosely in the reality of the ever shifting narrative of the markets. These posts are meant for enjoyment and self reflection and nothing else. So ENJOY and REFLECT!