As a pessimistic China observer (naive western perma bear), I’ve wanted to short emerging markets for sometime. For my sake I’ve been very patient on this trade and haven’t fancied a go on the dark side, unless you count my 2nd failed attempt to short the Superhuman Canadian Banks. Luckily there was an ongoing implosion in US retail industry that has kept me busy. But even that trade appears less appetizing these days. So here I am, a bear without anything to short, which is partly why I’ve turned my attention to the rip roaring Emerging Markets, but I swear I have other good reasons.

Whatever happened to Brendan Fraser? I guess the same question could be asked about the dollar bulls.

https://twitter.com/HerrWilmore/status/909011286146600960

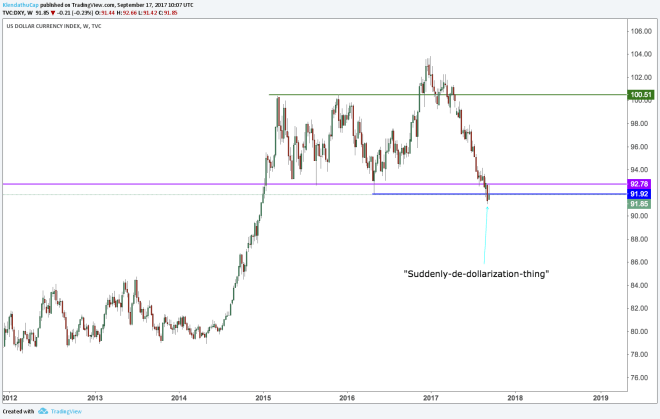

Anyway you slice it, USD positioning is not only incredibly bearish, but just 9 months ago incredibly bullish. The shift in investor positioning is enough to give a person mental whiplash. Why the sudden shift you ask?

Such a shift in sentiment is not without a narrative to support it.

I’m not mocking the proponents of this theory, although it certainly seems like I am, I swear (see previous Mummy reference) that I’m not. I just happen to sincerely doubt the speculators who switched from net long to net short are capable of such deep thought and will only come to their sense after they realize they’ve overreached.

As the infinitely evil DarthMacro likes to argue the USD will lose reserve currency status eventually but until then there are likely to be a few tradable scenarios in which we don’t have to sell the dollar into oblivion. Now MIGHT just be one of them…

Because last time I checked, the USD is still THE world’s reserve currency. As much as certain countries want to shift to a new regime, the high levels of debt and fragilities built into the current system make that virtually impossible. A clear example is the EU and the Euro. Although recently, some rather smart people have started to suggest that in fact the EU can handle a stronger Euro.

The note was from September 5th, but little did I know, 2 days before I made this tweet that in fact the French had begun to protest the much needed labor reform, although not in “great” numbers. There’s a star wars reference in here somewhere…

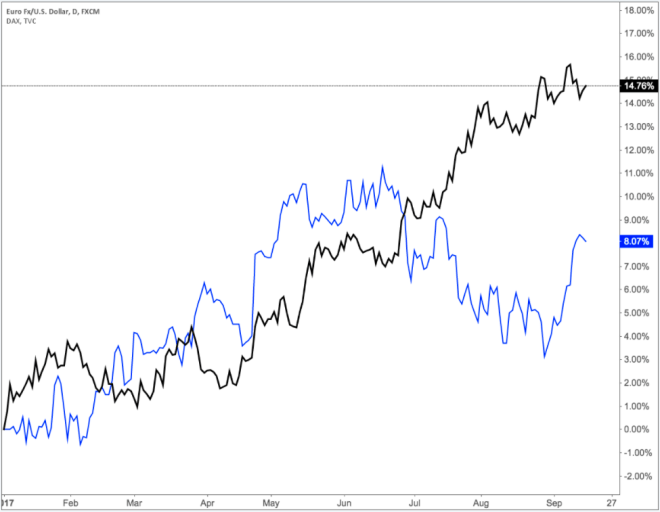

And yet, despite the mild protests, if your are an exporting economy and your currency strengthens 15% against a major trading partner, it’s going to hit you no matter what. Just look at the German DAX (blue) versus the Euro (black).

By the way, before I go any further, is there a more bullish sign out there than a heavy exporting economy’s stock market moving up in lockstep with a stronger currency? I’m sure some really smart macro guys picked up on this, unfortunately I was not one of them. But I digress because right now the DAX is having trouble rallying into this “excessive” Euro strength.

It’s bad enough for Germany, but what about countries like Greece, Spain, and Italy who were already suffering under a currency too strong for their own good. Fellow European exporter, Sweden has seen its economy take a turn for the worse.

Why is this significant?

https://twitter.com/m4crotrader/status/906498818404962304

After doing a little digging (aka a simple google search), I found Sweden’s top ten export markets to be as follows: Germany (10.3%), Norway (10.1%), US (7%), Denmark (6.9%), Finland (6.7%), UK (5.9%), Netherlands (5.3%), Belgium (4.5%),France (4.3%), China (3.8%) and Poland (3.2%).

Sweden mostly exports to Northern European countries. Meanwhile a large part of the resurgent EU story is actually a southern rebound story. Countries like Italy and Spain even Greece have started to show signs of life. Of course the Euro was already too strong for these countries. One can only imagine what the 15% rise YTD has done to their future growth prospects.

It is important to remember that the level of a currency is not as important as the magnitude and direction of change. The last time the dollar was at this level in 2014, emerging markets were undergoing a massive correction, commodity markets were in complete disarray and china was seemingly on the verge of a complete implosion. Once again I reiterate this does mean I think the EU is about to implode under a stronger Euro, just that the monetary union’s economies are about to take a breather…

Speaking of China, the rising power seems to be making trade deals every day to wean itself off its dependence of the US and the USD.

Have any of the dollar bears asked why China needs to do these trade deals in the first place? Oh yeah, because the US is a key trade partner and the USD is an ESSENTIAL cog in global trade as it stands right now. Removing the USD from the global economy would be tantamount to bleeding the global economy dry. Global trade would grind to halt, and everyone would be worse off. No one wants that. But I digress…

Because China’s economy has been running hot on the back of a poop ton (technical term) of stimulus and the weaker dollar.

What is often missed in this post Jan 2016 correction world is that China has gone from an exporter of deflation to an exporter of INFLATION, and given the fall in the USDCNY this should show up in the US in a big way towards the end of the year catching a lot of people off guard.

Can rates in Europe and Japan going to follow the US higher? With the NIRP and QE programs still in place I’m not so sure. Draghi certainly has the potential to tighten, so I won’t count the euro out. But the yield curve controlled Yen in this scenario?

At the very least, it seems like we are setting up for a bit of 2016 Q4 redux, where rates in the US rise higher than they do in the EU and Japan and the dollar strengthens. Given investor positioning, rising rates and a stronger dollar could set up for quite the pain trade. Not only are investors very bearish the USD, they are also very long UST duration.

Retail investors going hard in the paint for that $TLT.

Should probably ask some of my millennial friends what they think of dividend stocks.

And just so we are clear on the size of the potential tinder available to such a pain trade…

If you’re an EM investor it might even get worse, because China’s economy due to base effects and waning stimulus is set to slow into the end of the year.

Did Klendathu find his desired short trades? Perhaps. It seems that higher US rates are in the cards, and given USD positioning, we could see a rebound in the USD, but I wonder if we have in fact seen the highs for the USD this cycle.

DISCLAIMER: This blog is the diary of a twenty something millennial who has never stepped foot inside a wall street bank. He has not taken an economic or business course since high school (which he is immensely proud of) and has been long gold since 2012 (which he is not so proud of). In short his opinions and experiences make him uniquely unqualified to give advice. This blog post is NOT advice to buy or sell securities. He may have positions in the aforementioned trades/securities. He may change his opinion the instant the post is published. In short, this blog post is pure fiction based loosely in the reality of the ever shifting narrative of the markets. These posts are meant for enjoyment and self reflection and nothing else. So ENJOY and REFLECT!

What kind of dumbass shorts Canadian banks? Stick to what you know, kid.

LikeLike

Pingback: Big Week For The Once Mighty Dollar – The Klendathu Capitalist