I’ve struggled to write this article for over a month now. Thinking about the most clever way to talk up the bull case for oil. With the potential breakdown in the USD I thought about just saying dollar bear market = commodity bull market. But let’s face it, that’s far too obvious and I’ve already done that…

” I believe on a cyclical basis that commodities have bottomed or are in the process of bottoming. Maybe oil retests the 2016 lows, but overtime it should head higher, US shale be damned.”

Then I thought about incorporating the oil bull case with the fiat bear case. Because when every central banker is behaving like the Mad King Aerys Targaryen, shorting fiat in terms of real assets is a no brainer (maybe some other time though).

Instead, I thought it important to focus on something Opa used to tell me:

“Buy low.”

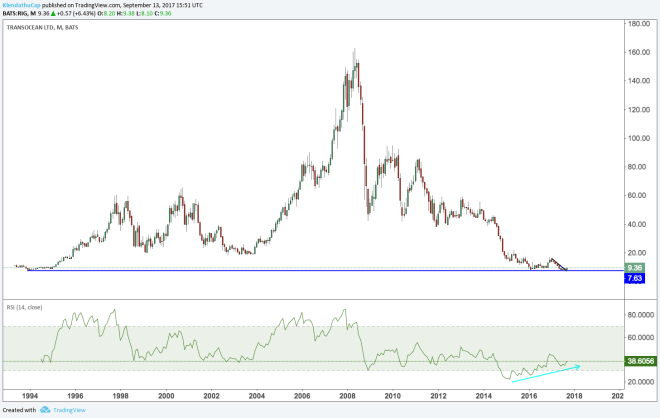

RIG, a company we own through the ETF OIH, is down over 95% from its ATHs and was recently trading at the lowest point in its 23 years. To put that in perspective, RIG fell 50% FOUR times. The multi year trend of rising RSI momentum and repeated failure to mark a new low is reminiscent of the pattern in the Euro we saw at the in December of last year. To be clear this trade is not without risks.

But as contrarians we welcome such news. If we look at the broader OIH ETF which includes as basket of these names. We’ll see a similar pattern bottoming pattern to RIG’s.

Think about what this chart is telling you. Think about the statement the market is making in regards to the oil industry. Offshore oil drilling is dead.

Think about what this chart is telling you. Think about the statement the market is making in regards to the oil industry. Offshore oil drilling is dead.

If US shale is really a technological revolution, why have the producers underperformed the commodity since the bottom in 2016?

And yet we are led to believe that oil prices will be contained in a 40-60 range. As Jawad Mian recently noted, complacency towards this mythical range is reminiscent of the view from 2011-2014 that oil would remain above $100 in perpetuity. And with the largest cut in capex since 1998, this seems unlikely to say the least.

Meanwhile, it’s been up to US shale to make up the difference in capex. I’ve recently read a couple of skeptical reports on the technological revolution that is the US shale industry. One of which comes from my friend @IndiePandant who makes a strong case that the shale revolution is not all it’s cracked up to be.

Then there’s a man who is as smart as he is skeptical, Russell Clark, who brings up a number of key questions in a recent piece such as the rapid decline rates of US shale, the heavy concentration in the Permian and Eagle Ford plays, and the incredibly poor returns on capital. And then of course there’s the plateauing US rig counts.

If the rig count is plateauing, why are predictions for US oil production growth continuing to rise?

And if the bearish oil case was only a bullish US shale case, that might be enough, but it gets better much better…

In case you haven’t learned to zig when The Economist zags yet…

The “Electric Vehicle crushing oil demand” story is completely overblown. Mass adoption, or even marginally higher rates of adoption continue to be pushed further and further out into the future. Meanwhile oil demand is booming baby.

It is likely that the weaker dollar combined with China’s fiscal stimulus have reawakened global oil demand. Although Emerging markets are not booming like they used to, they are still growing, and require more and more energy to fuel their growing economies. So not only is it likely that have we overestimated future oil supply, it’s likely we have underestimated future oil demand as well.

At a time when the all knowing oil gods cannot survive,

perhaps it is time for contrarian millennials who know nothing to thrive.

DISCLAIMER: This blog is the diary of a twenty something millennial who has never stepped foot inside a wall street bank. He has not taken an economic or business course since high school (which he is immensely proud of) and has been long gold since 2012 (which he is not so proud of). In short his opinions and experiences make him uniquely unqualified to give advice. This blog post is NOT advice to buy or sell securities. He may have positions in the aforementioned trades/securities. He may change his opinion the instant the post is published. In short, this blog post is pure fiction based loosely in the reality of the ever shifting narrative of the markets. These posts are meant for enjoyment and self reflection and nothing else. So ENJOY and REFLECT!