Head fakes, it’s a theme I’ve been trumpeting a lot of late. The rising inflation story I have said multiple times is a major component of this theme. Already fund managers have shifted to this rising inflation story, and the multi-year high in US 10 year reflects this thinking.

And perhaps the move in US yields has gone too far, but I’ll get to that later. Overall, I think the rising inflation story is not yet over. I may be a long term bond bull, but for now, I think higher inflation coming out of both China, and OPEC will lead to higher interest rates in the developed world, particularly in Europe.

OPEC has successfully pushed the price of oil much higher than it was a year ago. There of course has been much talk about how ridiculous the optics of their agreement looks but I think it is important to ignore the snarky Zerohedge headlines and focus on the actual price of oil. On a YoY basis we can clearly see that oil is pushing +50%. Bond bulls ignore this at their own peril.

OPEC production hit a record high this November, which certainly doesn’t bode well for a successful cut. At the same time, it looks to those on the surface, that OPEC is ceding defeat in its war with North American shale. And they are but that doesn’t mean they don’t have a plan. Russia recently sold a stake in Rosneft to Glencore (a Neutral Swiss Company) and Qatar’s SWF (OPEC). The deal was also financed through Russian banks to further integrate the two sides, OPEC and Russia.

With this bit of news, the OPEC production cut, in my estimation, has gone from an act of desperation to a smart gamble. OPEC+Russia now produces half the world’s oil, making it a much more formidable cartel. A cut of 10% of their production would amount to over 4 million bpd, the likes of which North American shale could simply not keep pace with.

But I’m not suggesting they do that all at once. This new cartel will likely take the Federal reserve’s approach of slow and steady moves. IF this first relatively small cut holds and by that I mean the price of oil stabilizes somewhere over $50, I could easily envision a scenario when as early as this spring we see significant chatter of a future cut that could come this summer. In essence, the cartel would force the market to price in additional production cuts before they even happen. OPEC+Russia production future production quotas could become the new Fed dot plots.

It must be said, that this is still a gamble. And like all gambles, this one is not without its downside. OPEC + Russia have acknowledged the power of North American shale, and will have ceded significant market share to them. IF there is another downturn in the price of oil due to a demand shock in the form of a global recession or something to that effect, this new cartel will find a much more resilient North American Shale industry than the one we saw in 2015 and 2016 which is saying something. In such a scenario, the price of oil could easily fall way below the lows we saw earlier this year.

But for now I don’t foresee an imminent global demand shock. In my previous article, We Need To Talk About China, I discussed the implications of China goosing its economy long enough so that it will make it to the government reshuffling next fall. It is important to watch state investment in RoC terms which should continue to decline into the winter months, and could put significant pressure on this thesis. China has to be very careful here and realize just how fragile their economic counter attack has left them. Meanwhile the private sector showed a modest improvement, but most likely will not come even close to carrying the load necessary to get China to the government reshuffling.

In order to cross the finish line, state investment in the commodity heavy enterprises will have to continue to be the major drive of Chinese economic growth which should continue to push inflation higher. The Li Keqiang index has sharply rebounded from record lows earlier this year, and is likely to continue to remain elevated for at least the next few months.

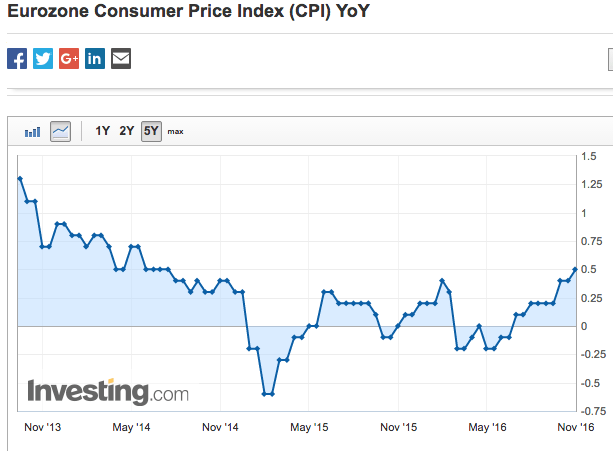

OPEC + Russia combined with China’s inflationary policies should have a huge impact on European inflation which had already bottomed and had been trending higher throughout the year.

A lot of folks are calling for EUR/USD parity, and I am one of them. But perhaps the timing of that call may be a little bit further out than we anticipate.

I remember in the summer staring at this obviously dead end currency with an insolvent banking system scratching my head to as why anyone would use this multi-colored paper for anything other than kindling. But now I’m going to offer a different perspective.

One of Europe’s most glaring problems is its insolvent banking system. The banks cannot lend because the yield curve is as flat as a pancake that was thrown in a NIRP hole. The European bank business models were supposedly dead in this environment, and they were… But inflation is rising and with it the long end of the yield curve is set to go much higher and the banks will be able to breathe a temporary sigh of relief.

Given these rising inflationary pressures, one might think the ECB would be all hands on deck, but the ECB is a monolithically slow and reactive institution that will not be able to turn the ship in time. Draghi has only just announced the smallest of tapers while extending the duration of QE. FFS a three toed sloth on more quaalude than The Wolf of Wall Street has faster reflexes than these guys.

The ECB will still be pumping QE into this inflationary environment. Now you can make a very good argument that the ECB is not buying bonds to push up inflation, but maintain the low borrowing costs of the insolvent nations that make up the EU. And this is quite valid for it has certainly helped suppress Euro area sovereign bond yields and contributed to the the record spreads between US and European sovereigns.

This ridiculous mis-pricing in European credit over US credit is even more insane when one looks at Italian bonds. This is the same economy where 20% of its loans are non-performing.

But then you must consider the ECB’s credibility is at stake and the market will be more than happy to serve these technocratic sloths their much deserved humble pie. Imagine inflation hitting 1.5% over the next few months with an accelerating trajectory. In spite of the ECB’s QE, long term rates could begin to rise, and we would start to hear rumblings of a potentially accelerated taper out of the ECB further pushing rates European sovereign rates higher.

At the same time, US rates may have gone a little too far too fast. The Trumpflation narrative appears to be on the verge of tipping over. Yet again it bares repeating, from my recent post, It’s a Trap!:

“Donald Trump much like Alexander Hamilton has promised drastic change in a time of hidden crisis. To these men it was clear that the final battle had not yet been fought, but the majority of the population did not share their sentiment.

In order to win the election, Donald Trump successfully united a diverse group of people and yet he didn’t win the majority vote. And although the republicans may have won congress, Donald is hardly a republican president. Donald Trump is akin to a battle commander who has charged too far ahead of his troops. He will need to wait to gather the army before he can launch an effective attack.”

Lo and behold the Republican establishment is now prepared to fight him on his stimulus package and tax cuts. Of course these are the same folks who rolled over for Obama as he added $10T in debt in just 8 years.

The fact remains, that expectations of US fiscal stimulus have gone too far and will have to be reigned in considerably as reality sets in. This should translate in significant downward pressure on US yields which once again should further tighten the record spreads between US and EU sovereigns.

A lot of what I have discussed, will also have tremendous implications for Japan but that is for another post. For now, I’d like to end this post with a chart. This time, of the wonderful EUR/USD that has staunchly held the 105 line for over the past 2 years now. I believe it will one day break, but not today, and not very soon. As you can clearly see, RSI momentum has diverged from the overall trend. If we do see a stronger Euro, like most the recent moves, this will be something to fade. #HeadFake

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.

Pingback: Keeping Up With The 2017 Predictions – The Klendathu Capitalist

Pingback: Euro vs Dollar: Ecks vs Sever – The Klendathu Capitalist

Pingback: Buy Low: Cripples, Bastards and Broken Things – The Klendathu Capitalist