I know what you are thinking, “Hey kid, it’s only been a week. Your predictions aren’t even cold yet!” Just humor me. I believe this thesis has continued to play out and there are important developments that I need to talk within the context I have previously provided. That context being that rising inflation due to both China’s temporary rebound and higher oil prices would lift Developed Market inflation much higher than current expectations.

I expected and continue to expect, that this pulse of inflation (DM central bankers better hope its just a pulse) would be highly disruptive, catching a lot of investors and central planners off guard. Although we are only a little over a week into the new year and 2 weeks removed from that post, I think some important data has come out that further supports this thesis.

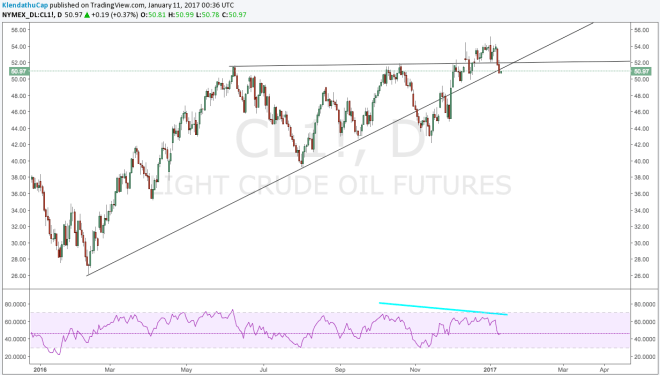

For starters, crude oil is up +80% YoY. Although it’s not looking the best, technically speaking.

But Saudi Arabia appears committed to this production cut…

As does Iraq…

Meanwhile Iran has dumped its excess oil onto the market and the price of oil is still above $50.

But most importantly, Russia has started to cut production.

https://twitter.com/Lee_Saks/status/818339003254587392

The addition of Russia, to the production cuts is potentially a paradigm shift in the oil markets. OPEC+Russia is a new cartel the likes of which we haven’t seen in decades. Recall just over a month ago, when Qatar and Glencore bought a portion of Russian Oil Giant Rosneft.

“With this bit of news, the OPEC production cut, in my estimation, has gone from an act of desperation to a smart gamble. OPEC+Russia now produces half the world’s oil, making it a much more formidable cartel. A cut of 10% of their production would amount to over 4 million bpd, the likes of which North American shale could simply not keep pace with.

But I’m not suggesting they do that all at once. This new cartel will likely take the Federal reserve’s approach of slow and steady moves. IF this first relatively small cut holds and by that I mean the price of oil stabilizes somewhere over $50, I could easily envision a scenario when as early as this spring we see significant chatter of a future cut that could come this summer. In essence, the cartel would force the market to price in additional production cuts before they even happen. OPEC+Russia future production quotas could become the new Fed dot plots.“

So far so good. But where am I going with this? Well that inflationary pulse from oil base effects may have lasted only a few months, but now with this new cartel, the price of oil could continue to rise potentially above $60 further pumping inflation into the NIRP districts of Europe and Japan. And perhaps the most overlooked dynamic of OPEC’s production cut, are the guys they’ve ceded defeat to, US shale.

Their “enemy”, US producers, have hedged 50% more production than they did going into the summer of 2014. Getting rid of them during the next plunge would be even more difficult, and it was already bloody difficult when they were totally unprepared. Adding that the OPEC member countries still haven’t recovered from the prolonged low price of oil (you don’t create a massive revamp of your country and IPO your national treasure if things are going swell). It seems suicidal for them to let the price fall, and restart the all out pump war.

To look through the lens of game theory, it is now in each member’s self interest to ensure the success of the production cuts. That speaks to a low probability of failure, although it must be noted that if this new cartel does fail, the downside to the price of oil is tremendous. Assuming, $50 oil for the next few months, it will be interesting to see the BOJ and the ECB try to sell their negative interest rate policies to their citizens.

Although in Europe no one is panicking… yet.

As a matter of fact the EU economy has responded quite well to this inflationary pulse. Remember folks, a little inflation always feels good in the beginning. Especially after a long deflationary drought. They say hunger is the best sauce, and it seems the Eurozone is proving that to be true. From Economic Calendar:

I’ve been calling for a bottom in the Euro since mid-December. The record spreads between US and German bond yields were particularly out of whack. Now that inflation is surging higher in Germany, I expect this spread to tighten.

Higher inflation, combined with rising rates and strengthening European economies, further supports the rebound in EU banks. These “failed and insolvent” institutions should continue to climb that wall of worry we all know so well.

From a technical perspective the charts on some of these banks are starting to look quite constructive as well. (DISCLAIMER: I OWN SHARES IN RBS)

“Come spring of next year, trend followers will be tripping over themselves to get a slice of these no longer “dead beat” banks. With their banks no longer in free fall, and rising interest rates, capital should flow back into these economies. Given the huge flows into US as of late, I suspect the EUR/USD carry trade is about to unwind.”

The technical back drop for long EUR/USD also looks quite compelling.

The refusal to break to parity despite pleas from dollar bulls is another strong case for a turn around in the Euro. Readers of my blog will recognize this chart. Notice how the momentum has continued to diverge from price.

But once again, it is important to remember that this is all a head fake… a very powerful head fake but a head fake all the same. Debts are too high to sustain any real move in interest rates. It is simply shocking how little talk rising LIBOR has received of late.

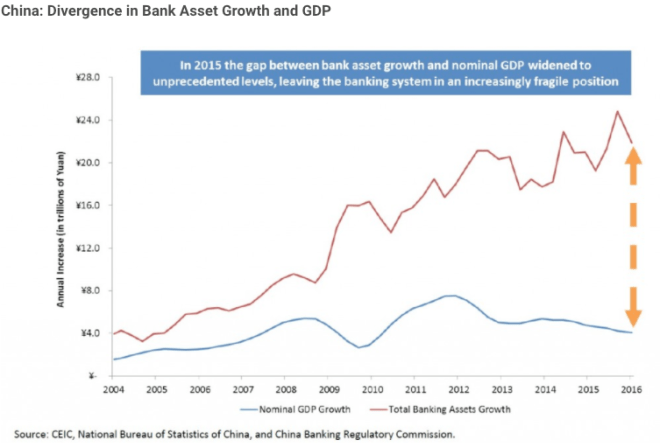

But of course, I’ve been ignoring the elephant in the room, China, and its increasingly large and increasingly fragile debt bubble.

If you go back and read Kyle Bass’s letter from February 2016 (and I highly HIGHLY suggest that you do), you’ll notice part of his thesis was built around the fact that Chinese SOE profits had turned negative, and could no longer service their massive debts. Those debts are at the center of a massive speculative and interconnected bond bubble I might add (but we’ll get to that later). From Kyle Bass’s letter:

“As it is obvious that China’s economy is slowing and loan losses are mounting, the primary question is what are China’s policy options to fix the current situation?”

Yes it was obvious. Look back at the chart, Industrial profits were negative. Everyone knows you can’t service a growing debt burden on negative profits. Unlike the 08 financial crisis, where the central authorities, Fed and US treasury, were completely oblivious to the actual problems, the Chinese authorities knew exactly what the problems were. So what Kyle Bass missed was that the Chinese authorities were planning a Battle of the Bulge type counter attack in the form of a massive stimulus push. And since then, Chinese SOEs have roared back to life with profits turning positive for the first time in 2 years.

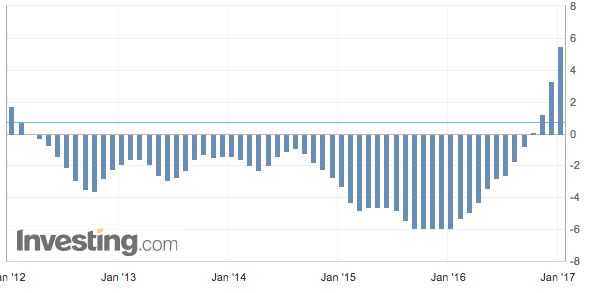

It would be foolish to think this stimulus is one, without cost, and, two, is sustainable. The Yuan took this inflationary policy on the chin. Despite spending $400B in reserves to defend the Yuan, it still fell 8% against the dollar but arguably even more important, is inflation which has taken off. Producer prices surged the most in over FIVE YEARS!

Chinese PPI

Higher inflation will push interest rates up and as victims of the US housing bubble will tell you, it’s hard to sustain a speculative debt bubble when interest rates are rising.

Although that won’t stop China from trying. After an arguably disastrous 2016, stability has now become paramount in the Middle Kingdom. From Bloomberg:

“The price was too high, the leaders agreed, according to a person familiar with the situation. The buildup of debt used to fuel smokestack industries from steel to cement had helped win the short-term battle for growth, but the triumph itself undermined the foundations of long-term expansion, the leaders decided, according to the person, who asked not to be named because the meeting was private.

What followed was an order to central and local government officials that if they are forced to choose this year, stability must be the priority while everything else, including the growth target and economic reform, is secondary, said another four people familiar with the situation.”

That sounds vaguely familiar. From We Need To Talk About China:

“Despite the 6.7% growth, 2016 has not been a good year for China. I’ll be the first to admit that I do not fully understand why Xi is waiting for the government reshuffle next fall. In spite of the smoothest GDP growth in economic history, I find it hard to believe that higher debt levels, smaller FX reserves, and rising shadow bank risk will be any more manageable under a regime where he has “full” control.”

It looks like the Chinese authorities agree with my assessment. Economic stability will now be prioritized over everything else including economic growth and reforms. Not exactly music to the ear of an investor who put money into China on the hopes of +7% GDP growth and a stable currency.

Which begs the question, how do you maintain stability while at the same time slowing your debt fueled economy without it tipping over? Given China’s shadow banking risks (which I’ll get to later), and the bond panic in December, the simple answer is you can’t. Like riding a bicycle, the closer your speed approaches zero the harder it is to balance.

And In China’s case they are riding a bicycle while spinning half a dozen plates of uranium at once while juggling a pair of Molotov cocktails. If they slow down too much, they will not only crash, they will explode. It will be interesting how local governments interpret this seemingly contradictory directive of stability over growth. If the PBOC is any indicator, we are about to witness some very odd behavior coming out of the Chinese Authorities.

Although given the recent price action of iron ore, when it comes to China we should always expect the unexpected.

Because clearly iron ore is in short supply in China… or not.

Perhaps demand is set to sky rocket as China seeks to further build out OBOR projects as well as domestic projects… or not.

Or perhaps, investors are panicking about what to do with their falling currency and are trying to hedge it. There’s a certain level of irony (pun intended… I’ll wait) that the largest source of instability in China comes from a “pegged” currency. It seems self evident that China’s pivot towards stability would include a stable currency but given the rising inflation, slower growth pivot, dwindling reserves and lack of defensive options, one wonders just how long they can support the Yuan.

A falling Yuan is perhaps the worst thing that could happen for the Chinese Authorities. For one it undermines their credibility. Secondly, it forces the PBoC to intervene and drain liquidity from the market. And finally, it pushes inflation higher as the value of imported commodities and goods rises. With that said, recall that the Chinese bond market is a massive intertwined web of hidden risk, and in a falling liquidity and rising inflationary environment it will get butchered worse than the younglings in Star Wars Episode 3: Revenge of the Sith.

Once again getting back to Kyle Bass’s thesis, it’s important to note the key role both Wealth Management Products (WMPs) and Trust Beneficiary Rights (TBRs) play in the Chinese Banking System. As the sticky systemic glue that binds the over-levered Chinese banking system together, they will be the focal point of any meltdown. From Kyle Bass’s letter:

“TBRs are one of the biggest ticking time bombs in the Chinese banking system because they have been used to hide loan losses.The table below illustrates how pervasive TBRs are throughout the Chinese banking system. One can make many assumptions regarding the collectability of such loans, but our takeaway is that the system is already full of massive losses. Pay particular attention to the column of the ratio of TBR’s to loans on each bank’s books.”

We saw just how potent TBRs can be when Sealand Securities, a midsize brokerage firm, suggested it would default on loan contracts due to a “fake seal”.. or as I used to say in elementary school, “my dog ate my homework”, although honest to God, one time it did, so maybe we should give Sealand Securities the benefit of the doubt.

Although, the Chinese bond market certainly didn’t. Bond values plunged and the PBOC was forced to inject $23.7B of liquidity in one day. By the end of the month, the PBOC injected a record $120B in liquidity. Recall, this all came against the backdrop of the highest SOE profits in over 3 years! It didn’t matter that the underlying fundamentals of the debt had improved (albeit temporarily), the bond market still cracked!

So if the situation is this bad that not even a medium size company can default on its TBRs without sparking a major panic, then how are the authorities supposed to “maintain stability” without pumping more liquidity into the system? And how can they pump liquidity and credit into the system without pushing down the Yuan? And how can they maintain stability if the currency is falling?

You see where I’m going with this. It’s not difficult. I don’t believe nor claim to have any unique insights. If there’s anything that I do possess whether right or wrong is a high conviction level which allows me to see through all the smoke screens put up by the Chinese Authorities.

With that said, I do believe there is some room over the short term (1-2 months), for China and the Yuan to surprise to the upside. They’ve done a relatively good job shifting the narrative these past few days. Although I’d say hiking HIBOR to 105% reeks of desperation, it’s not my opinion that drives markets (if only).

I also see incredible potential for the PBOC to defend the psychologically important $3T reserve level this month. Come the release in February, the market may be shocked to discover that the reserve level has held. The Yuan could strengthen, with bitcoin falling to the low 700s if not lower. The narrative would temporarily shift to the masterful job done by the Chinese Authorities, and developed markets would rally on the back of higher inflation. Of course all of this would ignore how the PBoC managed to hold the line. From Bloomberg:

“Financial regulators have already encouraged some state-owned enterprises to sell foreign currency and may order them to temporarily convert some holdings into yuan under the current account if necessary, they added.”

The Chinese Authorities, lauded for their long term planning, are actually some of the best short term fixers the world has ever seen. Their ability to pull any and every lever necessary to kick the can down the road is both impressive and incredibly myopic. And sadly, the game, now in quintuple overtime, is almost over. The players are about to drop dead from exhaustion and this is the part where I agree 100% with Kyle Bass:

“Once analysts, politicians, and investors alike realize the sheer size of the impending losses and how they compare to the current levels of reserves, all focus will swing to the banking system.

As it is obvious that China’s economy is slowing and loan losses are mounting, the primary question is what are China’s policy options to fix the current situation? We believe that a spike in unemployment, accelerated banking losses / a credit contraction, an old-fashioned bank run, or more likely the fear of one or all of these events, will force Chinese authorities to act decisively.”

Although we aren’t there at this point, we are very very close. What separates China’s coming crisis from the US’s in 08, it is that will happen not because the authorities failed to notice the problems, but because they have exhausted all short term stability mechanisms. My argument today is that they are already completely out of ammo, and the last shoe to drop is the narrative. Although they can manage the narrative for a few months, to think they can last the year is a bet I would not make.

The Klendathu Capitalist apologizes for his bearishness but sees few alternatives. Like the ’08 crisis, we should expect higher inflation before severe deflation. One only has to remember the Fed’s repeated rate cuts that pushed inflation and commodities to record highs in ’08 right up until the US economy imploded.

Once again we are on the trapped in the middle of a similar set of circumstances this time originating from China. It doesn’t matter what Trump does or doesn’t do, he is almost irrelevant when it comes to China’s short term debt cycle which was going to correct with or without him. But he certainly makes for an entertaining sideshow, distracting US investors and business.

Lastly, DB put out a list of 30 things for investors to worry about. Curiously, the Yuan-USD peg was missing. As Jay-Z once said, I got 30 simple issues and the Yuan-USD peg ain’t one.

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.