I think of myself as a China bear, and yet a lot of my growth based investments revolve around China. It’s the elephant in the room that we are all forced to take into account with every investment decision we make. Whether it be its massive demand for resources or equally massive infrastructure build out, China has shaped the world in ways the US has not done for decades, but China is pivoting. The things that China needs to continue its ascendant path have changed and the world will be forced to adapt.

China’s battle versus its dirty growth model has reached a heightened level as of late. Although the government will continue to push debt and stimulus through the system to prevent a deleveraging, there is only so much smog the citizens can take. With bitcoin breaking above $1000, the year is off to an ominous start in China.

But China will and has been pivoting to a cleaner growth policy. Perhaps China’s first and most noticeable step forward is the build out of its electrified vehicle fleet.

Electric vehicles require an array of unique materials from relatively small and esoteric markets. For example, the lithium market is incredibly tiny and run primarily by three companies. A large portion of the world’s cobalt comes from the Democratic Republic of the Congo, of which China has already secured a sizable portion of, leaving little for the Western companies such as Tesla to use for themselves. Then of course there is graphite, which makes up the anode of the lithium ion battery. The mining of graphite is an incredibly dirty process. China is already the world largest miner of graphite and it will be interesting to see how they strike a balance going forward.

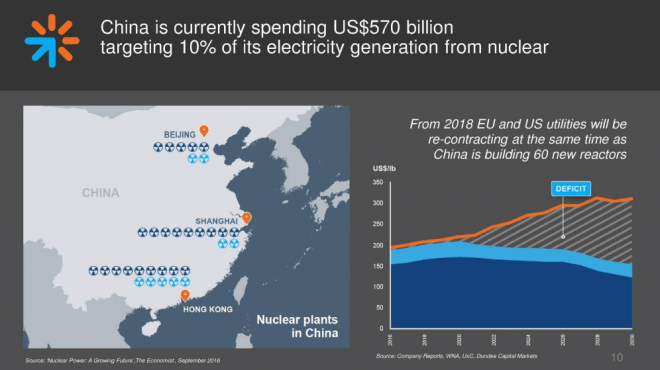

Although supporters of electric vehicles at times suggest electricity from the grid is cleaner than a gas powered car, that isn’t always the case, especially in China where the bulk of grid power comes from old and inefficient coal fired power plants. So China cannot simply switch to electrical cars and buses and call it a day. Which is why it is building out a huge number of nuclear power plants. For those interested in the case for Uranium, I recommend “Uranium: The Falling Radioactive Knife.”

At the same time, China cannot easily abandon the “environmentally dirty” policies that have lifted hundreds of millions of people out of poverty. These industries still employ millions of people. And of course there are trillions of debt tied to these slowing sectors that cannot be simply erased with the sweep of a broom.

In large part this is where the One Belt One Road policy comes into play. China will continue its infrastructure growth model in other countries where the ROI is much much higher. The money to finance these projects will come from China. Chinese banks will lend cheap Yuan to State Owned Enterprises who will in turn export China’s infrastructure boom to the central and south Asia.

There is an obvious flaw in this strategy (Hint: commodities are priced in dollars not Yuan), but on the surface, China’s OBOR program is an ingenious move that widens China’s sphere of influence, and also eases China’s difficult economic transition. At an order of magnitude larger in size than the US’s post WWII Marshall program, it is an effort the likes of which the world has never seen and will shape the world for decades to come.

But is the OBOR’s enormous size, more a function of the massive imbalance in China than prudent investment policy? Under Hu Jintao, power was more distributed, which led to rise of powerful vested interests. These vested interests delayed the necessary pivot which in turn has led to an insurmountable build up of excess debt and risk within China. It now takes seven units of debt for every unit of GDP growth. China has put a lot of eggs in this OBOR basket, and needs it to not only pay dividends for the long term, but as things become more and more unstable in China, for the short term as well.

Which brings me to the issue of time horizons. As a small investor I have a hard enough job matching my time horizons with my position sizes, although part of that I will blame on China’s inability to do the same. For me, it is becoming abundantly clear, that the time horizon for China’s OBOR program does not match up with its shorter term debt cycle.

We’ve seen the liquidity crisis in the bond market force the PBOC unleash a record amount of liquidity last month. With inflation rippling through the economy, the PBOC’s days of easing the economy with record amounts of stimulus are coming to an end. Instead of easing liquidity, stimulus will push inflation and interest rates well above the safe levels. These recent instabilities have fueled further capital flight. And despite talking a tough game, with each passing month, and feeble attempt to stop further capital flight, the PBOC is showing the world just how weak its hand truly is.

From the FT:

“Investment professionals, however, have queried how the ultimate use of the money could be verified. “If someone transfers money for overseas study or medical treatment, how is the bank supposed to check what they really spend the money on,” asked Kelly Jiang, a Beijing-based real-estate agent who helps Chinese investors buy properties in London. “

Like all governments, the CCP is only as strong as its citizens allow it to be. With the Yuan in a virtual free fall, the crowd of “speculators” picking off the PBOC is growing into an army. And of course, there is another short term cycle that is completely out of their control and in the hands of a seemingly hostile actor, Donald J. Trump.

In my 2017 Predictions, I largely ignored The Donald. This is a bit of a copout on my part, and yet, given my other assumptions (to be discussed later), and lack of knowledge on the subject of Donald Trump’s inner strategy, I find this to be the best position for me to take. My mother, chided me for such a foolish move. I’m sure the Chinese Authorities will not make the same mistake. On the surface, The Donald is a paradigm shift in US politics and not taking him into account is likely to bite some of my predictions in the butt.

At the same time, given my belief that the US consumer is quite weak, and the tightening Fed policy will exacerbate their overall health, I find it quite likely that Donald’s positive impact on the US economy will be minimal during his first year on the job. And let’s not forget the US election cycle’s correlation to US recessions. From Raoul Pal’s Global Macro Investor:

“I recently noted that since 1910, the US economy is either in recession or enters a recession within twelve months in every single instance at the end of a two-term presidency… effecting a 100% chance of recession for the new President.”

Policy makers can steer the economy when it is moving with speed, but once it stalls, it doesn’t much matter what you do, turning the wheel doesn’t change the fact that you are stopped. Just recall the last two US recessions, when the Fed slashed interest rates to record lows (at the time) and still the US economy slowed, stocks fell, and bubbles still burst.

The evidence continues to point to similar circumstances. We are seeing the late cycle inflation that exacerbates the record high debt loads. We are seeing the US consumer roll over. And although the dollar may weaken in response to the slower US economy, the reprieve the Yuan will feel will be temporary. In the end, the rest of the world will follow the US down, and the larger forces driving the dollar higher will reappear. Most importantly, despite, the OBOR program, and China’s other efforts to diversify itself away from the dollar and the US sphere of influence, China will find itself pulled down with the mythic force of Charybdis.

Time horizons, position sizes, lithium batteries, nuclear power, and The Donald, I realize this article is all over the map. So here is my attempt to rein it in. China is a system, and like any other system, it has its limits. As it bumps into those limits, variables become constants, and the predictions become easier. The paths to China’s success are dwindling by the day. This post has been my attempt to illuminate the available paths, and their potential pitfalls. Relying on China to stay afloat forever, is a fools errand, but one that has worked out well for the past few decades. Although I believe the sands in China’s hourglass are almost out, I also believe that some of the pathways in front of us are too tempting to not explore. #StayHedged.

Disclaimer: This blog post is not advice to buy and or sell securities. I am merely informing you of my intentions. If you act on the words of a twenty something millennial over the internet you have only yourself to blame.