“Shit escalates.” ~ Sevro au Barca, Golden Son a novel by Pierce Brown

“If you do not know where you come from, then you don’t know where you are, and if you don’t know where you are, then you don’t know where you’re going. And if you don’t know where you’re going, you’re probably going wrong.” ~ Terry Pratchet

My predictions for 2017 follow two simple rules, shit escalates, and it’s so crazy that it just might work. You’ll know which prediction follows which rule when you see it… Trust me, I’m from the government and I’m here to help.

But as the wise Terry Pratchet once said we can’t make predictions for 2017 without discussing the disaster that was 2016. An obvious statement, and yet a necessary one. 2016 started off with consensus believing bond yields would rise to the 3% (at least in the US). But China’s unstable economy threw investors off balance in the January sell off. The middle kingdom’s economy, on the back of a super yuuuuge stimulus push, made a local bottom shortly there after.

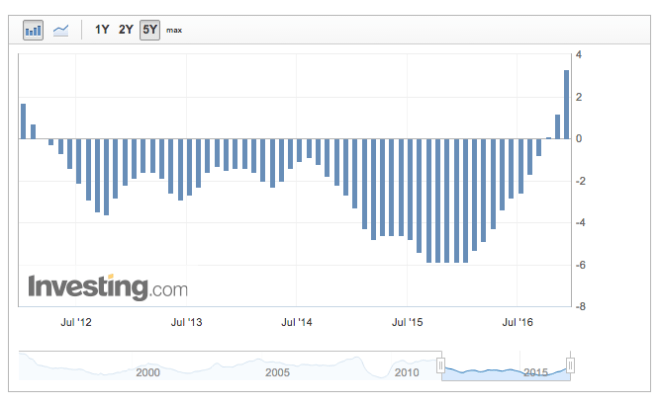

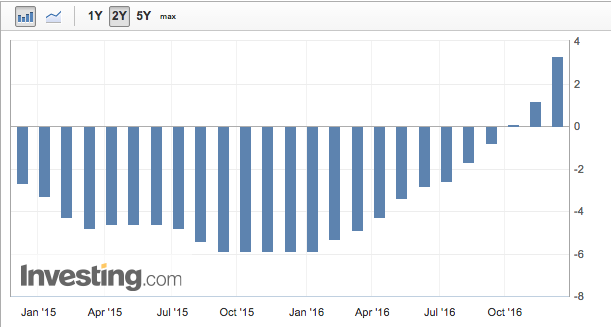

Even though China’s economy bottomed, it still took months before it stopped exporting deflation to the rest of the world. And because China had been exporting deflation for so long, the market became convinced that deflation would continue in perpetuity. What the market and more importantly Central Bankers were missing was the fact that deflation in China had in fact bottomed, and although negative, was rising sharply.

Chart of Chinese Producer Price Index (PPI)

This turn from deflation to inflation also fooled Chinese investors who piled into the record low bond yields. In fact, investors’ response to these rising inflationary pressures was so slow that yields in China did not bottom until PPI had already turned positive (for the first time in over 4 years)!

Chinese PPI

And this is where things get very tricky for the Chinese authorities. They wanted this inflation. Just not this quickly. Locked in a deflationary debt spiral, a little inflation is a gift from the financial gods, BUT rip roaring inflation has the nasty effect of pushing up bond yields which in turn tightens financial conditions. And although we have not yet seen rip roaring inflation, China has gone from DEEP deflation to rising inflation within 12 short months. The Chinese Authorities are clearly aware of this shift, but it’s unlikely that they acted fast enough. The PBoC did not start tightening liquidity until a month before PPI turned positive.

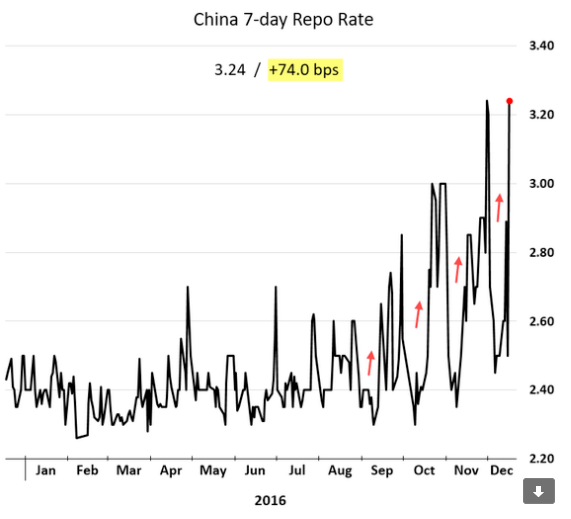

It needs to be said, that by comparison, the PBoC is light years ahead of their western counter parts, the BOJ in particular. The BoJ pinned bond yields to the floor the same month that Chinese PPI had turned positive. But we’ll get to this later. For now let’s place our focus back on China where the PBoC has been tightening liquidity since September. Which brings me to my first prediction, which is more of a backward looking statement.

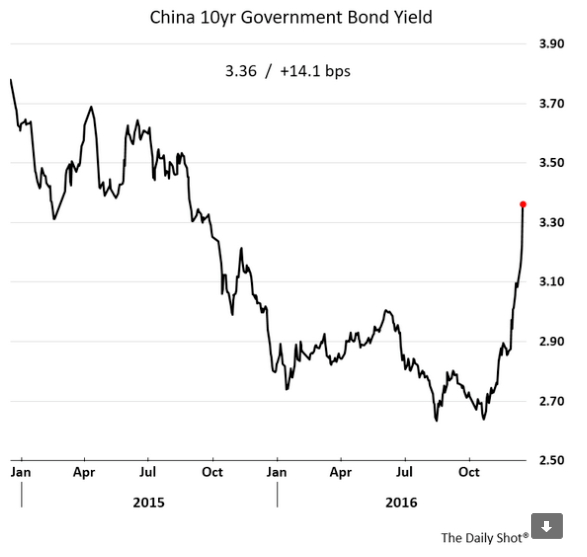

#1. We have likely seen the top in the Chinese bond market.

Philosophically speaking, a peak in bond values means that risk is growing. Given the predicament the Chinese authorities find themselves in, caught between Scylla and Charybdis, this would seem like a rather obvious statement. On the one hand, we have seen how little room they have to tighten before the deflationary pull of Charybdis overwhelms their economy. To reuse my Battle Of The Bulge Analogy:

“The Chinese government to use yet another historical reference, has engineered a counter offensive akin to the Battle of the Bulge in WWII. Right up until the battle it was perfectly clear that Nazi Germany was going to lose the war. Nazi Germany was quickly crumbling under the multiple fronts, dwindling resources, and Hitler’s repeated mistakes. And because of all of these “facts”, the Allies under estimated the Nazi Germany’s strength and paid dearly for it.

Nazi Germany threw everything it had into that battle and once it was over, the regime quickly crumbled less than four months later. Economic cycles last much longer than war cycles, so I’m not saying China is less than 4 months from collapse, but that once the stimulus fades, the economy will roll over hard and fast.“

HIBOR is approaching levels last seen in the January sell off.

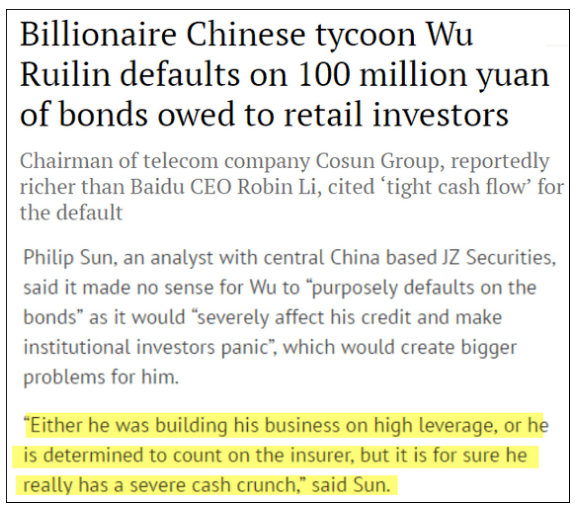

In fact liquidity is so tight that just recently, a MULTI-“billionaire” defaulted on just 100 million Yuan worth of debt. I use quotes, because anyone can be a billionaire if they borrow a few billion dollars and ignore the liability side of their balance sheet.

I’m sure he’s not the only one swimming naked. Wealth management products are incredibly susceptible to higher interest rates. These ponzi finance vehicles have increasingly invested in each other which has pushed counter party risk exponentially higher. From WSJ:

“Some 40% of the assets in wealth management products—the biggest portion—was invested in bonds as of the first half of this year, up from 29% in 2015, according to Moody’s Investors Service.”

This interconnectivity of WMPs has further restrained the PBoC’s ability to tighten. In spite of rising inflation, if the PBoC wanted to keep the economy going they would have to inject more liquidity… and that is exactly what they did. From WSJ (my emphasis in bold):

“On Friday, the PBOC tapped an emergency lending facility it created in 2014 to extend 394 billion yuan ($56.7 billion) in six-month and one-year loans to 19 banks. That pushes the net amount extended through the facility to 721.5 billion yuan so far in December, a monthly record, according to Beijing-based research firm NSBO.”

The Chinese government finds itself in a constant battle against short term destabilizing forces. Every time it tries to take its foot off the gas, the economy gets pulled in by Charybdis, prompting even more Cow Bell. I’m mixing metaphors but you get the point.

On the other hand, they can no longer stimulate as much as they want or else they’ll face, Scylla, the nine headed inflation monster that will rip their debt to shreds. It is quite likely that China has now reached the point where stimulus’ effect on the economy over the medium term is net negative. More specifically, more stimulus pushes inflation higher which in turn tightens liquidity and defeats the purpose of stimulating in the first place. My guess is that the recent monthly record of stimulus injections will show up in the inflation data much sooner than the Chinese authorities would like.

But why are they doing this? Surely they don’t believe this is sustainable? To once again use my Battle of the Bulge analogy, this time from the perspective of “the other side”.

In the article, a German tank officer is asked about what thoughts were running through his head before the now famous Battle of the Bulge.

The Chinese authorities may be trying to walk an atomically thin line but they still have hope. They can see the finish line! It’s just nine months away to the government reshuffling. They can surely make that. Right? Unfortunately, the German soldiers weren’t able to buy time for the full 3 months. The battle ended after just 40 days.

Which brings me to the thorn in the Chinese Authorities’ side, capital flight. For if there’s anything that’s going to derail the government’s plans it is capital flight. Thanks to increased stimulus fueling the weaker currency, rising inflation, and tighter financial conditions, capital flights has re-accelerated. Once again stealing from We Need to Talk about China:

“…to use yet another WWII analogy, the Yuan would be fighting a war on two fronts. Rising inflation coupled with rising demand for safety would only add more fuel to the dollar shortage inside China. This short period of strength the Yuan has enjoyed from tighter monetary policy is likely over. With the 7 handle in sight of USDCNY, FX reserves should deplete much more quickly and once again reenter back into the consensus narrative.”

This voracious demand to diversify out of the Yuan is exactly what we are seeing. From Bloomberg:

“A wealth management product from China Merchants Bank Co. in Shanghai last week, paying 2.37 percent annual interest on U.S. dollars, sold out in 60 seconds flat.”

Investors do not even care that this WMP is likely invested in a host of other WMPs nor do they care that inflation is already higher than the offered yield. For now dollar denominated WMPs may be the next gimmick to keep the ponzi-scheme going. There certainly is no shortage of demand here, from Bloomberg:

“In November, banks sold 49 percent more foreign-currency denominated wealth management products, most of them in U.S. dollars, than in October, according to PY Standard, a Chengdu-based wealth management research and ratings firm that tracks the data. November’s foreign currency deposits increased 11.4 percent from a year earlier, more than double the 4.8 percent rise in October, according to the People’s Bank of China.”

And of course, one only needs to look at the performance of bitcoin to get an idea of the state of Chinese capital flight. As of writing this article, Bitcoin crossed $900.

China has limited tools to fight this continued capital flight. Normally a country could hike interest rates, but the fragility of the Chinese debt bubble has proven this to be impossible. The other economic option is to grow fast enough in dollar terms to attract foreign capital. Given the debt, instability, and slowing economy, that is not likely to happen either. As of writing this article, Xi Jinping indicated that he expects the economy’s slow down to continue.

Nobody attacks this Chinese “stabilization” narrative better than Jeffery Snider. From Alhambra Partners:

“If you had proposed a stabilizing Chinese economy in the middle of 2014 it would have meant with IP at 9%, not 6%. And if you had done the same in 2010, as many policymakers and economists attempted, production would be growing at 13% not 9%. The Chinese economy, as the global economy, gets weaker not in a straight line but via clear, distinct episodes.”

So China is really left with just one option which is to close the capital account down, and restrict almost all outflows. This method has worked for as long as it hasn’t really worked. What I mean by that is as long as companies did not have trouble getting their profits out of the country, this was a viable strategy. But clearly capital was fleeing the country, likely much larger than the PBoC is willing to admit, thus the PBoC was forced to implement more effective (stricter) capital controls.

The problem with strict and rigid capital controls, is that they also hurt foreign businesses trying to do business in the country. As the business environment becomes more and more unfriendly, foreign and local companies will begin to pull back investments. From the WSJ:

‘”A majority of clients are currently consolidating and restructuring their China business,” said Bernd-Uwe Stucken, a lawyer with Pinsent Masons LLP in Shanghai. Some clients are closing down their business, with new investments being the exception to the rule, Mr. Stucken said.’

To make matters worse, these capital controls were also poorly implemented further compounding the falling faith in the Chinese economy. From the WSJ:

“Adding to the confusion: it is unclear where the limits are, because regulators haven’t published official rule changes, but instead have given only informal guidance to banks, according to Daniel Blumen, partner at Treasury Alliance Group, a consulting firm.”

“That’s when a $50,000 cap on how much foreign currency individuals are allowed to convert each year resets, potentially aggravating capital outflow pressures that are already on the rise. If just 1 percent of China’s almost 1.4 billion people max out those limits, that’s an outflow of about $700 billion — more than the estimated $620 billion that Bloomberg Intelligence estimates indicate has already flowed out in the first 10 months of this year.”

The communist party has done a commendable job delaying the inevitable but 2017 will be the year where the cracks become to wide for even the guys on CNBC to ignore. Which brings me to my next prediction.

#2. USDCNY will surpass the mythic 8 level.

- And given the correlation between Bitcoin and the Yuan, I will add a corollary to this prediction which is for Bitcoin to exceed the all time highs of $1200. Although I’m not exactly calling for gold/bitcoin parity but I’ll get to that later.

It is important to note that the PBoC can still inject liquidity into the system for a few more months before inflation reaches intolerable levels. But as long as Chinese Authorities prioritize short term stability over long term stability they, and by proxy the rest of the world, will suffer much higher inflationary pressures.

The developed world is not only ill-prepared for but almost completely ignorant of these rising inflationary pressures. At least the Fed is hiking and promising to hike even more. Unfortunately tighter Fed policy only compounds China’s capital flight problems. But what is the Fed to do? Given China’s inflationary path, they are likely behind the curve. From The Case For Higher Interest Rates:

“The Fed has been cornered for years, never able to unwind its policies without inviting disaster. The problem with being behind the curve is that the Fed will have to admit through policy that they made yet another mistake. If the Fed doesn’t react fast enough, inflation could rip higher pushing bond yields to intolerably high levels.”

The Fed’s addition of a 3rd rate hike in 2017 is likely to be a prelude to a much bigger admission. But that doesn’t necessarily mean that the dollar is about to rip higher.

No comment.

Although the three additional rate hikes haven’t fully been priced in, the market is now aware of the possibility. On the other hand, the market is currently unaware of any rate hike or tighter monetary policy from the ECB or the BOJ.

Although the ECB did taper.

Sorry, the ECB did NOT taper…

But remember those powerful inflationary forces that China is likely to export to the rest of the world? Well they’re coming to Europe and Japan, where rates are NEGATIVE. And let’s not forget that oil is up 40% YoY and soon to be rising. Recall oil was in the 20s into the end of January, $50 oil would translate into a 66% YoY move. Can you say, “HELLO inflation?”

Which brings me to the ECB’s CPI forecasts. If this institution had no power, and the “elite” people working there did not devote their entire lives to managing the economy based on unknown information, this would be adorable…

#3. The BOJ and the ECB tighten monetary policy, and potentially end NIRP.

In the face of rising inflationary pressures the ECB and the BOJ will be forced to tighten monetary policy. They may even consider using the opportunity as an excuse to end the mistake that is Negative Interest Rate Policy (NIRP), although that perhaps is more unlikely than it seems. Negative rates allow any debt level, no matter how high, to be sustainable. And these economies have too much debt. The only thing keeping them together is the same thing that is slowly killing them. So they may leave those foolish policies in place but still allow the yield curve to steepen tremendously.

Take a step back and recall the mood around European and Japanese banks back in the summer of 2016. Locked in a deflationary spiral, rates were negative and falling to new 10,000 year lows. The business models of the unfortunate banks trapped in these deflating economies were unsustainable and their equity reflected it. But if we get inflation and interest rates in these deflationary trapped economies begin to rise, that narrative vanishes faster than Keyser Soze.

#4. In a phoenix like turn of events EU and Japanese area banks rise from the ashes… only to be slain once more.

Come spring of next year, trend followers will be tripping over themselves to get a slice of these no longer “dead beat” banks. With their banks no longer in free fall, and rising interest rates, capital should flow back into these economies. Given the huge flows into US as of late, I suspect the EUR/USD carry trade is about to unwind.

Not to mention that the multi decade high interest spreads between Germany and the US should tighten.

With the BOJ and ECB unexpectedly tightening monetary policy, the Yen and the Euro should rise against the dollar.

#5. The dollar pause ain’t over…

It is important to remember, that US yields have already risen dramatically. This has dramatically tightened financial conditions in the US which has its own debt problems. The US consumer is already suffering from a financial tightening that it was not prepared for, and since the US consumer is 70% of the US economy, US economic growth should slow. European and Japanese economies and currencies should out perform expectations as they play catch up.

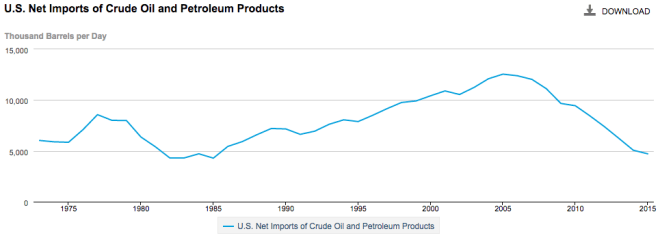

Before I get to the weak American consumer, I’d like to discuss, US shale. US imports of oil and petroleum products are one of the largest sources of dollar funding for the rest of the world. But since the advent of US shale, US oil imports has fallen by over 50%.

Combine the falling US oil imports with the falling dollar value of oil, it becomes quite evident that the US is not exporting the same quantity of dollars it once was. Because the dollar is the global reserve currency, foreign nations rely on additional dollars to fund and expand their economies. In the immediate aftermath of the GFC, the Fed made up this difference via its QE policies. But now due to the rising inflationary pressures, the Fed is tightening.

US shale is also increasing its output and locking that production in so that they can not only maintain these high levels of production but also better weather the next down turn in the price of oil.

With US dollar exports virtually flatlining since the GFC, combined with a much more hawkish policy from the Federal reserve, the amount of dollars flowing abroad is unlikely to be sufficient for developing nations to continue growing at the pace they would like. Trump’s protectionist policies if enacted will only compound these effects accelerating a short squeeze in the dollar. That is UNLESS…

The American consumer can step up to the plate and supply the necessary dollars to the global economy…

#6. Don’t be fooled by any dollar weakness the dollar bull market ain’t over.

The American consumer is tapped out and will not be able to supply the dollar funding the rest of the world requires. Real wages have not been nearly as high as advertised.

Facing a triple assault from higher mortgage rates, rising health care costs, and higher energy prices, the US consumer simply doesn’t stand a chance at supporting the global economy. Falling dollar liquidity globally will initiate a short squeeze and reignite the dollar bull market sometime in 2017.

Rising healthcare premiums made the headlines and may have turned the election in Trump’s favor. And although US shale has decreased US demand for foreign oil, the US remains a net energy importer. Higher oil prices will hurt the consumer more than it helps. Let’s not forget that natural gas bottomed in February of this year. This winter is already making out to be a cold one. Natural gas prices should rise higher, further pushing up the utility bill.

In the face of these rising costs, the US consumer has been forced to dip into their savings to maintain their standard of living. This trend is likely to be self defeating and reverse over the next few months.

And even though Americans dipped into their savings, they still slowed their purchases at restaurants, who have taken a double hit on falling margins and sales over the last quarter.

Next up on the weakening US consumer’s hit list is the auto industry. As @TeddyVallee puts it, one would be hard pressed to find a more favorable environment f0r US auto companies, and yet in spite of record discounts, low gas prices, and falling interest rates, sales fell.

And still inventories grew. Now US auto makers are laying off workers. Yet another headwind for the consumer.

#7. The US Consumer will roll over and the US will enter a recession in H2 2017.

Calls for a US recession in 2017 are much more quiet than they were in 2016. The Q3 GDP growth of 3.5% has silenced many a bear, but not this one.

It is important to note that this time last year, US shale was struggling to survive. Oil rigs were being cut left and right. Production was falling. Workers were being laid off. US shale in YoY terms should be a heavy contributor to GDP growth over the Q4 and Q1 2017. A resurgent US shale industry will likely do a sufficient job masking the underlying weakness in the US consumer. But don’t be fooled by a +2% GDP growth number in Q1, it will likely mark the high point in US GDP growth in 2017.

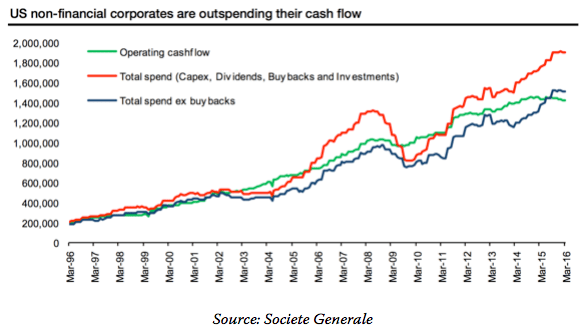

Of course, the American consumer isn’t the only one drowning in debt. US corporates have been taking on debt since 2011, and over the past two years have been spending all their profits on financial engineering gimmicks such as buybacks and dividends.

Higher interest rates will reduce US corporates’ ability to buy back stock.

But if you thought a declining growth rate, declining buybacks, European capital flowing home, and a weakening US consumer would dampen investor euphoria you would be mistaken. Welcome to Trumptopia! Or as Admiral Ackbar likes to say, “It’s A Trap!”

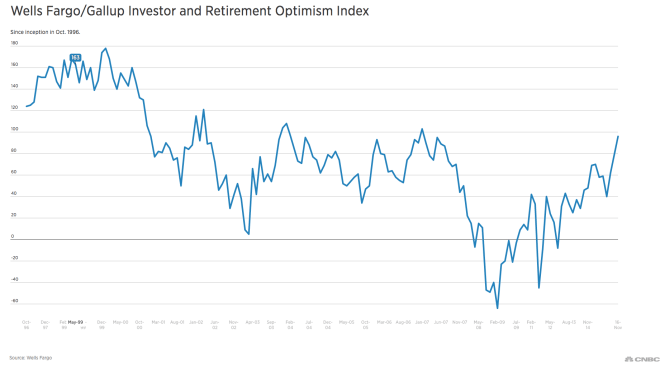

Another sign of optimism just hit a record high. Who needs cash when Trump’s going to inflate it all away?

And in case you didn’t know who to ask for information on a new cannabis strain…

#8. The US equity markets will peak in 1H 2017, and in spite of any Trump stimulus will end the year in the red.

Now as much as readers would love for me to make a fool of myself predicting what the yellow metal/pet rock formerly known as gold will do, I will say that I haven’t a clue. But perhaps you should ask this guy.

Even the bitcoin bulls are jumping on the gold bashing dog pile.

Given government’s surging desire to ban cash, and tighten capital controls, it’s hard to argue against them. Which is why I’m not, just noting the shift of yet another demographic from bullish to bearish on the yellow metal. Although I’ll remind fellow bitcoin bulls to be wary of China no longer tolerant of capital flight, regardless of the form it takes.

Back to gold. By the time a trend becomes an “official trend”, the major driving forces are no longer the major driving forces. And yet, the crowd still focuses on them with x-ray vision that cuts through the new driving forces. It is somewhere in this phase where the real forces driving the price could and do turn and yet the crowd is none the wiser because they are still focusing on the initial non irrelevant driving forces.

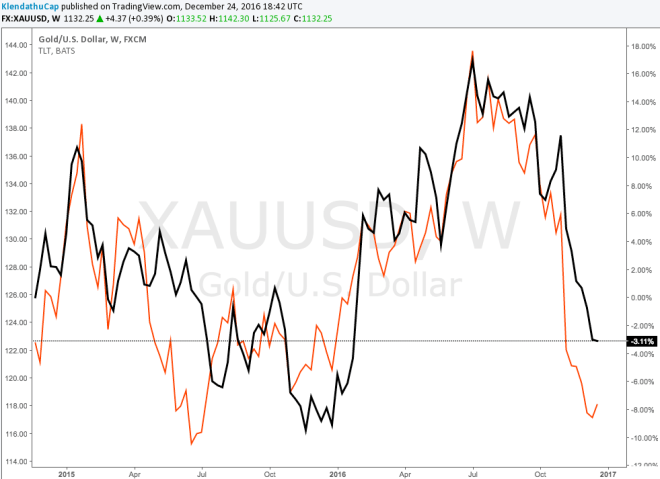

#9. Gold will break its correlation to nominal changes in interest rates.

Gold (rhs) in black, TLT (lhs) in orange

The major driving force of gold in 2016 was the addition of negative rates which prompted a deflationary state of mind. As bond yields approached the zero lower bound, and in some cases plunged through them, it didn’t make much sense to hold them over gold. Now that yields are rising, investors have jumped ship.

I expect yields in developed markets to move higher with inflation. But what if they don’t? What if rates in Japan and the EU remain suppressed due to a staunch commitment from the central banks? After all, they want negative real rates to deflate their very large debt bubbles.

If the authorities do not allow rates to rise, then the EU and Japan will be facing deeply negative real rates. Gold should do quite well in such an environment. And once again, if you consider a weaker dollar on the back of a slowing US economy into a rising inflation environment, gold could really shine… at least until the dollar begins the next of its bull market (see prediction #6).

Which brings me to my next prediction, which is actually more of a statement of fact than a prediction, which in turn gives me confidence that I will absolutely nail it.

#10. In regards to future events, I know nothing.

No one does. My predictions are shouts into a howling wind. It is my hope that they have stimulated your mind and opened you to new possibilities.

To sum up, my 2017 Predictions are as follows:

#1. We have likely seen the top in the Chinese bond market.

#2. USDCNY will surpass the mythic 8 level.

#3. The BOJ and the ECB tighten monetary policy, and potentially end NIRP.

#4. In a phoenix like turn of events EU and Japanese area banks rise from the ashes… only to be slain once more.

#5. The dollar pause ain’t over…

#6. Don’t be fooled by any dollar weakness the dollar bull market ain’t over.

#7. The US Consumer Will Roll Over hard and the US will enter a recession in H2 2017.

#8. The US equity markets will peak in 1H 2017, and in spite of any Trump stimulus will end the year in the red.

#9. Gold will break its correlation to nominal changes in interest rates.

#10. In regards to future events, I know nothing.

I think Inflationary pressures originating primarily in China with help from OPEC are quite likely to ripple through the global economy, catching investors and central banks off guard. This inflation surprise should destabilize markets in ways that even the great and powerful Klendathu Capitalist cannot predict (see prediction #10.).

I would argue that those inflationary pressures have already done tremendous damage to the US economy where the US consumer was already suffering under immense pressure from stagnant wages and rising energy and healthcare costs. Unable to provide additional dollar liquidity to the rest of the world, the global economy will slow and the dollar will begin the next leg higher in its bull market.

If it was not obvious, a large portion of my thesis hinges on higher inflation coming out of China. I would argue that inflation has been baked into the cake via excessive monetary stimulus out of China, but I could be wrong. I don’t believe there’s much of a chance of a muddle through for China though, and this is likely the biggest hole in my thesis. If China muddles through and is neither too hot nor too cold but just right, I could prove to be very wrong. But there’s another outcome, which I find much more likely than a muddle through…

If China surrenders to deflation then everything I’ve said is null and void. Prepare for negative yielding US treasuries. $2,000 bitcoin, and volatility… lots of volatility. If anyone is offering residency in New Zealand here’s my email: zegemabeach@gmail.com…

Just kidding…

But seriously, everything I’ve said gets thrown out the window in the event China decides to have a hard landing, although I’d argue that within 18 months it will be forced on them. I hate to end my predictions for 2017 on such a gloomy outlook, so here’s some cheerful war propaganda for ya! And to paraphrase Lieutenant Johnny Rico,

“Come on you Apes, do you want to invest forever!”

Pingback: XAUJPY: The Coiled Spring – The Klendathu Capitalist

Pingback: Top Posts From 2016 – The Klendathu Capitalist

Pingback: One Belt One Road: Position Size and Time Horizons – The Klendathu Capitalist

Pingback: Keeping Up With The 2017 Predictions – The Klendathu Capitalist